Today’s Employment Data Come from a System Designed to Measure the Great Depression

The lecture addresses conditions in the American labor market today: trends in employment, unemployment, and an interesting category of adults who are not in the labor market at all but perhaps should be. We focus especially on that last category—the men and women officially termed “NILF” (not in labor force) in the United States government’s statistics.

Inattention, in both the academic and policy circles, to American adults who are neither working nor looking for work is in part a consequence of the way we collect and report official information on employment in modern America. A few words of background are in order here.

Nowadays, the government continuously tracks national employment conditions and reports on them every month through the familiar “Employment Situation Summary” bulletins, informally known as the monthly jobs report (BLS 2023). But it was designed in a bygone era.

The monthly jobs report is ostensibly a product of the early postwar period: its initial release was in 1947, and its first full year of reported national coverage was 1948. But its genesis dates back earlier to the final years of the Great Depression (Dunn, Haugen, and Kang 2018).

During most of that prolonged economic crisis, astonishing as this may sound now, the United States lacked comprehensive, consistent, and timely data on the magnitude of the national unemployment problem. Such data as were to be had on employment and unemployment in America during the 1930s were limited, haphazard, and often incomparable. It was only in 1939 that the project of categorizing, compiling, and producing modern job and wage data as we know them commenced, pioneered by statisticians at the New Deal’s Works Progress Administration.

The labor data from that project initially debuted in the 1940 census, which estimated the national unemployment rate in March of that year at 14.6 percent. Although there have been certain changes to the survey since early 1940, the basic methodology and definitions for our current measurement of employment and unemployment have been in place ever since then.

The Current Population Survey, whence the facts and figures in the government’s monthly jobs report emanate, is thus a product of the Great Depression, reflecting its concerns and expectations. It focuses on trends in unemployment and in gainful employment. And reasonably enough: updates on the headline numbers from the labor force were crucial and remain so—they are still eagerly awaited each month on Wall Street and in Washington.

But Depression-era statisticians had no reason to be especially interested in the size or composition of the population of men and women outside the labor force. At a time when over a seventh of the workforce was seeking employment and could not find it—the situation in early 1940—no one would have imagined that appreciable numbers of grown men who could be looking for work would not be doing so. Consequently, the NILF population was a statistical afterthought, a residual number available only as a remainder after the key labor-force numbers had been subtracted from the adult civilian noninstitutional population.

Yet, as fate would have it, trends in the NILF population took on a life of their own in the postwar era, and in a manner no one with a Depression-era mentality could have imagined. The past two generations have witnessed troubling and historically unfamiliar long-term declines in workforce participation for key segments of the working-age population. I have referred to that phenomenon elsewhere as “the flight from work” (Eberstadt 2016). And, as we will see, that flight from work is not only continuing but seems to have spread unexpectedly to new demographic contingents since the coronavirus pandemic.

The Great Postwar Flight from Work by Prime-Age Men in America

The US labor force more than doubled in size between 1965 and early 2023, rising from less than seventy-five million to over 165 million. Over those decades, US labor-force growth was more robust than in most other developed economies. But, over those same years, a problem was quietly gathering: male workforce participation was steadily faltering.

The problem was disguised by new sources of labor-force growth, which kept the national labor supply burgeoning: first, through the influx of women into the workforce, and, later, through an upsurge in immigration (both legal and illegal). The faltering of male workforce participation was further disguised by prolonged periods of relatively low unemployment: numbers widely taken to mean that the country was genuinely at full employment or close to it. But today, low unemployment rates coexist with low employment rates for American men.

The paradox is underscored in figure 1, which displays work rates (the employment-to-population ratio) for US “men of prime working age” from 1965 through early 2023. That paradox originally attracted my attention back in 2016 when I released the first edition of my book Men without Work: America’s Invisible Crisis.

“Men of prime working age,” or “prime-age men,” are what labor economists call civilian noninstitutional men between twenty-five and fifty-four years of age. The term itself is self-explanatory. Despite all the changes in the composition of the labor force in the postwar era, this demographic group is still indispensable to the economy—arguably, it remains the economy’s backbone. And these men have other important functions in society: this, after all, is the portion of the life cycle when family formation and child-raising typically take place.

From the mid-1960s to the present, the United States has witnessed an eerie but relentless increase in the proportion of prime-age men with no paid work. Today, that proportion parallels the level reported at the tail end of the Great Depression. Actually, at the time of this lecture (for which the latest data come from February 2023), the seasonally unadjusted work rate for US prime-age men was slightly lower than when unemployment was first officially measured back in March 1940. This is not a new occurrence. As may be seen in figure 1, over the entirety of the twenty-first century thus far, the mean monthly percentage of prime-age American men with no paid work has been over a percentage point higher than it was back in March 1940 when the national unemployment rate was almost 15 percent! Yes, twenty-first-century America has more income than ever before, more education than ever before, and more prosperity than ever before. And yet the average percentage of nonworking prime-age men in our country is higher than it was at the tail end of the Great Depression.

Note in figure 1 how, incidentally, the percentage of nonworking prime-age men has been climbing over the postwar period. In our decade to date, its average monthly level is over two and a half times higher than in the 1950s and almost three times higher than in the mid-to-late-1960s.

The paradox of simultaneous low unemployment rates and low employment rates for the contemporary prime-age American male population is exhibited in figure 2, which compares trends in postwar-era monthly headcounts for prime-age men who are unemployed—out of a job and looking for work—and those who are NILF—neither working nor looking for work.

Over the generations under consideration, the latter came to outnumber and then to dominate the former. The last time America counted as many prime-age unemployed males as prime-age NILF males was back in the early 1990s, over thirty years ago. Even in the depths of the Great Recession and the darkest months of the COVID-19 crisis, fewer prime-age men were reportedly unemployed than out of a job and not looking for work. In the 2020s, despite the spectacular shock of the pandemic to the labor market and the highest postwar unemployment rate yet registered, the average monthly ratio of NILFs to unemployed among prime-age men was nearly three to one—and in early 2023 that ratio was well over three to one.

Thanks to the Depression-era conceptions and definitions that still shape our current labor market numbers, these NILFs are omitted from the monthly summary statistics on the US jobs situation. That is why it is possible to hear the continuing patter of “happy talk” from the Fed, Washington, and Wall Street about how we are “at or very near full employment” at the same time that we have Depression-era work rates for men. If you are measuring macroeconomic well-being or guiding economic policy by the unemployment rate, you are missing three-fourths of the problem, at least when it comes to nonworking prime-age males.

To be sure, declining prime-age-male labor-force participation rates—the driver of the exploding NILF counts in figure 2—have been noticed and discussed by economic and policy experts. But in economic and policy circles today, this long-term flight from work by prime-age males is still usually described as a consequence of “structural and technical transformation” of the national and global economy. The prevailing consensus in academic and policy circles still attempts to describe the ongoing drop in male workforce participation in terms of factors such as declining demand for less skilled labor, the decline in manufacturing’s share of employment, China’s entry into the World Trade Organization, offshoring, and other facets of globalization.

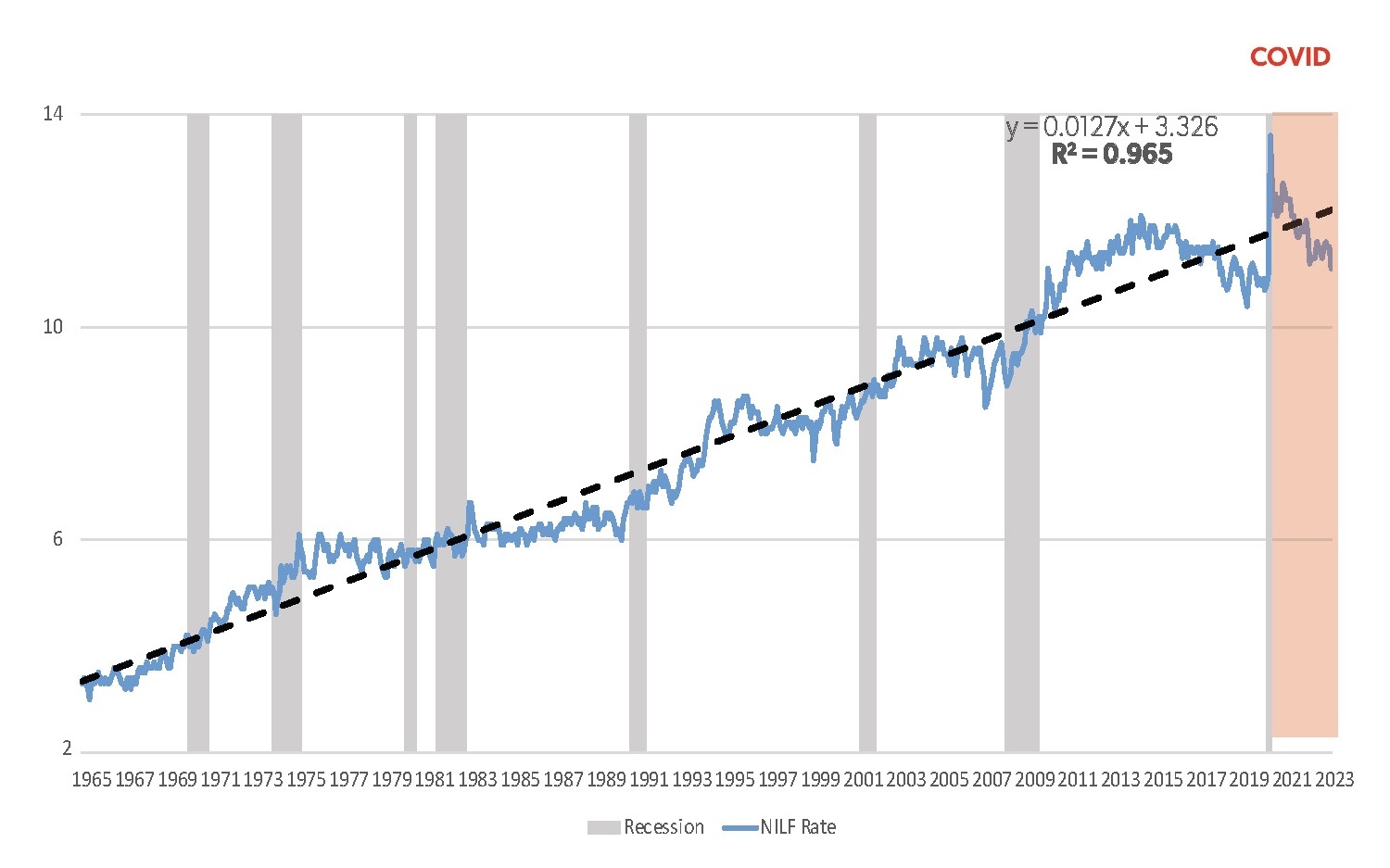

Now, there is truth in this received wisdom. The trouble, I would submit, is that it’s not the whole story, and, as I have argued elsewhere, it isn’t even most of the story. The shortcomings of this received wisdom are vividly revealed in figure 3, which plots a simple ordinary least squares regression line through over half a century of data on prime-age-male NILF rates, covering the period from 1965 to the present. Using calendar month as the independent variable and NILF rate as the dependent variable, we obtain a coefficient of determination—an R squared—of almost 0.97.

I like to describe that graph as a social-science straight line. Unlike the natural sciences—which deal with physical constants like orbital patterns and chemical bonds—the social sciences must contend with human beings, who tend to be slightly more unruly and untidy in their behavior. Given that we are talking about human events, the upward trajectory of the prime-age-male NILF rate appears to be stunningly regular from one month to the next over the nearly seven hundred consecutive months under consideration in figure 3.

Now, why is this a problem for the received scholarly and policy wisdom on the prime-age-male flight from work in modern America? Simply put, it confounds all their “demand-side” presumptions. If the main factor influencing this collapse of work for prime-age men were demand-driven economic and structural change, as the received wisdom holds, we would expect business cycles to show up in figure 3. But no perturbations in NILF rates worth mentioning are visible in the graph in the wake of each of the many recessions since 1965. Nor is there any reflection of the trade-and-employment shock registered in America after China’s 2001 accession to the WTO. Nor for that matter do we see any reflections of the succession of disruptive technological innovations over the many decades figure 3 covers. Like Old Man River, the upward trend in prime-age-male NILF rates in figure 3 just seems to keep rolling along no matter what else is going on in the world.

I might mention another striking finding from that chart, one that will not be evident to viewers. An earlier version of that same chart appeared on the cover of the first edition of Men without Work in 2016. In preparing a second edition of the book in 2022, six years later, I updated the underlying data and reran the regression. Six years later, the regression model for predicting prime-age-male NILF rates on the basis of calendar month was virtually identical to the original—with constant, beta coefficient, and R squared all matching down to the third or fourth digit. The simple bivariate regression model in figure 3, updated still further since the release of the second edition of Men without Work, is likewise nearly identical to the initial model nearly seven years earlier. I have no explanation for the stubborn consistency of estimated model results over time. Coincidence perhaps, but it is a striking result nonetheless, and not one that lends support to the “demand-side” interpretation of events.

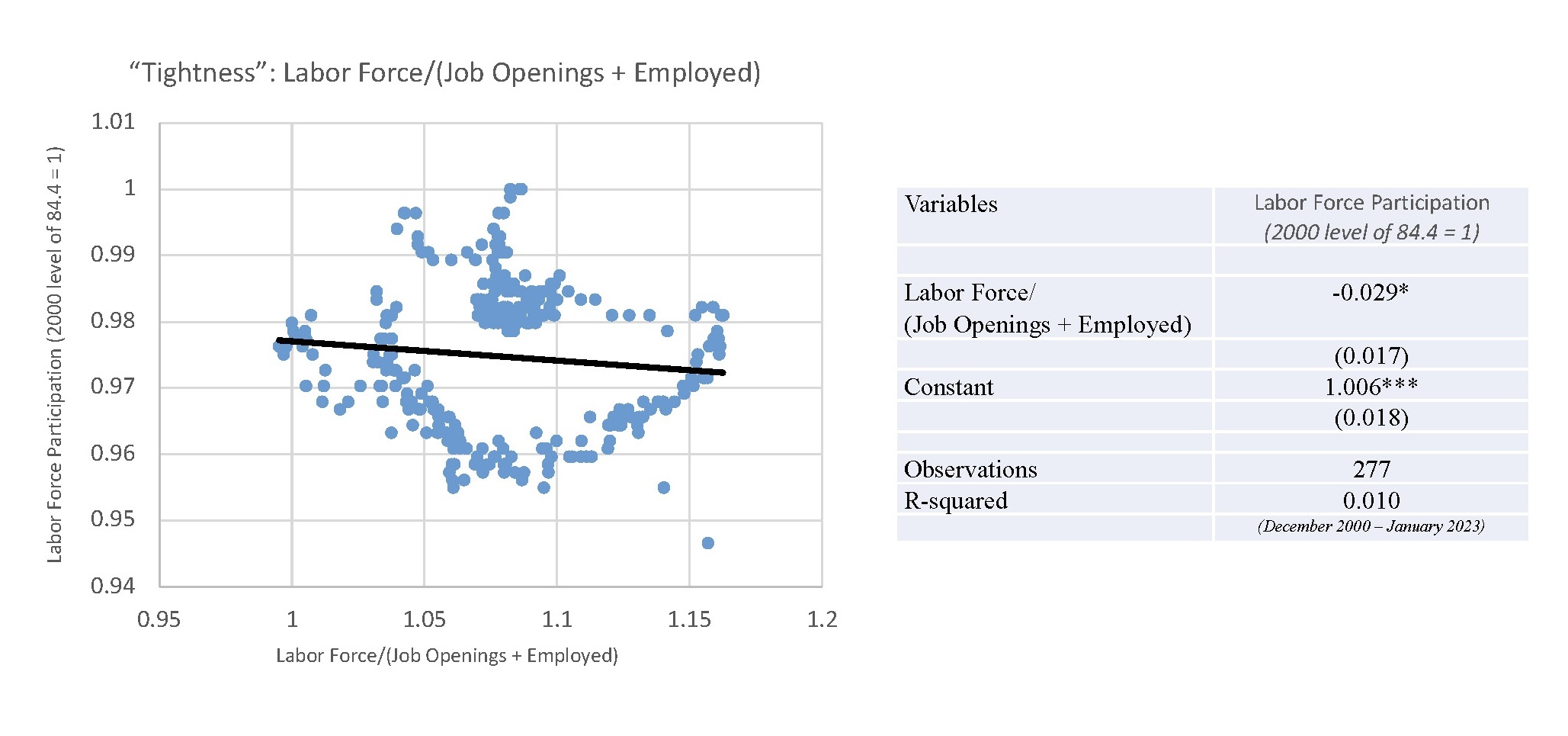

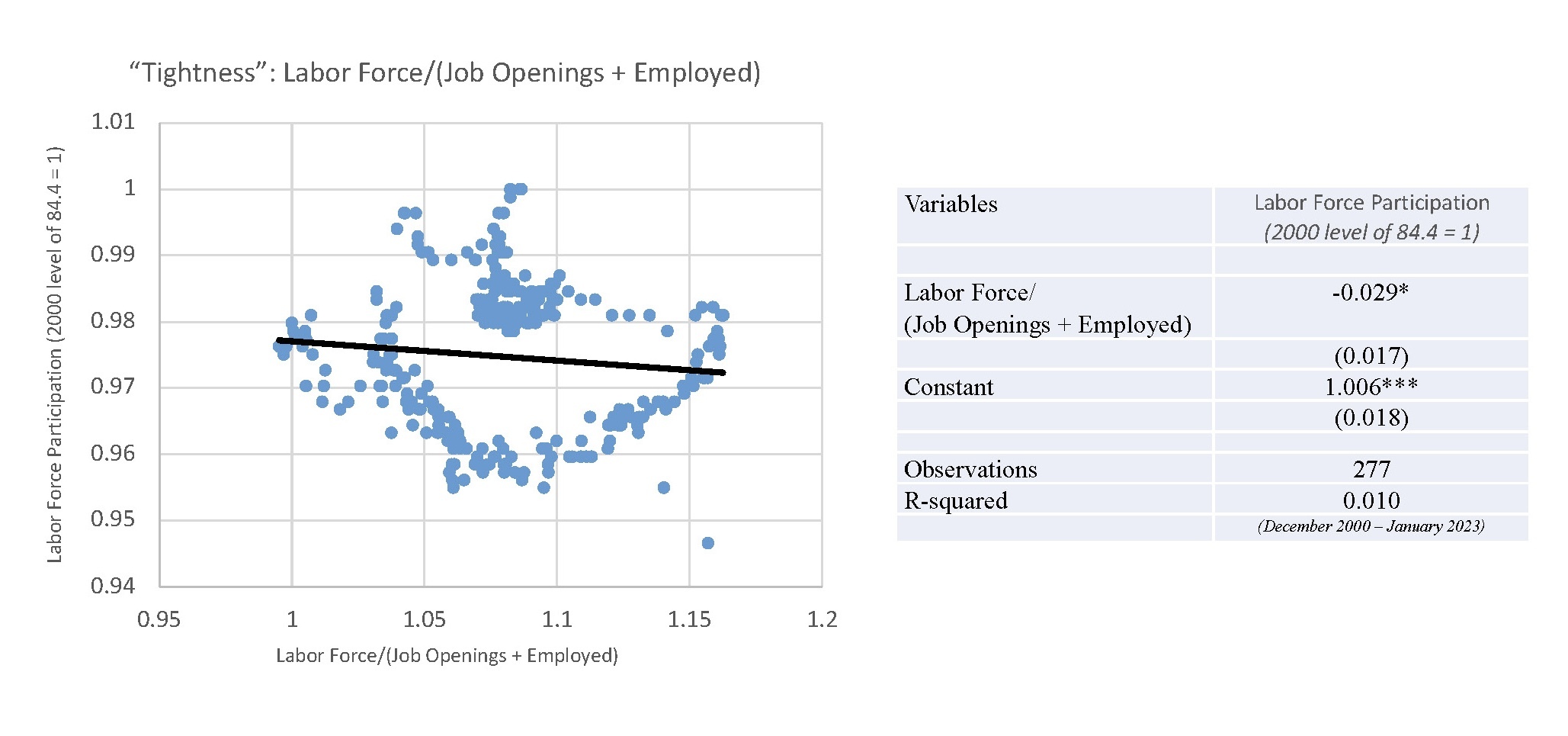

Further skepticism about the predictive power of the “demand-side” explanation for the long-term rise in prime-age-male NILF rates may be encouraged by figure 4, which charts the relationship over time between overall labor-force tightness, on the one hand, and the prime-age labor-force participation ratio (LFPR), on the other. In this figure, labor-force tightness is measured as the quotient of labor supply divided by the sum of employed persons plus job openings, while the LFPR for prime-age men and women together is scaled against its 2000 level. We use monthly readings for the period since January 2000 as our dataset, a pool of over 270 observations as of this lecture.

All else equal, we might have assumed that tighter labor markets—periods associated with relatively more demand for workers than supply of them—would bring some of the prime-age NILF men and women sitting on the economic sidelines back into the labor market. Yet figure 4 shows little evidence of this for the twenty-first century to date. Our results show practically no association between labor force tightness and prime-age LFPRs (R squared of just 0.01). This simple regression reaffirms something more sophisticated analyses have already demonstrated. While mobility between unemployment and employment tends to be quite fluid—out-of-work job seekers tend to get back to work fairly quickly in the United States—labor-force dropouts, and especially prime-age-male labor-force dropouts, tend to be long termers. Just why this should be the case is of course an important question for our nation today.

At present, roughly seven million prime-age men are neither working nor looking for work—this out of a total population of around sixty-three million civilian noninstitutional American men between the ages of twenty-five and fifty-four. The prime-age male NILF population is about seven times larger than it was in 1965—and the NILF rate today is over three times higher than it was back then. If demand-side factors cannot satisfactorily explain much of this momentous change, what can?

The economists in the audience will immediately be wondering about supply-side factors and institutional barriers. And there are likely suspects at hand in both regards.

With respect to supply-side factors, the most obvious general change in the US economy since 1965 would be the enormous expansion of the welfare state, with all of the potential disincentives to labor-force participation its many programs and benefits might provide. Of particular interest here is the expensive jumble of disability-insurance programs available at the federal, state, and local levels to prime-age men. These programs do not coordinate with one another, so economists and policy makers do not know—and cannot know—exactly how many people in our country are on one or more disability programs at this moment.

In the 2016 edition of Men without Work, however, I used Census Bureau data to demonstrate that more than half of prime-age male NILFs were obtaining one or more disability benefits in the years before the COVID pandemic—as were at least two-thirds of the households in which these nonworking men lived. That finding cannot speak to causation, and government disability benefits hardly afford a princely lifestyle. But they manifestly do help to finance a life that does not include work—and for many more prime-age male NILFs than economists and policymakers commonly assume.

As to institutional barriers, the obvious culprit here, so to speak, is the vast increase in the population of sentenced felons since 1965, with the explosion of crime and the subsequent surge in punishment. Here again, official data are woefully weak. As I prepared my research for Men without Work, I was stunned to learn there simply are no official data on employment rates for ex-cons. In fact, Uncle Sam cannot even give you an estimate of the number of people in America with felony convictions in their backgrounds.

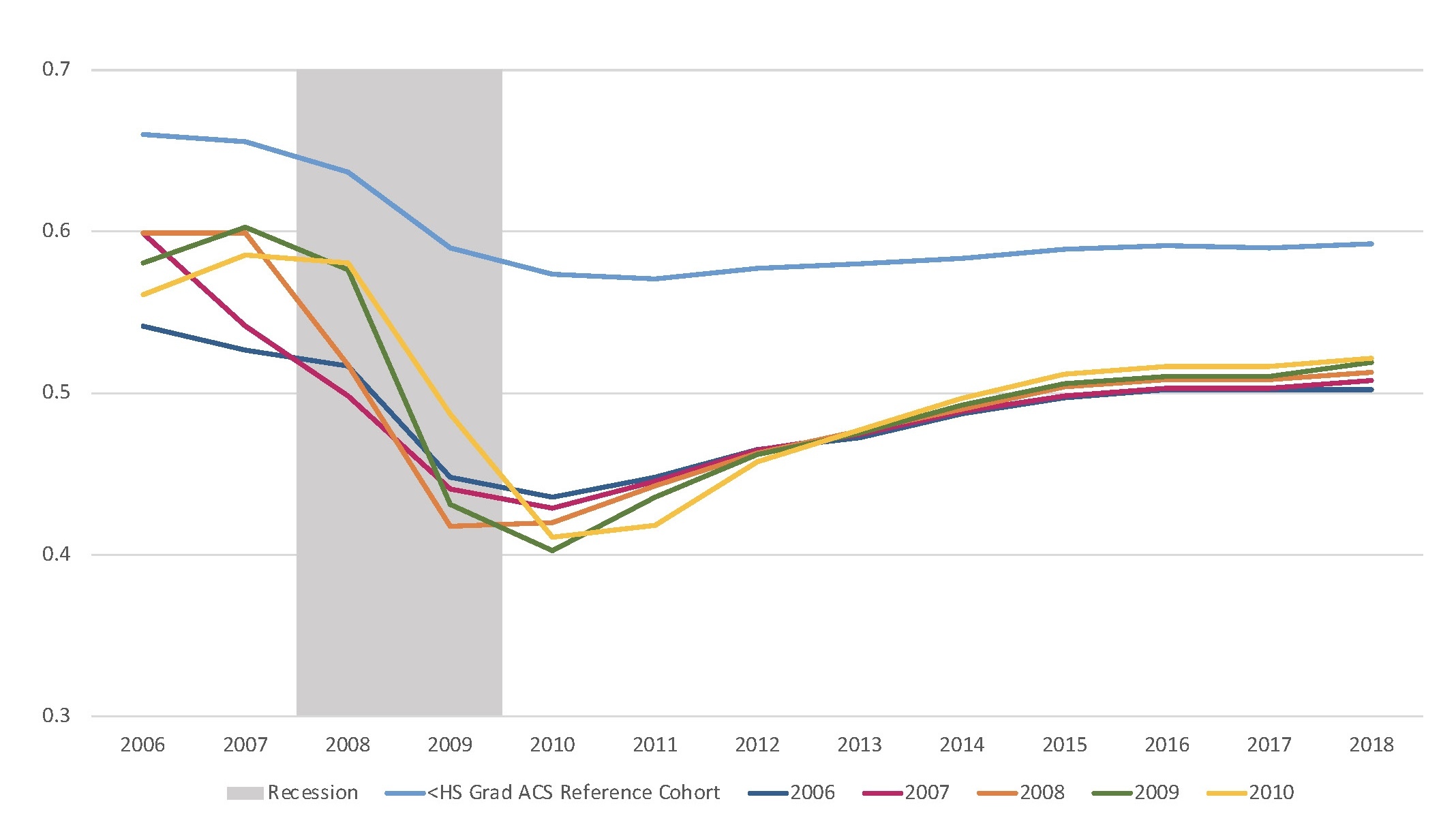

But demographic reconstructions by independent scholars suggest that nearly twenty million American adults—overwhelmingly male—were felons or ex-felons in 2010 (Shannon et al. 2017). By my own back-of-the-envelope calculations, that would mean roughly one in seven men in America today carry a felony conviction. The impact of this national burden on the labor market can hardly help but be consequential. Indications of just how consequential are suggested by the intriguing scholarship in figure 5, which utilizes state-level data to trace employment rates for ex-cons in the wake of the Great Recession. As may be seen, their employment prospects were far poorer than even those for high-school dropouts. Much more work is needed to illuminate the circumstances of America’s statistically invisible ex-con population and to understand the role that the rise of this cohort plays in the long-term rise of America’s nonworking male population.

America’s Strange New Peacetime Labor Shortage

Let us turn now to the impact of the COVID pandemic on the US labor market. The pandemic was a terrible catastrophe: COVID cost the lives of over a million Americans in 2020 and 2021 before the full rollout of the remarkable new mRNA vaccines. We would expect a disaster of this magnitude to have reverberations on employment and work. The actual trends that we have witnessed, however, were predicted by no one.

In the wake of the COVID catastrophe, America came to experience a labor shortage—a peacetime labor shortage. We have never had a peacetime labor shortage in this country before. It’s a highly unusual thing to see in any market economy, simply given the nature of free markets. Labor shortages are instead characteristic of Soviet-style, centrally planned economies, where they are entirely characteristic—an outcome of constant and extreme policy-induced distortions.

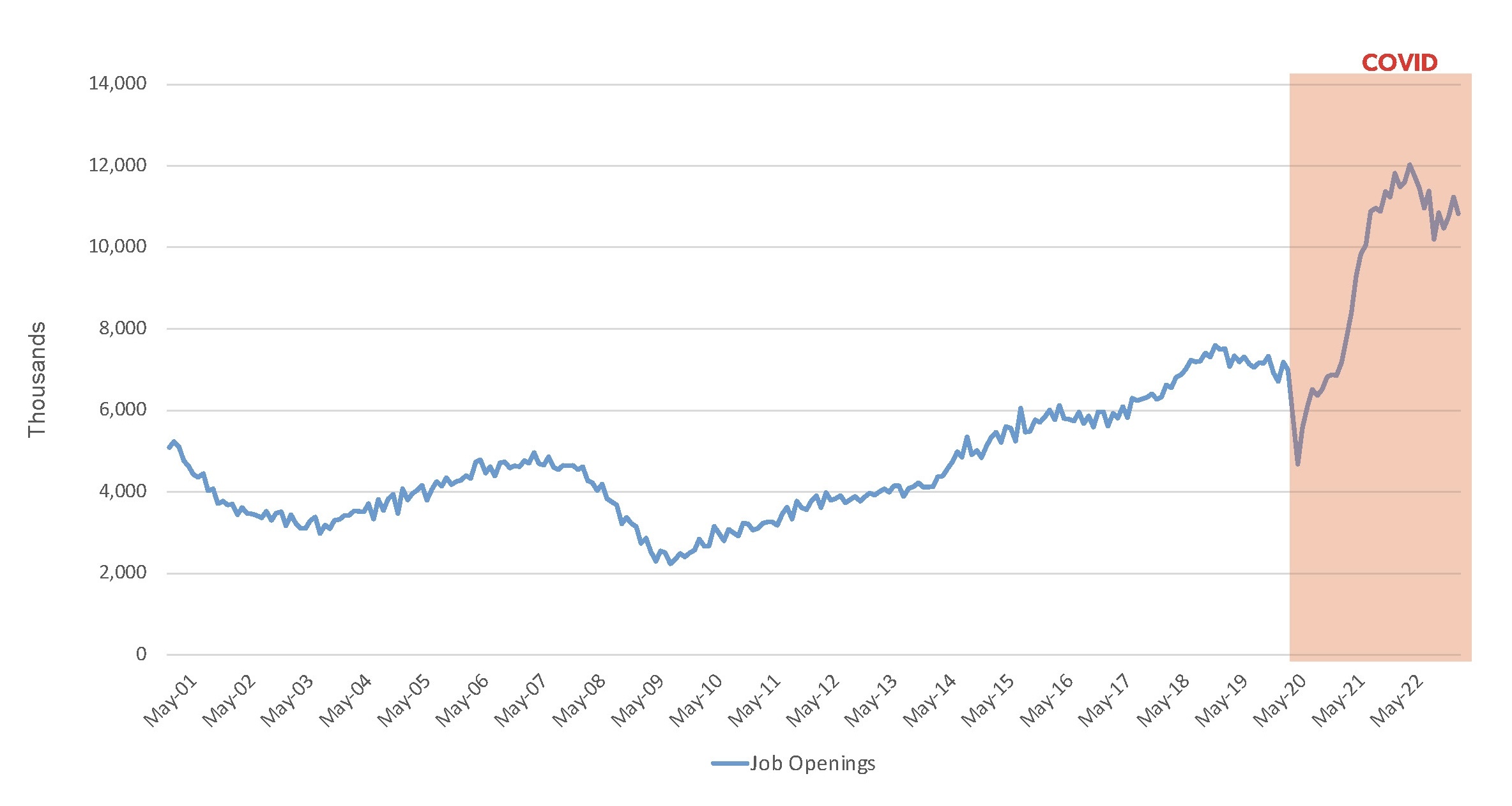

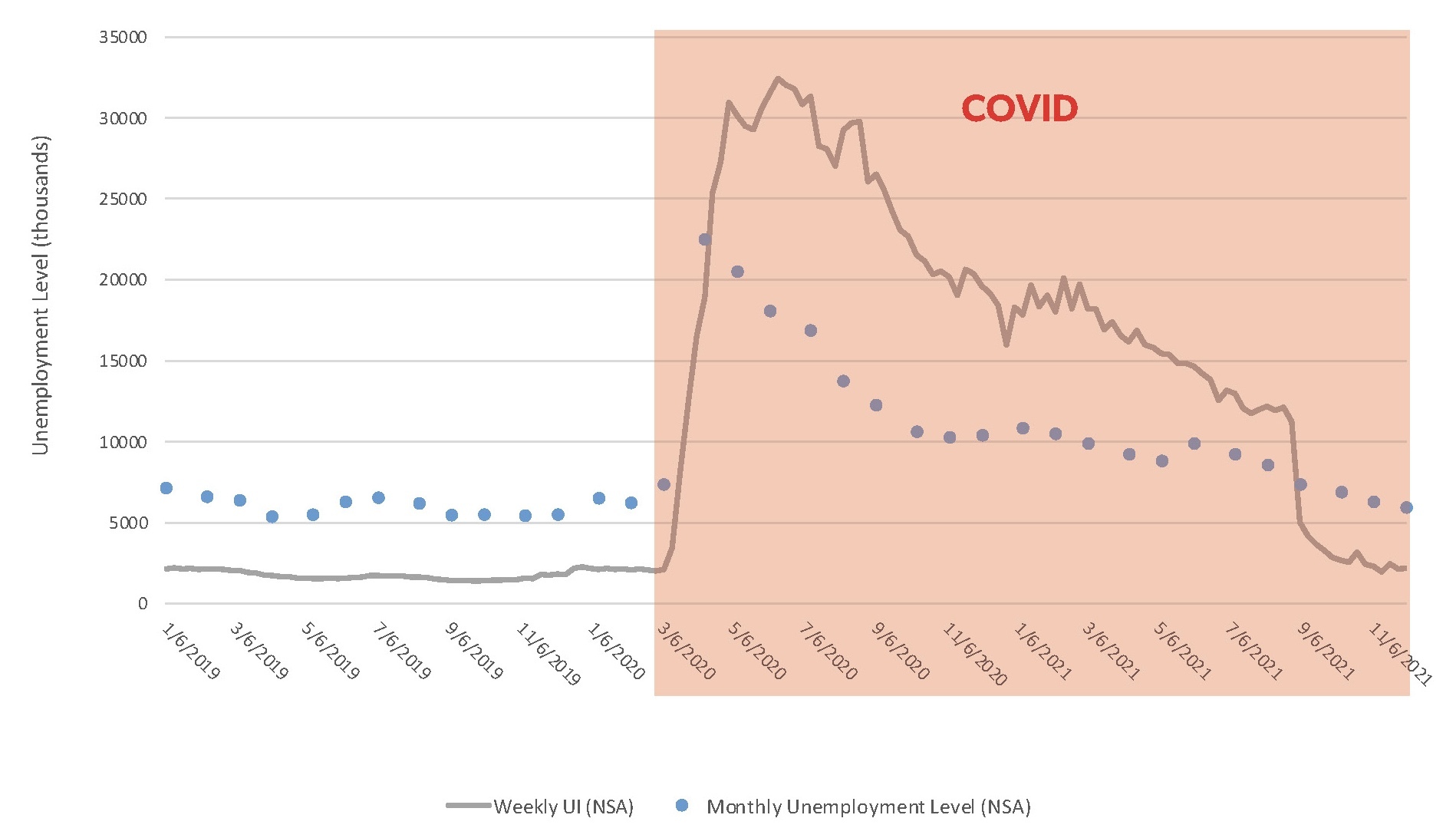

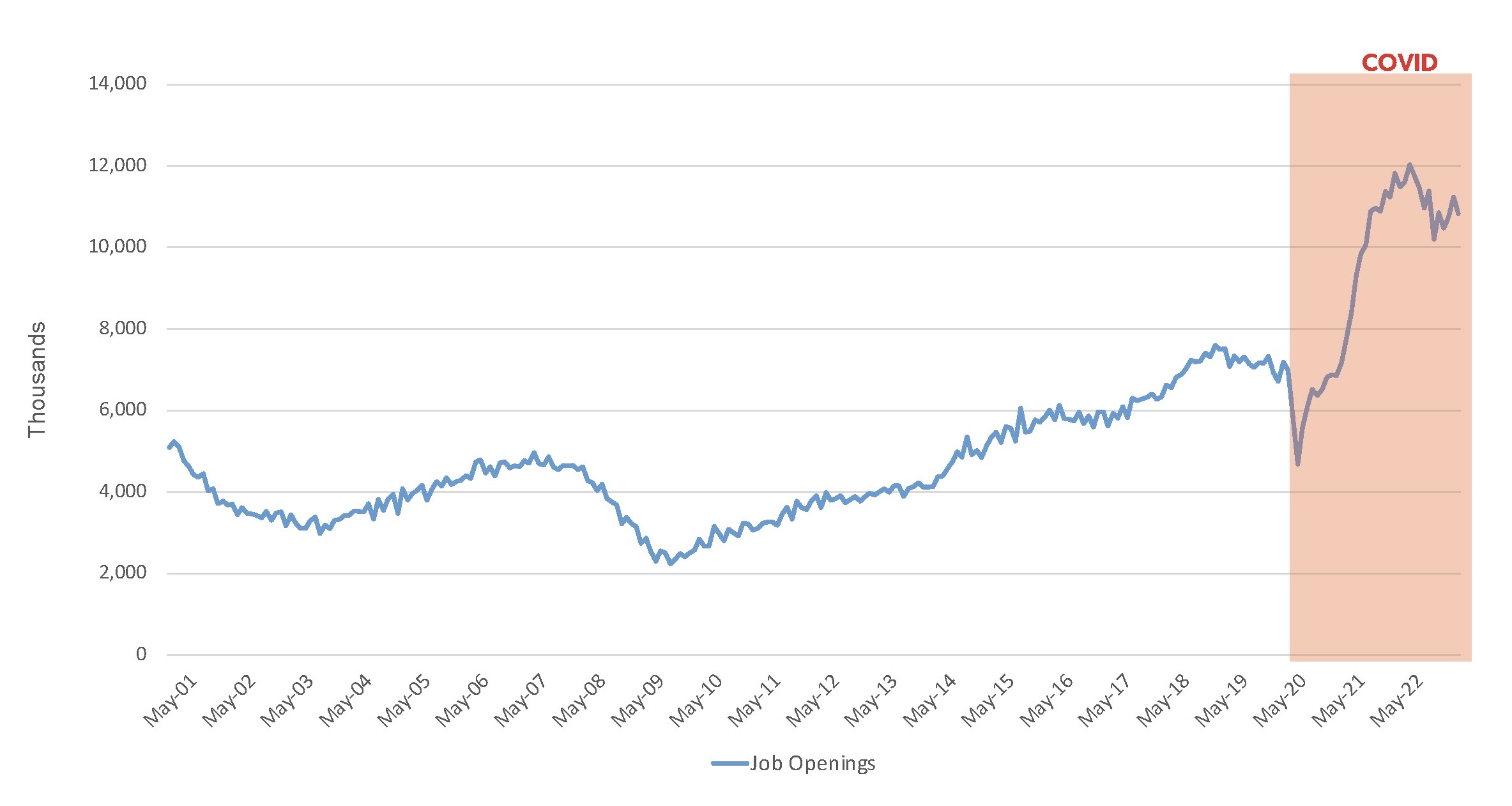

Figure 6 offers an indication of the magnitude of the labor shortage that emerged in the aftermath of the COVID pandemic. The numbers are Bureau of Labor Statistics estimates of job openings in the United States While these figures may not be perfectly accurate—high-frequency data from private-sector sources provide slightly different estimates—the fact of the matter is that anybody who goes anywhere in the United States at this moment knows that employers are practically begging for job applicants even though job applicants have more bargaining power now, during the so-called Great Resignation, than at any time in living memory.

Why this sudden labor shortage? The men-without-work phenomenon described above cannot account for this. The long-term flight from work by prime-age men appears to be continuing—but, by itself, it does not explain the new post-COVID imbalances we see in our labor market. The sheer arithmetic of the labor shortage suggests that new groups in the workforce must have joined the flight from work too. And that is exactly what the data reveal.

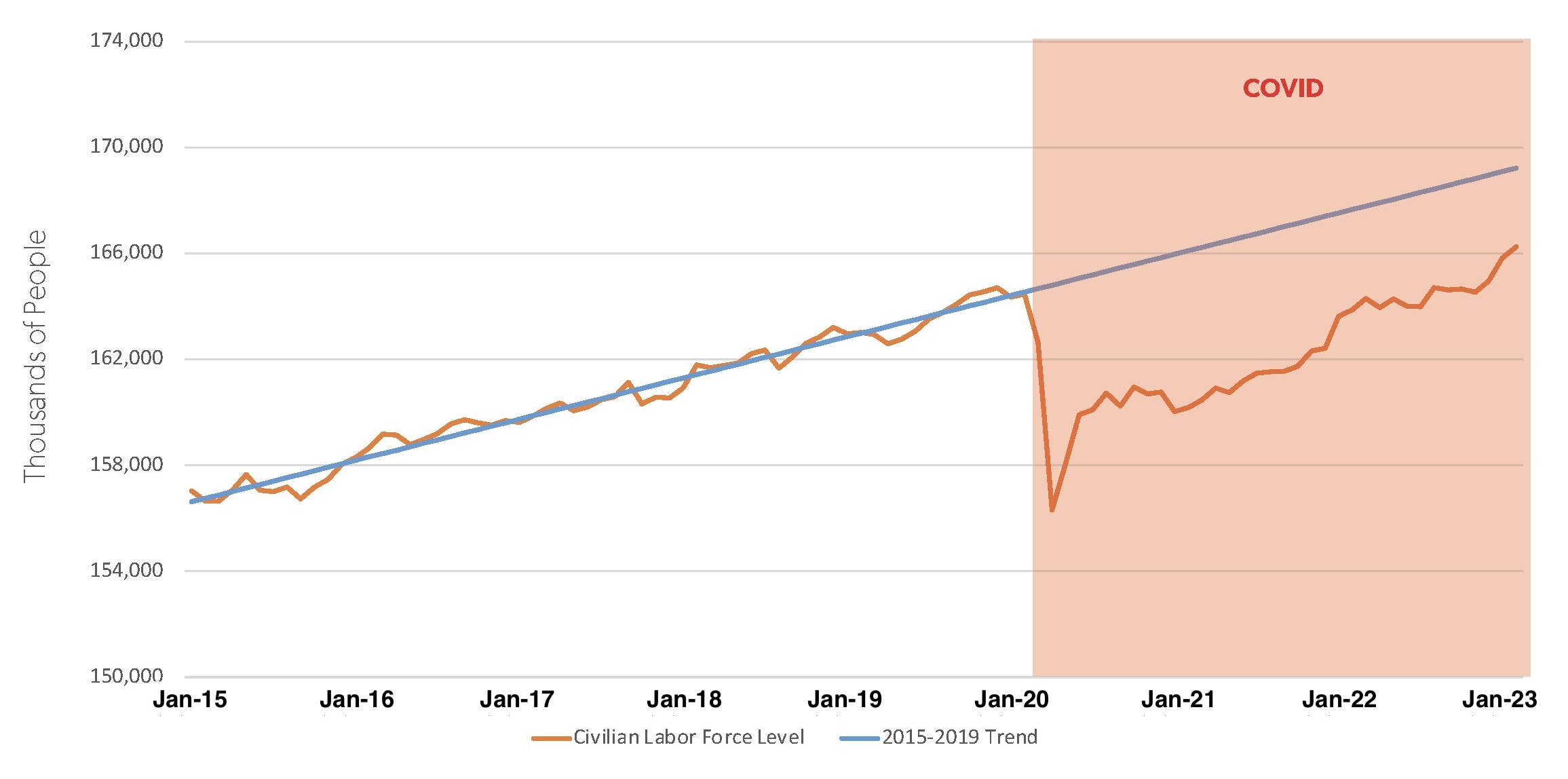

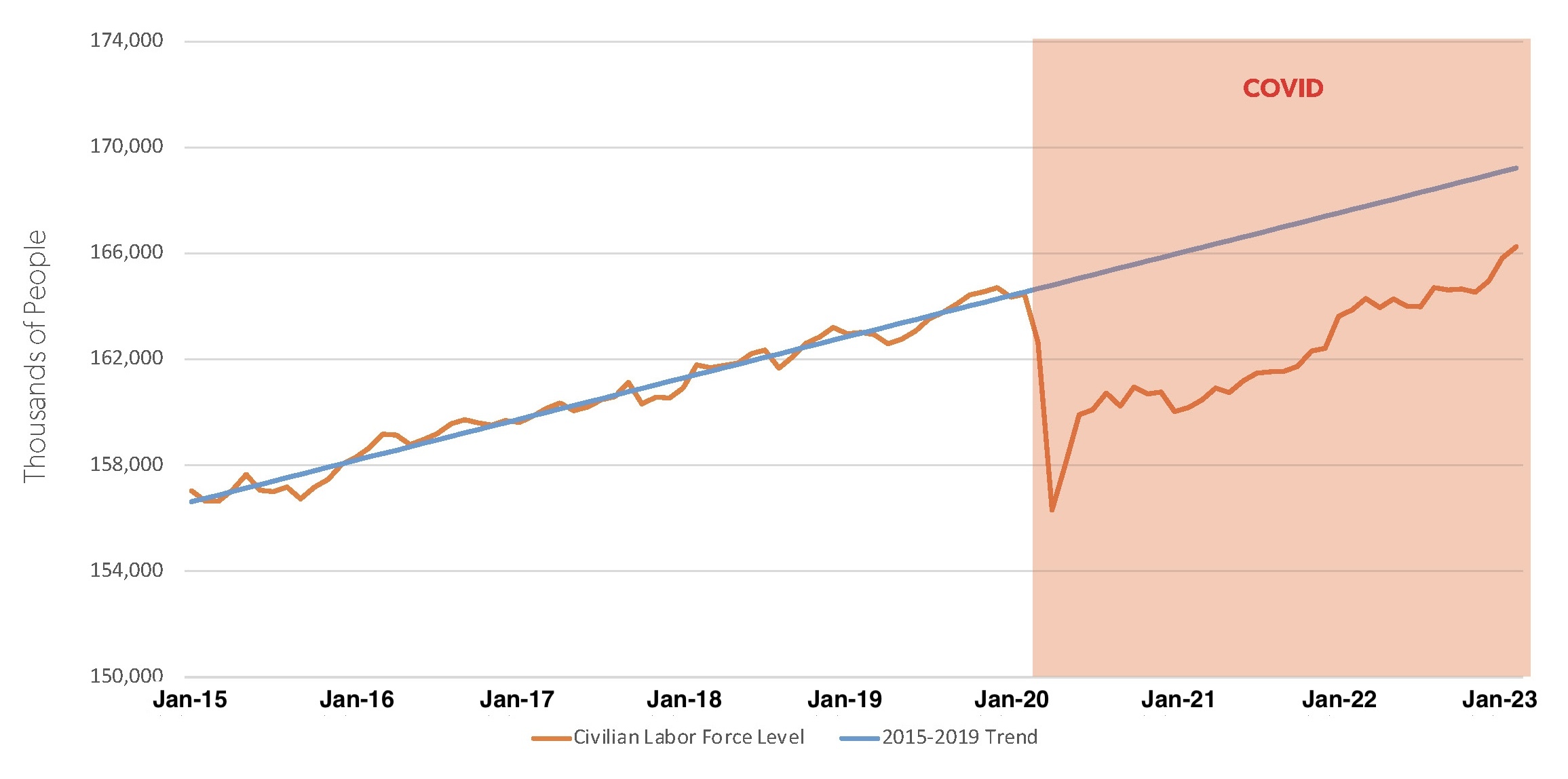

Consider figure 7, which contrasts the trend in actual US workforce numbers today with the totals we would have expected if pre-COVID trends had continued. Today’s labor force is about three million men and women shy of where we would have expected it to be. The gap between the trend line and the estimated labor supply seems to have been closing over the course of 2022—but painfully slowly.

There is a curiosity in figures 6 and 7. Back in our school days, those of us who studied economics were probably warned of the “lump-of-labor” fallacy. The good Lord did not sprinkle a specific, limited number of hours of work across every continent on the planet. Since human action creates demand for labor in a free market, the assumption that there is a fixed demand for work in the United States or any other market economy is simply wrong.

But you’ll see that the increase in job openings since the pandemic strangely mirrors the shortfall in manpower here. It is almost as if the lump-of-labor fallacy has been incarnated in contemporary America. This is not a result one would ordinarily expect to encounter in a market economy. It almost looks like something out of Gosplan.

How do we account for America’s current labor-force shortfall of roughly three million workers and would-be workers? Let’s examine potential components.

We have to start by looking at the COVID catastrophe itself, which, as mentioned, cost over a million lives in America and afflicted millions more with debilitating long COVID. In theory, losses from this public-health disaster could have taken a big toll on the US workforce. In practice, however, this does not seem to have been the case. Overwhelmingly, deaths from COVID were concentrated in America’s older population, people no longer in the labor force.

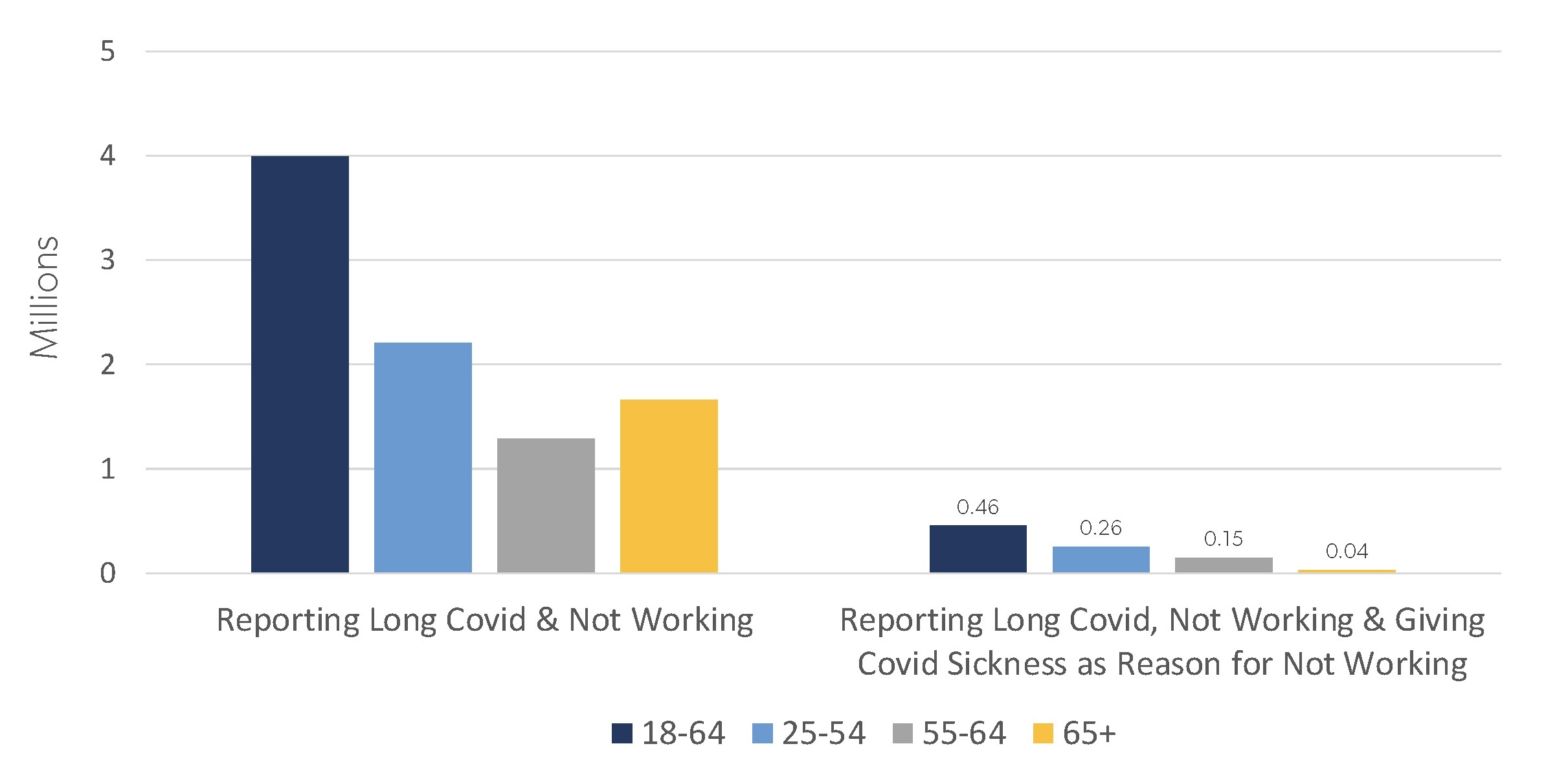

As for long COVID, many millions of Americans are still suffering from this, including millions who were once in the labor force but are no longer economically active. These raw numbers have led some researchers to conclude that long COVID is responsible for a drop of many millions in the ranks of the US workforce (Bach 2022).

But such presumptions are superficial and erroneous, as we see in figure 8. While about four million Americans who are no longer in the workforce recently reported that they had been affected by COVID, only a tiny fraction of them said they were out of the workforce because of COVID—that is, due to the direct impact of the illness itself or the need to take care of others with it. Among those 18–64 reporting long COVID and not working, 11.5 percent give the following reason for not working: “I am/was sick with coronavirus symptoms or caring for someone who was sick with coronavirus symptoms.” According to the Census Bureau’s new “Household Pulse Survey,” COVID is keeping just under half a million working-age men and women out of the labor force today. That is a large number, to be sure, but it pales in comparison to the three-million shortfall we have identified.

Now, immigration statistics are notoriously problematic. They are estimated as a residual from other demographic trends that we’re more confident about: births, deaths, and population totals. But to go by the numbers in figures 8 and 9, COVID health effects and immigration effects together would appear to explain half or less of the post-COVID workforce shortfall we have identified.

COVID-Relief Measures and the New Flight from Work in America

So how do we explain the rest? To begin, there is a new face of the flight from work in postpandemic America. It’s no longer just prime-age men.

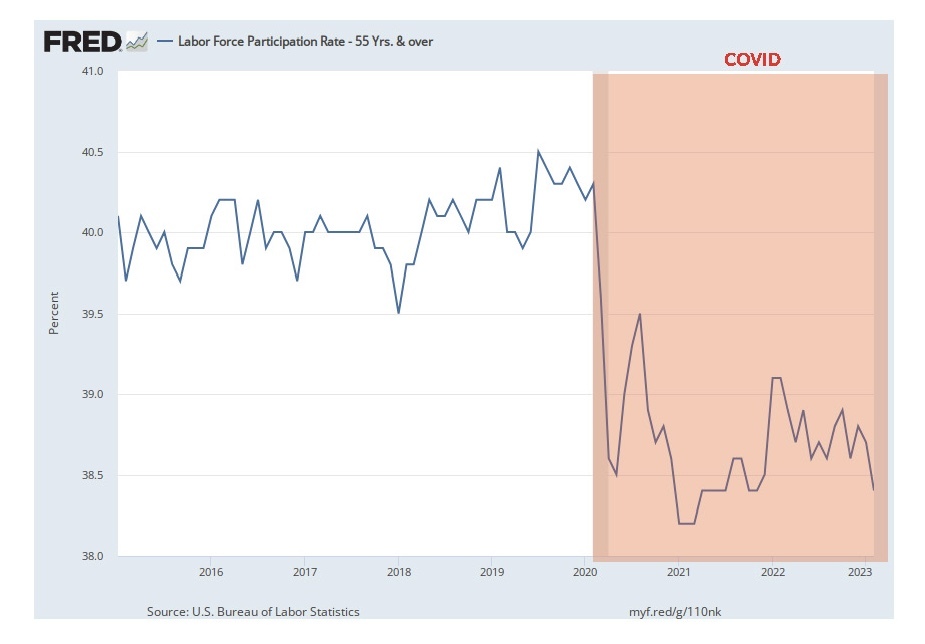

Before the pandemic, the only real ray of sunshine in the U.S labor tableau was the work profile for older American men and women. From the mid-1990s to the eve of the pandemic, the fifty-five-plus group was the only contingent in the US labor force whose work rates and labor-force participation rates were increasing. But that all changed with the COVID crisis, as we can see in figure 10. Roughly speaking, the shortfall in the fifty-five-plus workforce, in and of itself, currently comes to about 1.5 million today; it would account for about half of the total gap between current labor supply and the pre-COVID trend.

Like the rest of the workforce, participation rates for older workers took a severe hit when the pandemic struck. Yet despite America’s rapid economic bounce-back—and despite the vaccine rollouts and everything else—the labor-force participation rates of older men and women in the United States have not yet recovered.

This is a puzzle that has to be addressed and explained. I would suggest the answer has much to do with the COVID pandemic or, more specifically, with the government’s COVID emergency policies and their unintended consequences.

Immediately after the outbreak of the pandemic, US policymakers feared that the COVID pandemic and its associated lockdowns might precipitate a second Great Depression or even a general collapse of the world economy.[1] Informed by this sense of urgency, American policymakers took both monetary and fiscal policy into a sort of overdrive never seen before in peacetime.

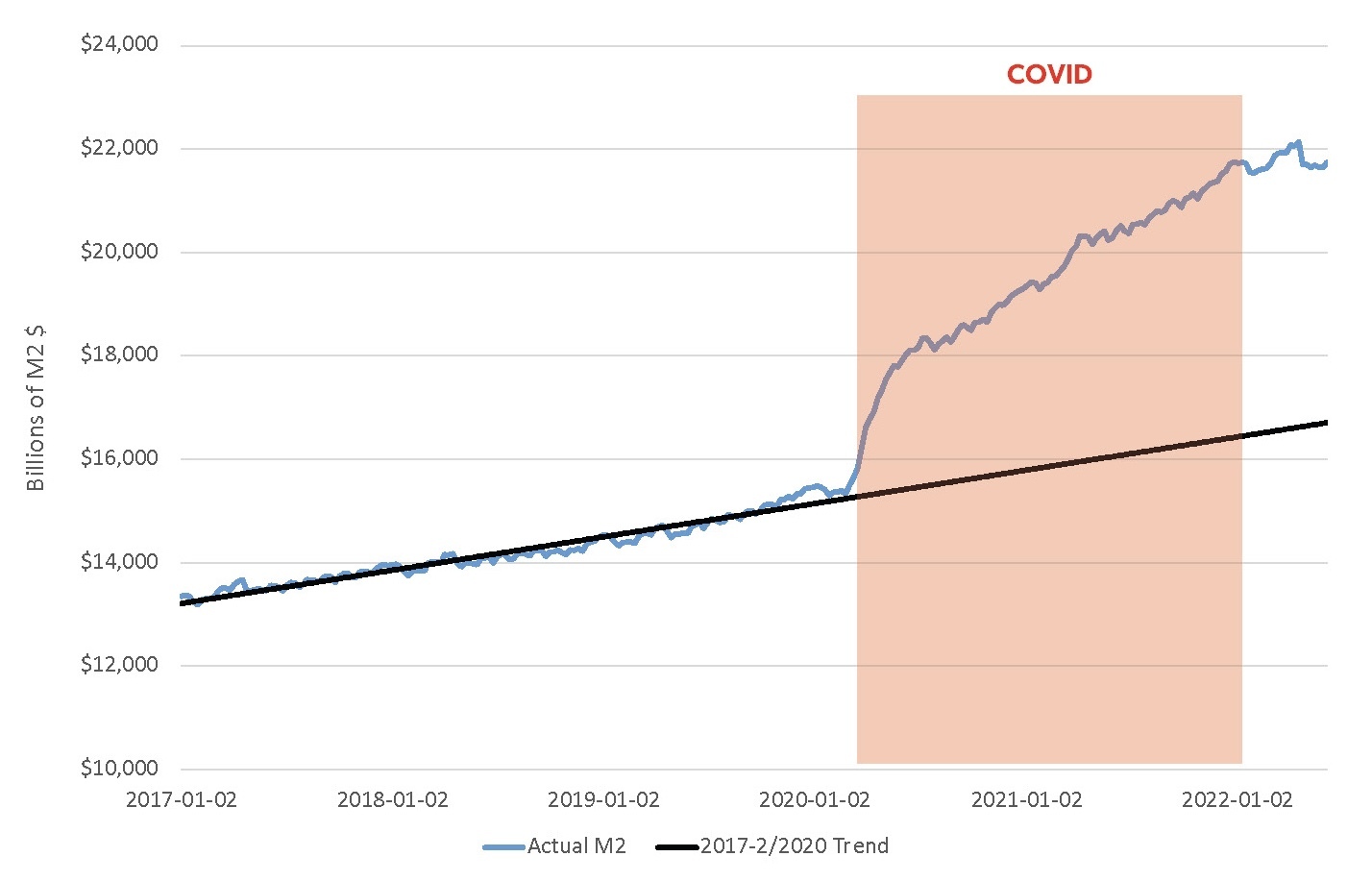

As we all know, the Fed pulled out the stops on monetary policy. Some (but not all) of its emergency measures are reflected in figure 11, which shows trends in US money supply over the past six years. As we are all aware, the surge in money supply during the pandemic was extraordinary: by mid-2022, M2 was 30 percent greater than would have been expected on the pre-COVID trend. That is a big monetary shock. If you’ve been to the grocery store lately, you may have noticed some of its consequences.

But we had what at least some of us would have identified as monetary-policy problems well before the pandemic too. For many years before COVID, we lived under a regimen of virtually free Fed money. Indeed, by some measures, such as the Cleveland Fed’s estimates of real one-year interest rates, the monthly average for real interest rates in the United States was running negative for over a decade and a half—since at least 2007 (Federal Reserve Bank of Cleveland 2024).

You do not have to be too much of an economist to imagine how such central-bank interventions could distort long-term investment choices and long-term macroeconomic performance. One consequence of exceptionally low real interest rates shows up as a fiscal-policy effect: negative real interest rates make it exceptionally easy for a government to finance domestic spending through public borrowing. And, of course, that is exactly what has taken place in America for most of the twenty-first century.

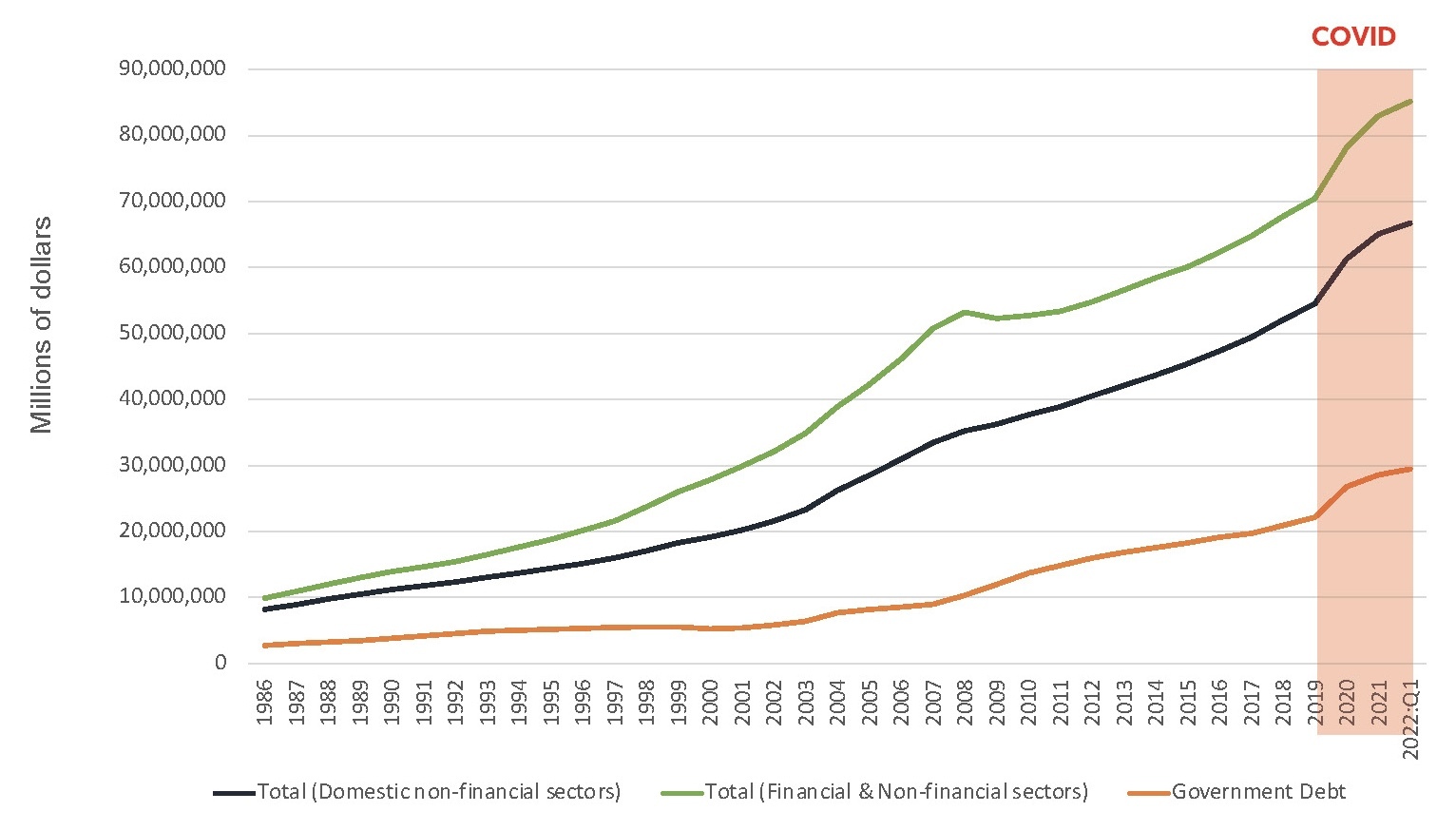

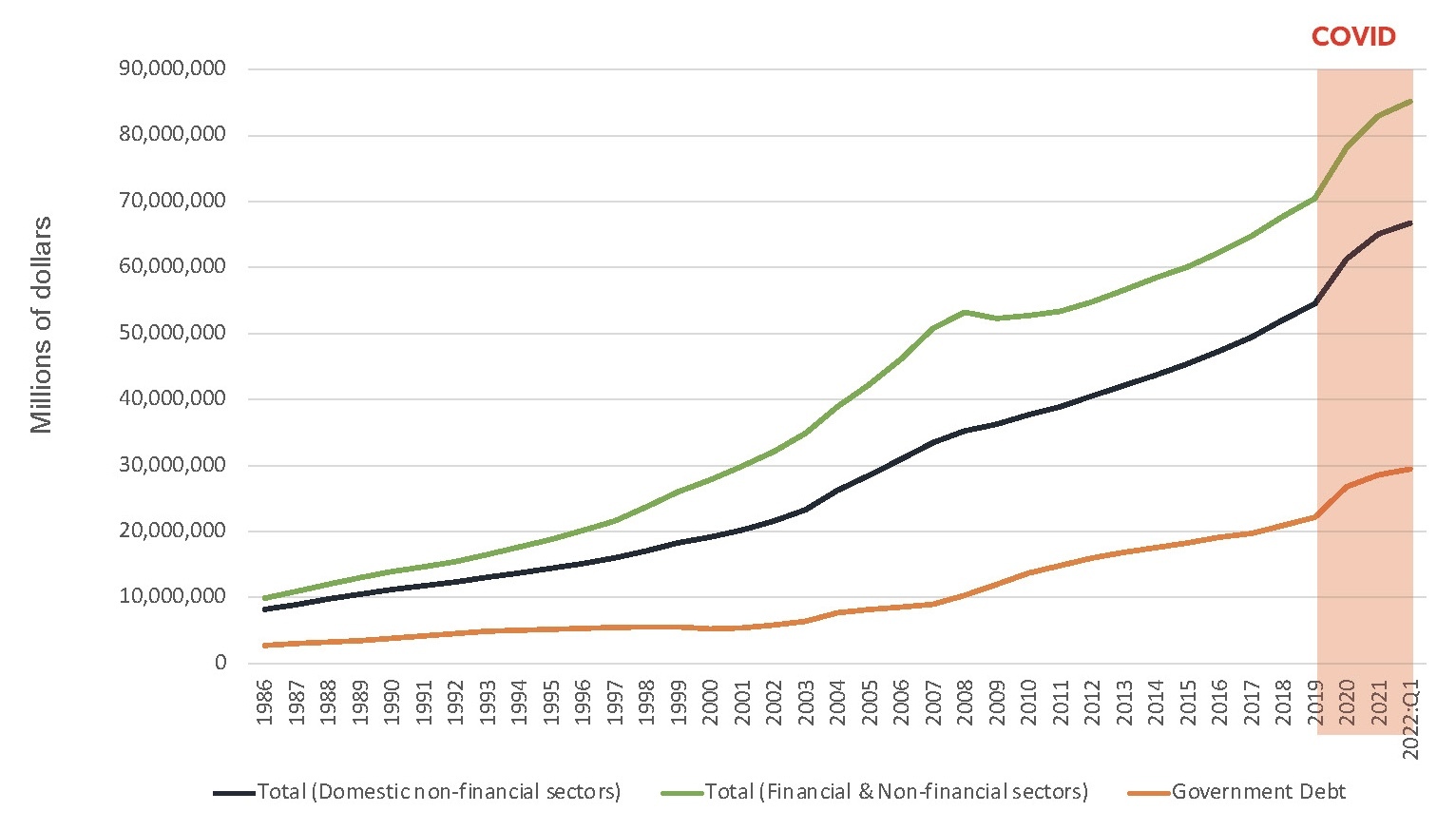

As we see in figure 12, nominal-dollar US government debt tripled between the end of 2007 and early 2022. Over that same period, the American government accounted for over 60 percent of all US debt accumulation. By contrast, the US private sector—households and businesses combined—accounted for only 39 percent of nominal credit growth over those years. In other words, a smaller share of American borrowing was going to at least potentially productive private-sector purposes than at any time since World War II. And with real interest levels at or below zero, the quality of such investments as were being financed by borrowing could also have been degraded. With negative real rates of interest, it is possible to turn a profit despite very low rates of return on capital. Is this what “secular stagnation” looks like, I wonder?

In any case, state mobilization of fiscal resources through heavy public borrowing had already become business as usual in the United States well before the outbreak of the coronavirus in 2020. Remember: in 2019—a time of ongoing economic expansion, maybe even the peak of a business cycle—the federal budget deficit amounted to 4.5 percent of GDP (OMB and Federal Reserve Bank of St. Louis 2023). Still, during the COVID pandemic itself, fiscal mobilization measures and the transfers of borrowed public money were like nothing America had ever before seen in peacetime.

Figure 13 tells the story. It shows disposable income, personal consumption expenditures (PCE), and personal savings in America before, during, and after the pandemic. Something entirely new, completely different from all previous experience, happened to the American economy during this particular crisis. During the pandemic, America’s disposable income jolted up—it shot up above trend. The COVID pandemic was the only economic crisis in US history in which disposable income went up. And, of course, it did so on the strength of transfers of borrowed public money.

Yet perhaps the most remarkable aspect of figure 13 is not the disposable income trend but rather the trend in personal savings. So massive were the successive waves of “stimulus” transfers during the COVID emergency that Americans found themselves with more money in their pockets than they cared to spend. Thus, America witnessed a doubling of the personal savings rate in 2020 and 2021—actually, somewhat more than a doubling. These borrowed-money windfall savings for America’s households amounted to roughly two and a half trillion dollars. That works out to an average of about $25,000 dollars per home.

This “wealth effect” from COVID-emergency-relief policies may be one of the keys to both the strange shortfall in labor supply in the post-COVID era and the changing face of worklessness in the United States today.

Basic economic theory would suggest that pandemic transfers would influence labor supply. The pandemic-relief programs provided a natural experiment of sorts, demonstrating the workforce’s sensitivity to direct and indirect subsidies for nonwork.

Consider the so-called Pandemic Unemployment Assistance (PUA) benefits. We all remember them—special payments to individuals during the crisis, earmarked at first for $600 a week, later $300 a week. I say “so-called” because, as we may recall, you didn’t actually have to be unemployed to qualify for them. You could also qualify for these benefits if you were working. In fact, some people who qualified for these benefits were earning six-figure incomes. They were so easy to obtain that they could almost be described as unconditional.

As figure 14 shows, the number of PUA recipients significantly exceeded the number of people who were unemployed during most of 2020 and 2021. At its peak, over thirty million adults were taking home “pandemic unemployment” benefits—twice the total number of unemployed at the time. This was not “unemployment assistance”—it was a guaranteed-income program of sorts: a limited test-drive for a “universal basic income” or UBI.

_claims__januar.jpg)

Now, notice what happened to workforce trends with the initiation of pandemic unemployment assistance and then with its termination. We can see this in figure 15.

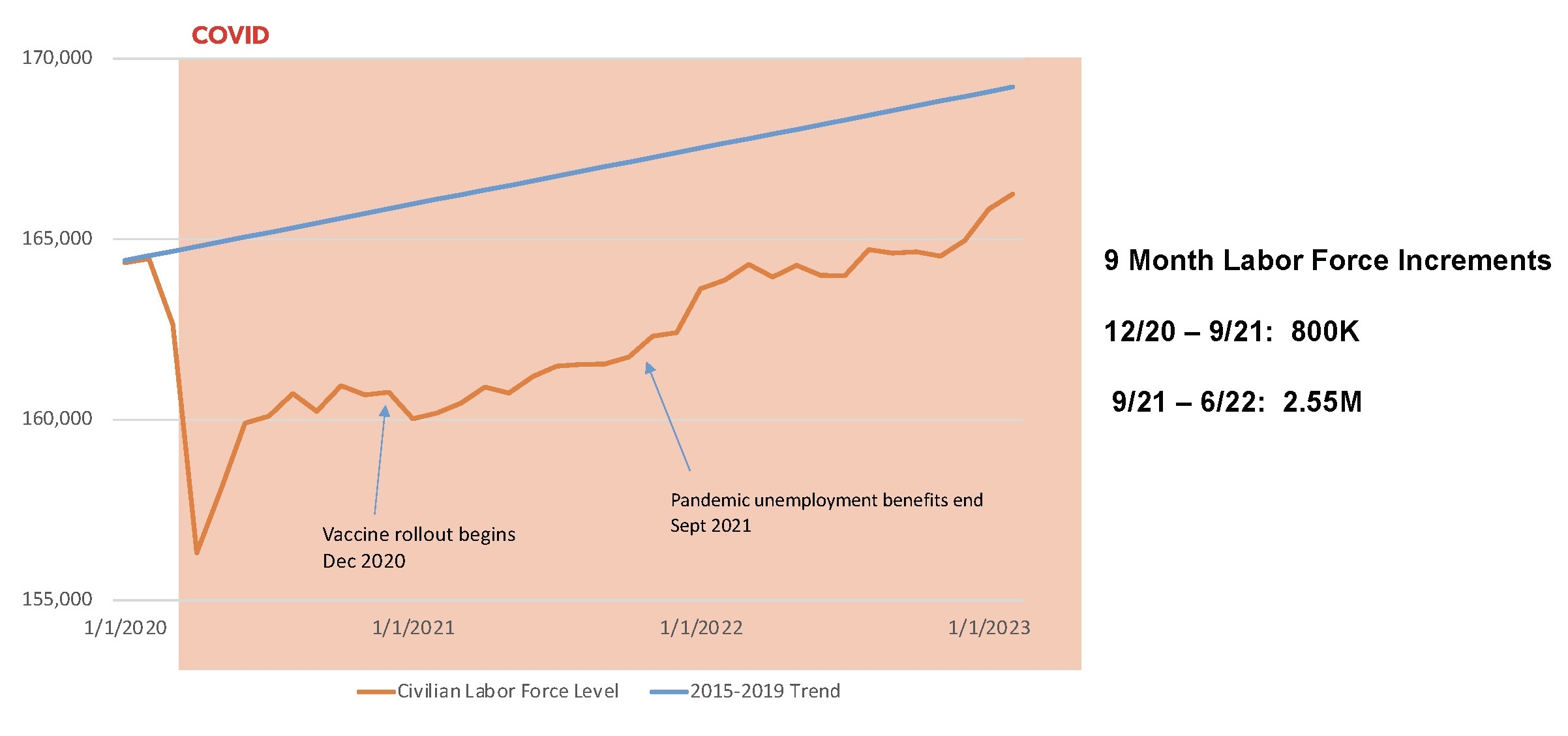

Recall the timeline here. The mRNA vaccines developed by Moderna and Pfizer were approved for general use in November 2020. Their rollout commenced in December 2020. In September 2021, on Labor Day, PUA benefits formally ended.

In the nine months between December 2020 and September 2021, despite a vigorous national COVID-vaccine rollout, the nation’s workforce recovery was tepid. Over those same nine months, despite a vigorous economic recovery and an incipient labor shortage, the civilian labor force grew by a disappointing eight hundred thousand—a mere three-fourths of the pace by which the labor force had been growing in the years immediately before the pandemic (BLS 2024b). By contrast, in the nine months after PUA ended, the labor force surged by over two and a half million—three times as many as in the previous nine months and nearly two and a half times the pace of pre-COVID labor-supply growth. With the end of PUA benefits, workers were returning to the workforce. Surprised, anyone?

Yet as we saw in figure 10, the post-PUA return to the workforce did not include older American workers, and the question is why. “COVID shyness” may perhaps be a factor, but by now the overwhelming majority of older Americans have been vaccinated, have obtained some immunity through contracting the disease, or both. Some older Americans are being kept out of the workforce due to “long COVID” or the need to take care of others with COVID, but, according to the estimates in figure 8, these numbers are very small in relation to the magnitude of the drop in labor supply for men and women fifty-five and older.

One hypothesis for explaining the striking and still continuing drop-off in workforce participation for older Americans would concern what we might call “COVID-policy wealth effects.” Figure 16, which traces the inflation-adjusted net worth per household for the bottom half of US wealth holders from 1989 to 2022, provides some clues for this surmise.

For three decades—from the collapse of the Berlin Wall until the eve of COVID—real net worth for the bottom half of American households stagnated. This is not a pretty picture, but we need to keep it in mind. According to estimates from the Fed, the real net worth for these homes in the third quarter of 2019 was a minuscule 3 percent higher than it had been three decades earlier—despite the huge explosion of wealth in the United States over the interim. This is a disturbing and basic feature of the economy in modern America, and it deserves much further examination. This great wealth stagnation, for example, may help us understand the gathering populist sentiment in the United States during recent decades.

For our purposes today, however, I simply wish to make the point that net worth for the bottom half in America had been stagnating for decades before the COVID pandemic. Then, suddenly, after the onset of the COVID crisis, real wealth for the bottom half in America soared. Between the end of 2019 and the end of 2021, it very nearly doubled. That surge, as it happened, amounted to about $25,000 per household. Clearly, the sudden jump in wealth for the bottom half in America during these years was very largely the consequence of windfall savings from emergency COVID policies.

Now, the aforementioned average $25,000 windfall may not seem like a great lot of cash to some people. But if your net worth on the eve of the COVID pandemic had been $25,000 or less, it might seem like a great deal of money indeed—possibly even enough to influence decisions about staying out of the workforce or even leaving the workforce.

In 2019, right before COVID, one in four homes headed by fifty-five-to-sixty-four-year-olds had less than $25,000 in net worth. This was also the case for over a fifth of homes headed by men or women in their late sixties and for nearly a fifth of those in their early seventies (US Census Bureau 2022). In 2019, almost twelve million homes in America with less than an estimated $25,000 in life savings were headed by men and women fifty-five to seventy-four years of age. The welcome financial surprise that awaited so many of these homes from the COVID-policy windfall may have also been a factor in their withdrawal from the workforce. (More affluent older Americans may have left the workforce or continued their temporary retreat from it thanks to appreciation in the value of their asset holdings because of the Fed’s easy-money policy during the pandemic emergency.) One of the unintended consequences of COVID emergency policies, then, may have been to encourage a premature, and possibly unsustainable, retirement for a large number of older Americans. Further research is warranted to examine this question.

Still Recovering from Unintended Pandemic-Policy Consequences

Where do we go from here? The men-without-work phenomenon shows no sign of abating. The post-COVID labor supply will be under market pressure to return to equilibrium, which is to say, to revert to its pre-COVID trend. This means, among other things, an abiding demand for immigrant labor while the domestic labor supply seems hesitant or faltering. But we should recognize that the unintended shocks of COVID-emergency-rescue policies may be felt even longer in US labor markets than the tragic shock of the COVID pandemic itself.

This was fog-of-war emergency decision-making. I am not prepared to judge these on-the-spot choices with the advantage of hindsight.