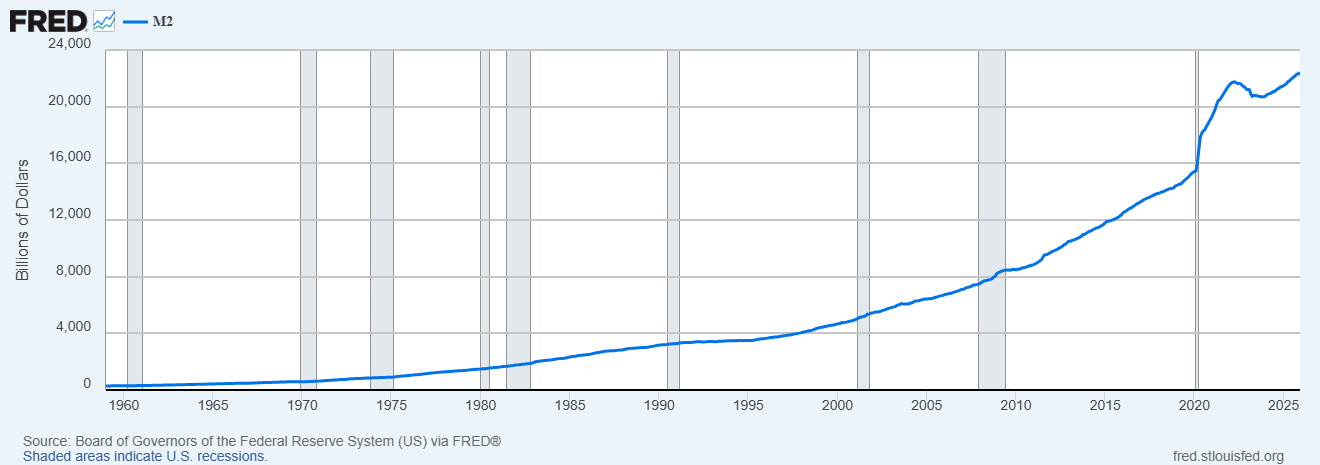

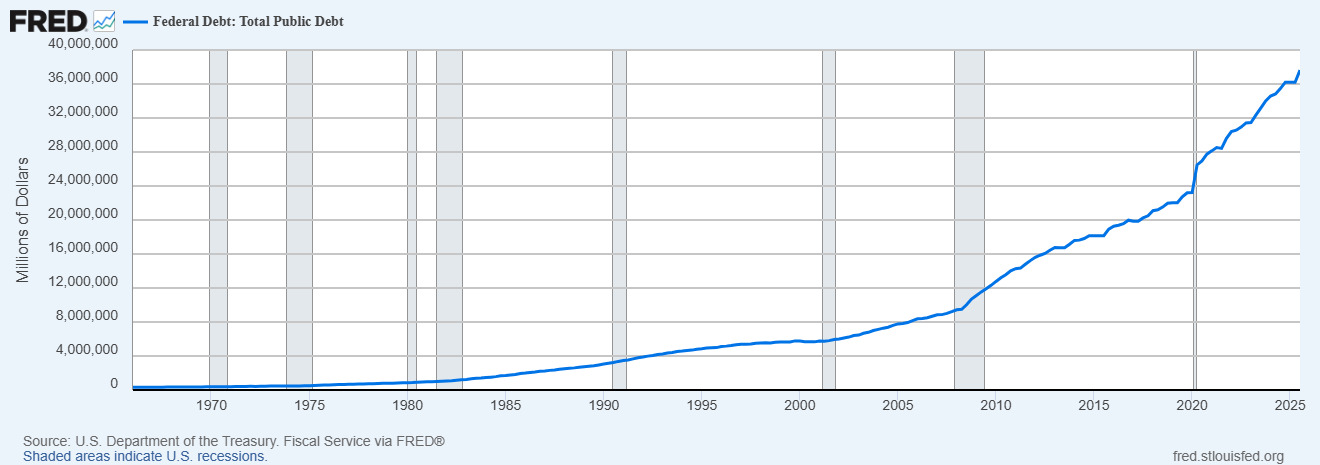

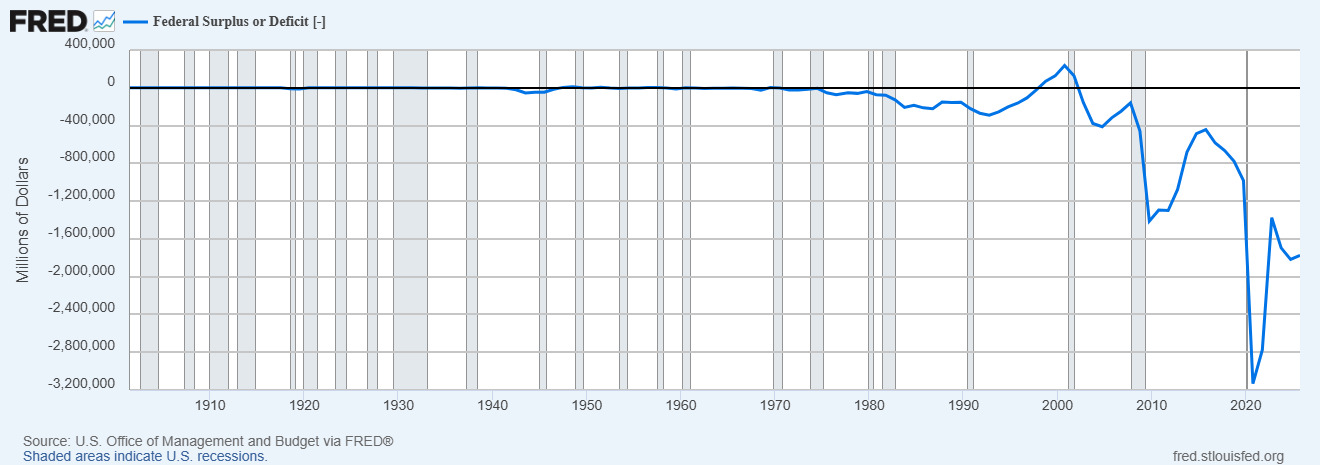

On August 15, 1971, President Nixon suspended the dollar’s convertibility into gold, thereby ending the last vestige of the international gold standard and ushering in an era of pure fiat money. Freed from any commodity restraint, the United States could now finance unchecked government expansion—and the relentless accumulation of debt—not through taxation or voluntary borrowing but through the monetization of deficits via inflation, producing unprecedented surges in money supply, federal spending, public debt, and structural budget deficits (see figures 1–3). The subsequent five decades witnessed a series of major US economic crises: the 1970s stagflation, the savings-and-loan debacle of the 1980s to the early 1990s, the 1990–91 recession, the 2000 dot-com bust, the 2008 housing and financial crisis, and the post-COVID surge in debt and inflation as well as bank failures in 2023.

Over this period the United States has shifted from the world’s largest international creditor in 1980 to its largest debtor nation (Aliber 2020), raising serious questions about the dollar’s long-term dominance as its share of global reserves steadily declines and nontraditional reserve currencies gain ground (Arslanalp et al. 2022). In short, despite the claimed theoretical advantages of a pure fiat currency, it is reasonable to wonder if the US economy would have performed better had the dollar remained under a commodity standard (see Hogan 2021; Askari and Krichene 2016; and Kydland and Wynne 2002).

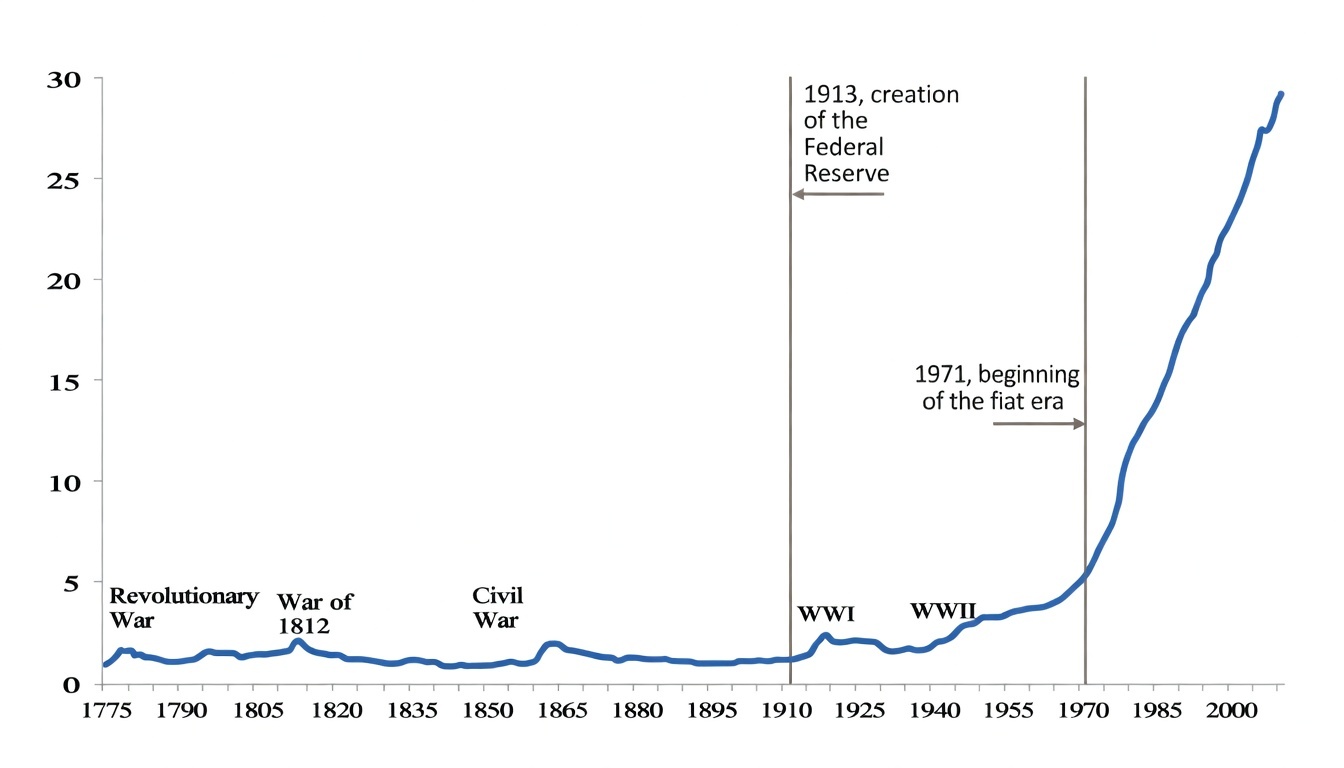

Developments in currency markets also cast doubt on the desirability of the current regime. The price of gold—a key barometer of monetary confidence—has surged to all-time highs, having risen by more than 60 percent in 2025 alone, as central banks have accumulated the metal in lieu of dollars; and they now hold more gold than US Treasuries for the first time since 1996 (McGeever 2025, fig. 1; World Gold Council 2025).[1] Meanwhile, the purchasing power of the dollar, which once exhibited remarkable long-run stability with some short-term, limited exceptions, has fallen more than 96 percent since the creation of the Federal Reserve in 1913, and especially after the nation’s break with the gold standard in 1971 (US Bureau of Labor Statistics 1947–2026; see figure 4).

.jpg)

In response to concerns about the stability and sustainability of the current monetary regime, various reforms have been advanced. These include proposals designed to strengthen fiscal discipline, permit the coexistence of alternative or competing currencies, or reintroduce a commodity-based monetary anchor. In particular, restricting monetary growth to a fixed rate (Friedman 1960) or adopting other rules-based monetary frameworks (Bernanke 2017) have received particular attention for their potential to enhance the credibility and discipline of central bank policy. At the same time, the possibility of returning to a gold or silver standard from a regime of fiat money has been studied, theoretically and practically, but often dismissed as infeasible, commonly on the grounds of the inefficiencies of a metallic standard, including prohibitive resource costs (Friedman 1960, 5); of concerns that it would induce excessive deflationary pressures (Eichengreen 1990); or of worries that it might be constrained by the supply of monetary metal required to sustain the needs of a large, complex economy (Fernández-Villaverde and Sanches 2022), among other objections.

Yet gold and/or silver have been reinstated successfully no less than five times in American history. The first reinstatement occurred in the colonial era, when the colonies were still under the rule of the British Parliament. The other four departures from commodity-based money were undertaken to facilitate the extreme government spending of the Revolutionary War, the War of 1812, the Civil War, Progressive Era government programs, and World War I. This history thus suggests that economies can, and do, return to commodity standards after periods of fiat money, and that reestablishing a gold standard in the United States may be less implausible than is commonly presumed.[2]

This article draws lessons from America’s experience with gold and silver that may help point the way toward a sounder monetary system. The nation’s historical episodes show that deviations from commodity money often followed a similar pattern of (1) price inflation, (2) a loss of confidence in the currency, (3) failed attempts to stabilize the currency, and finally (4) a reinstatement of sound money alongside reduced monetary interventionism, followed by significant economic recovery. More generally, these episodes of commodity money abandonment and reinstatement demonstrate how fiat money and economic central planning have made the nation vulnerable to chronic price inflation, business cycles, and economic crises.

Analysis of US Monetary History

Gold and silver were used as money in the United States from the early American period to 1971, but the country did not consistently uphold a hard-money system. Throughout its history, the United States has experienced six departures from sound money and, so far, five eventual returns to such a standard, albeit to varying degrees. What follows is a historical analysis of these periods, including the five reinstatements, with particular attention given to the fiscal motivations behind each departure and the monetary distortions that prompted a return to commodity money.

Episode 1: New England’s “Great Inflation” and the Original Reinstatement of “Hard” Money

By 1740, every colony except Virginia had issued fiat paper money.[3] It was the first use of paper money outside of China, and the practice was started in Massachusetts, where colonists initially used it to finance raids into the French colony of Quebec. In New England, fiat currencies inflated the stock of money by more than 24 percent per year (compounded annual rate) between 1743 and 1748, when those colonies issued paper currency to finance King George’s War, leading to an 11 percent annual rise in the price of silver (a well-established proxy for price inflation). It became such a problem that, in 1751, the British Parliament prohibited new issues of paper money throughout the region, barred the use of fiat currency as legal tender in private transactions, and ordered the redemption of the remaining fiat issues with metallic coins—rules that were imposed on the rest of the colonies in 1764 (Rothbard 2002, 53–56; Humpage 2015).

Contrary to predictions of economic collapse, the return to monetary restraint and market-based money enforced by a metallic standard led to greater prosperity and monetary stability. Murray Rothbard (2002, 53–56) notes that hard money and lower prices attracted an inflow of specie, fostering trade and rising real output; only dissenting Rhode Island remained on depreciated paper currency and suffered economic decline, thereby losing trade to neighboring Massachusetts. The reinstatement of metallic money[4] caused little financial disruption and worked well during the remainder of the colonial period, restoring economic confidence and stable exchange rates without intervention from a central government or central bank (Weiss 1970; Rothbard 2002, 54–55). Parliament’s action thus acknowledged fiat currency’s role in financing deficits and its potential to drive inflation, denoting an early recognition that the quality and quantity of currency matter (Humpage 2015).

Episode 2: The “Continentals” Fiasco, Boom and Bust, and Another Reinstatement

In 1775, the Continental Congress began issuing irredeemable paper notes to finance the Revolutionary War effort. The idea was that the states would levy taxes and collect the same notes in payment of those taxes, thereby retiring them. Unfortunately, the states never levied sufficient taxes, while the Continental Congress added roughly $225 million in “Continentals” to the existing money supply of about $10–12 million within the next five years (Rothbard 2002, 59; Bullock 1900, 64). The supply of paper money thus increased by roughly eighteenfold relative to the prewar money base in just a few years—a flood of new currency exacerbated by British counterfeiting designed to worsen colonial inflation and hasten the collapse of confidence in the Continental (Michener 2011; Rothbard 2002, 59–60).

Not surprisingly, the ensuing price inflation devalued the Continentals from the initial exchange rate in specie of 1:1 to 42:1 by December 1779, and to 168:1 by spring 1781 (Rothbard 2002, 59–60). In short, the currency suffered a near-total (99.4 percent) loss of value by 1781, demonstrating that, as Thomas Jefferson (1956) argued in a May 27, 1788, letter to Edward Carrington, “paper is poverty; it is only the ghost of money, and not money itself.” The Continentals and other state-issued paper monies that had been issued at the time were practically worthless (Rothbard 2002, 59–62, aligning with traditional historical estimates). They were “not worth a Continental,” as the saying goes, and economic chaos and dislocation followed. In attempts to prop up the failing currency, governments instituted price controls (Rothbard 2002, 60) and passed the first-ever US legal tender laws (Bullock 1900, 66), neither of which stemmed the devaluation of the Continentals. Fortunately, the president of the Continental Congress, John Jay, as shown in a circular letter he wrote to constituents on September 13, 1779, and other founders understood that “the moment the sum in circulation exceeded what was necessary as a medium in commerce, it began and continued to depreciate in proportion as the amount of the surplus increased. . . . The natural depreciation is to be removed only by lessening the quantity of money in circulation” (Jay 2010, 665).

Indeed, the disastrous experience with the Continental currency created such a “deep distrust of paper money issued by the government” that it prompted the nation’s founders to add the “gold and silver clause” to the US Constitution. The clause stipulates that the individual states could not issue bills of credit or “make any thing but gold and silver coin a tender in payment of debts” (U.S. Const., art. I, § 10, cl. 1). Gold and silver were soon reinstated as the nation’s sole legal money; Secretary of the Treasury Alexander Hamilton, with the concurrence of Secretary of State Thomas Jefferson—who had long advocated bimetallism and a decimal-based coinage—authored much of the Coinage Act of 1792 (also known as the Mint Act). The law established the US Mint, introduced a decimal monetary system, and restored a bimetallic standard defining the dollar as either 371.25 grains of pure silver or 24.75 grains of pure gold—a 15:1 ratio reflecting the metals’ contemporary market prices.[5]

The nation’s earliest leaders had turned to currency issuance to address the fiscal pressures of the Revolutionary War, resulting in hyperinflation, an enormous public debt of approximately $77 million (Hamilton [1790] 1962), and the Continentals’ demise. Unfortunately, while this economic outcome prompted a certain devotion to sound money in early America, expansionary monetary policy would remain a challenge in the years that followed. Indeed, a key component of Hamilton’s financial program, the short-lived First Bank of the United States (1791–1811), was chartered only a decade after the 1781 hyperinflation, ostensibly to mitigate a perceived “scarcity” of gold and silver coins in the economy. But the bank’s infusions of notes and deposit credit, albeit redeemable in specie on demand, led to an approximately 72–73 percent rise in wholesale prices by 1796, according to the Warren-Pearson Index (US Bureau of the Census 1960, 116, 119–21), fueling land and securities speculation and culminating in the contraction of 1796–97.[6] Thus, the nation’s first experiment with central banking produced a boom-bust cycle, and the First Bank was abandoned in 1811 as soon as its charter expired (Rothbard 2002, 68–72).

Episode 3: A Boom-Bust and the Third Reinstatement: The Jacksonian Gold Standard

When the nation confronted its next national emergency, the War of 1812, President James Madison resorted to printing unbacked money, sending the nation’s finances and economy back into turmoil (Todd 2012, 3). Madison encouraged the creation of new, inflationary banks in the western and southern states, which could in turn print new notes to purchase government bonds. The federal government used these notes to purchase war goods—particularly from New England, where support for both the war and expansionary banking was weak. A crisis emerged when New England bankers demanded specie redemption, which inflationary banks could not provide without facing insolvency (Rothbard 2002, 72–82). Suddenly, the nation’s finances became so disordered that the very operation of the federal government was threatened (Schur 1960, 119). After pleading by officials failed to persuade the state banks to resume specie payments, the federal government and some states, fearing that additional turmoil and losses to the Treasury would otherwise result, allowed the banks to stop redeeming their notes from August 1814 (when the British raided Washington) until February 1817 while continuing their operations (Hammond 1957, 228–47; Schur 1960, 119–20). The crisis had long-lasting historical implications, since allowing banks to suspend specie payments while continuing operations created an enduring moral hazard in the United States; as Rothbard (2002, 76–77) pointed out, by failing to enforce contract law and property rights, the government effectively encouraged inflationary expansion, undermining monetary stability.

During the nearly three years of the War of 1812, gold and silver money in bank vaults decreased by 9.4 percent, while paper banknotes and deposits increased by 87.2 percent (Paul and Lehrman [1983] 2011, 37). The resulting credit inflation generated a consumption frenzy that led to a surge in imports—from $13 million in 1814 to $151 million by 1816 (Dupre 2006, 280)—as well as to the nation’s first real estate bubble (Brands 2006, 66). In short, an “orgy of speculation, stock jobbing, and pursuit of luxury imports” had been created by 1815 (Maloney 2021). Finally, the nation’s leaders realized that the highly inflationary policy of the new central bank, the Second Bank of the United States,[7] would lead it to default on its own specie payment obligations. The bank then began taking heroically contractionary actions. By 1819, the Second Bank had contracted its contribution to the money supply by nearly half (47.2 percent), resulting in an overall money supply decline of 28.3 percent, after accounting for state bank and US Treasury reductions (Rothbard 2002, 89). A wave of defaults, bankruptcies, and investment liquidations followed, as did the nation’s first major economic depression. As economist William Gouge (1833, 119) put it, “The Bank was saved, and the people were ruined.”

The events surrounding the Panic of 1819 convinced the Democratic Party’s new leader, Andrew Jackson, that the nation’s expansionary monetary and banking policies had to be fought and roundly defeated (Rothbard 2002, 91–92). Once elected in 1828, Jackson went about enacting his program, including vetoing the recharter of the central bank in 1832 and achieving the full repayment of the US federal debt by 1835. As Jackson (n.d.) had explained in his 1829 first inaugural address, national debt freedom “will counteract that tendency to public and private profligacy which a profuse expenditure of money by the government is but too apt to engender.”

Central to the Jacksonian program as well was ending inflationary paper money and substituting it with either hard money or paper that was 100 percent backed by precious metals. Toward this end, the Coinage Act of 1834 readjusted the problematic mint ratio of 15:1, which had driven gold out of circulation, bringing it more in line with market prices (to approximately 16:1) and thereby back into use. In addition, the Jacksonians legalized the circulation of all foreign silver and gold coins, which then flourished in the marketplace (Rothbard 2002, 104–7).[8] Later, Jackson’s successor, Martin Van Buren, established the Independent Treasury System, under which the government conferred no special privilege or inflationary power on any bank and greatly restricted the government’s ability to borrow or monetize paper money for the purpose of financing public projects (Trask 2002, 1–10).

Despite these sweeping reforms, it should be noted that bank credit expansion was still tied to the public debt at the time, meaning that the more public debt banks purchased, the more money they could create and lend. The system essentially encouraged state governments to go into debt, and therefore government and bank inflation remained closely linked (Rothbard 2002, 113). Notwithstanding these flaws,[9] Jackson’s commitment to expunging political influence from the money supply demonstrated keen economic insight, and his war on the central bank was a “fully rational and highly enlightened” step toward the elimination of inflationary fractional reserve banking (Hummel 1978, 161). Moreover, the Jackson administration’s elimination of the national debt by 1835 has never been duplicated (US Department of the Treasury 1790–2025).

Indeed, Jackson and Van Buren laid the groundwork for an unprecedented, recession-free sixteen-year period of growth (1841–56), with per capita GNP surging between 1840 and 1860 by more than 30 percent, which is among the most robust rates of economic growth in American history. Without the intervention of a central bank, real per capita GDP grew at a 5 percent annualized rate between the mid-1840s and the late 1850s, while industrial production growth surged to more than 7 percent per annum (Davis and Weidenmier 2016, 7). Moreover, by the end of this period, analysts such as Gouge had identified the cause of the Panic of 1819 as an expansion of bank credit and of the money supply, and formulated a monetary explanation of the aftereffects: a rise in prices and a drain of specie abroad, culminating in contraction and depression. Further monetary expansion, they warned, would only renew this process and prolong the contraction necessary to liquidate unsound banks and reverse the specie drain (see Gouge 1833, part 2, chap. 3).

Episode 4: From Civil War Greenbacks to a Fourth Reinstatement: The Classical Gold Standard

Financing the Civil War would likely have been impossible for the federal government under a sound-money regime. As a consequence, by the final months of 1861, the Treasury and private banks had suspended specie conversions; the United States was subsequently off a metallic standard for almost twenty years. Instead, the Union government issued irredeemable “greenback” notes and outlawed state banknotes for the first time in the nation’s history. During the war years, the federal government also created a new, fractional reserve National Banking System, formally ending the separation of the federal government from banking and bringing the two institutions closer than ever. This new banking arrangement paved the way for the Federal Reserve by instituting a quasi-central-banking structure that allowed banks to pyramid credit on the same set of reserves, thus thwarting the competitive adverse clearing mechanism that previously limited excessive deposit and note issuance (Newman 2014, 487), leading to a boom-bust cycle that began with a 137.9 percent expansion of the money supply (US Bureau of the Census 1975, 625, 648–49)[10] and wholesale price inflation of 110 percent, or 22.2 percent per year (Andreano 1961, 178), from 1860 to 1865.

This greenback crisis led President Ulysses S. Grant to reaffirm hard-money principles during the economic contraction following the Panic of 1873. Amid intense political pressure from inflationist advocates, Grant vetoed the so-called Inflation Bill, which would have authorized additional greenback issuance. In his veto message, he argued that “paper money is nothing more than promises to pay, and is valuable exactly in proportion to the amount of coin that it can be converted into” (2 Cong. Rec. S3270–71 (April 22, 1874)). Instead, in 1875 he signed the Specie Payment Resumption Act, which reinstated the gold standard and began the removal of greenbacks from circulation, putting the nation back on a commodity money standard for the rest of the nineteenth century (Waugh, n.d.).[11]

After a transition period, gold-coin payments resumed at their prewar value in January 1879 and “banished all misgiving, for, when 1879 opened, only about $11 or $12 million worth of greenbacks were offered for redemption, while the Treasury at Washington had in its possession about ten or twelve times the amount in gold in its vaults,” according to reports from that era (Beach and McMurry 1901, 1792–93). Such was the successful transition to the classical gold standard era—a remarkable period in economic history lasting from 1879 to 1914 and characterized by “unprecedented economic growth” as well as the “free flow of labor and capital across political borders, virtually free trade, and, in general, world peace” (Bordo 1981, 7). The United States’ earlier, de facto gold standard, established when the Jacksonians passed the Coinage Act in 1834, was reinstated; and with the successful resumption of free coinage as well, anyone could take pure gold bullion in any quantity to an American mint and have it minted into gold coins, receiving $20.67, less certain petty charges for assaying and refining, for each ounce (Kemmerer 1944, 85, 103)—the same amount that had been received by citizens early in the century, and that would remain in place until 1934 (Kemmerer 1944, 129).

As a result, the gold premium to greenbacks fell to par, and the appreciated greenback promoted confidence in the gold-backed dollar. Capital investment surged, and American industry, production, and output expanded rapidly. Foreigners became willing to hold dollars again, and a rise in American exports and inflows of gold soon followed. In addition, the real costs of production declined and real, reproducible, tangible wealth per capita rose in the 1880s at an annual rate of approximately 3.8 percent, marking a decadal high in US economic history (Rothbard 2002, 159). The growth statistics of this period, like those of the Jacksonian era, are impressive (see tables 1 and 2 at the end of the article); and real wages rose by 23 percent between 1887 and 1889.[12] “No decade before or since produced such a sustainable rise in real wages” (Rothbard 2002, 162).

Indeed, between 1878 and 1889, the US economy—as measured by real GDP—nearly doubled (Domitrovic 2012); and by the mid-1880s, this expansion positioned the United States as the largest and most productive economy in the world (Bolt and van Zanden 2020).[13] Though growth in the economy outpaced growth in the money supply, the period actually saw a moderation, not an increase, of deflation. In fact, there was considerably less price deflation between 1879 and 1897 (annual Consumer Price Index decline of about 1.1 percent) than there had been in the years immediately preceding it, 1873 to 1879 (annual Consumer Price Index [CPI] decline of about 3.8 percent), when the United States was still on a fiat greenback standard (Johnston and Williamson 1790–2026). In addition, by the time the United States had re-embraced the marketplace’s commodity money, many of the major countries of the world had already adopted national monetary systems based on specific quantities of gold, creating a global gold standard that facilitated international trade with minimal, if any, central bank intervention. Gold was convertible at a fixed rate of exchange into the currencies of most nations, and the quantity of money in those countries adjusted to the amount of economic activity through the dynamics of supply and demand. A country’s adherence to gold convertibility was a sign of financial rectitude that limited incidences of inflation and sovereign default, enabling it to access capital at reduced borrowing costs—a property that rendered the gold standard largely self-enforcing (Bordo and Rockoff 1996).

After centuries of heavy taxation, feudal serfdom, and absolute monarchy, the classical liberal era produced a philosophy that championed limited government. During the 1800s, most Western countries’ spending averaged about 10 percent of GDP, and in the United States federal spending was about 2 percent (with the exception of the Civil War years; see International Monetary Fund 1800–2023).[14] In addition, just as the American Constitution was intended to restrain the arbitrary exercise of government power, the gold standard strictly limited the ability of a government to engage in inflation (Murphy 2011), protecting the purchasing power of money from political manipulation.

However, by the time of the Gold Standard Act of 1900, an interventionist political philosophy had begun to gain influence, ultimately bringing about the dissolution of the classical gold standard within fifteen years. Perhaps the most critical shortcoming of the era’s classical liberals was their failure to defend the privatization of the medium of exchange, for once the government gains control of money and credit, “from that point on it is no longer a matter of principle but one of expediency how far one wishes or permits governmental interference to go. Money control is the supreme and most comprehensive of all government controls short of expropriation” (Stolper 1942, 59). Consequently, monetary interventionism grew in the early decades of the twentieth century (Rothbard 2017; Ebeling 2008; 2020), setting the stage for the Progressive Era that followed.[15] “The government-controlled central banks and, in the United States, the government-controlled Federal Reserve System, were the instruments applied in this process of disorganization and demolition” (Mises [1912] 1953, 455).

Meanwhile, this classical gold standard still serves as the prime historical example of a successful monetary policy. Indeed, the economic record from 1820 to 1913 is remarkable: Marked by the rapid industrialization of that era, real GDP rose at an annualized rate of 4.1 percent in the US, more than 70 percent higher than any other nation during those years (Gallman 2000, 1–56). While some analysts have derided the 1800s as a period of booms and busts, the history surveyed above indicates that these cycles were not caused by sound money; indeed the famous busts of the nineteenth century correlated with departures from the discipline of gold.[16] “[The] 1819 [Panic] came on the heels of the severe overprinting and suspension of convertibility in the war years of 1812–15. Ditto 1873, likewise on the heels of severe overprinting and suspension of convertibility in the war years of 1861–65. And the Financial Panic of 1893 occurred just as the United States was monetizing in a major way a non-gold medium.[17] . . . Surely it was not the gold standard that led to the notorious and oft-invoked ‘cycle’ of boom and bust, but tiring of it that did” (Domitrovic 2012).

The “demolition” identified by Ludwig von Mises began soon after the turn of the twentieth century. Departing from the strictures of the classical gold standard, Congress in 1900 passed the Gold Standard Act, which formalized a single gold standard and ended the long debate over bimetallism, but also began the drive for greater currency elasticity by lowering capital requirements for national banks outside of the big cities and easing note issuance, thereby facilitating credit expansion. Along with contemporaneous agitation for centralized banking, the reforms marked an important early step toward greater monetary centralization and inflationary potential, eventually enabling US participation in the flawed international gold-exchange standards of the interwar period (originating at the 1922 Genoa Conference) and of the Bretton Woods era (originating at the 1944 Bretton Woods Conference), systems that permitted coordinated credit and monetary expansion under the guise of gold convertibility (Rothbard 2002, 202–34). The new standard, which emerged first in Britain (1925–31)[18] and culminated in the dollar-based Bretton Woods system (1944–71), allowed central banks around the world to maintain their reserves in a base currency (the British pound or the US dollar, respectively) with only those two nations able to redeem their notes directly for gold. For Britain and the United States, it meant that their monetary inflation would not necessarily entail losing gold to other countries. Meanwhile, other nations could inflate their own currencies on top of their expanding balances in British pounds or US dollars. The arrangement insulated Britain and the United States from the full disciplinary effects of gold outflows during periods of domestic monetary expansion, a flaw that ultimately led to both systems’ collapse (Bordo 1993; Rothbard 2002, 208–9).

The new monetary system would help finance the Progressive Era as well as the growth of myriad government interventions in the twentieth century, as would the creation of the Federal Reserve Bank in 1914. Cognizant of the increasingly unstable fractional reserve banking system that was developing early in the century, New York bankers sought a government-sponsored lender of last resort that would centralize reserves to prevent credit-expanding banks from getting caught short by the payment demands of sounder banks. Moreover, if bank panics and financial crises were to be avoided, they argued, the nation’s money supply would need to be more “elastic,” or inflationary. Given that a voluntary trade association would likely break down, the big banks realized they needed compulsory action to achieve their goals; and they successfully lobbied for what Rothbard (2017, 463–85) describes as the cartelization of the banking business in the form of the Federal Reserve System. The Fed’s monetary interventions would facilitate the increasingly ambitious spending projects of the twentieth century, while gaining the public’s passive endorsement of them. Indeed, the newly established Federal Reserve arrived in time to help finance US participation in World War I through expansionary policies that supported large-scale government borrowing (Friedman and Schwartz 1963, chap. 5; Rothbard 2017, 485). By monetizing Treasury debt and artificially lowering interest rates, the Fed allowed Congress to finance expenditures through inflationary means as well as through taxation.

Although a weakened classical gold standard stayed in place until May 1933, when Franklin Roosevelt issued an executive order banning the private ownership of gold, the early part of the twentieth century saw central banks and governments increasingly unwilling to accept the spending discipline required by gold convertibility; this paved the way for the final abandonment of a metallic standard (Bordo 1993). Without a mechanism to balance payments between nations and distribute gold throughout the world based on demand, Mises and many other economists of the time held out little hope for containing governments’ overspending. Gold had provided limits to politically engineered expansions of the money supply while allowing it to expand and contract as needed (via increases and decreases in gold mining) to meet the demand to hold it, stabilizing the purchasing power of money over time. The gold standard had worked so well because its implementation “render[ed] the determination of the monetary unit’s purchasing power independent of the policies of governments and political parties” (Mises [1912] 1953, 416). Mises’s predicted age of inflation thus came to fruition gradually over the course of the twentieth century: The seeming economic and monetary stability of the 1920s was followed by the Great Depression, driven by the Federal Reserve’s increasingly inflationary policy (Rothbard [1963] 2000);[19] and the ownership of gold, with few exceptions, would be illegal from 1933 to 1974, marking the definitive end of America’s gold standard era.

In summary, from the nation’s inception in the late 1770s to the mid-1930s, the United States mostly remained on either a gold or a bimetallic standard. Though government leaders and central banks repeatedly found reasons to abandon sound money, and with bad results, the nation always returned to a metallic standard. Remarkably, during that century and a half, the inflations caused by departures from sound money were almost exactly matched by an equal amount of price deflation so that the net effect during the period 1780 to 1935 was zero, with wholesale price index numbers at about the same level in 1935 as they were in 1780 (US Bureau of Labor Statistics 1635–2026).[20] Moreover, American real GNP increased about 175-fold between 1774 and 1909, an average growth rate of 3.9 percent per year. Higher rates than this have been recorded, but only for much shorter periods (Gallman 2000, 1–56). However, after the guardrails of sound money were lifted, the nation never saw a similar period again.

Episode 5: The Weak Fifth Reinstatement: The Bretton Woods Gold Standard

A decade later, the 1944 Bretton Woods agreement at the end of World War II was hailed as the return of gold-based monetary stability. In reality, as described above, it marked a profound departure from those ideals. Instead of restoring required redemptions in gold, Bretton Woods’ gold-exchange standard was in effect an international dollar standard that conferred inflationary powers to the Federal Reserve and other central banks while maintaining a loose connection to gold through the US dollar.[21] Because the dollar was defined as 1/35 of an ounce of gold while all other currencies were defined in terms of dollars rather than of a weight of gold, the system was doomed from the start.

Initially the system seemed to work well, especially for the United States, whose policymakers were able to issue more paper and credit dollars while the American public saw only small price increases. Although the supply of dollars increased and the US began experiencing balance-of-payments deficits, other nations were not cashing in their notes for gold (as they would have under an authentic gold standard). Rather, they accumulated dollars and pyramided their own currencies on top of them. In short, the US was for a time able to limit its own price increases by exporting its monetary inflation to other countries (Bordo 1993; Rothbard [1963] 2024, 115–18).

Unsurprisingly, in the 1960s hard-money countries began recognizing the inevitability of the dollar’s depreciation and demanded gold redemption at the official $35 price, depleting gold reserves. As many analysts have surmised, the US maintained a credible commitment to a noninflationary policy “for only a few years. By the mid-1960s it [had] shifted to an inflationary policy to further its domestic interests. The rest of the world, faced with imported inflation, soon lost the incentive to follow US leadership and the system began to collapse” (Bordo 1993). In 1968, the US government attempted a series of stopgap measures to stem the gold hemorrhage, but the runs on US gold intensified. On August 15, 1971, with the US economy stagnant and prices rising, President Richard Nixon “temporarily” suspended dollar-gold convertibility, severing the currency’s last remaining connection to gold. Subsequently, the price of gold began to rise, eventually precipitously (Macrotrends 1915–2025) as both the public and the central banks began buying the metal as an inflation hedge, affirming its continuing monetary role.[22] Appearances were maintained for some time,[23] but by 1973 the world had transitioned to the current system of fiat currencies and floating exchange rates (Rothbard [1963] 2024, 118–27).

The United States’ most severe and sustained levels of inflation and its largest financial crises thus occurred in the postmetallic, fiat-money era; conversely, the long-term price level was more stable and predictable on hard money, and particularly on the gold standard (also see Kydland and Wynne 2002), while GDP growth rates were higher and the volatility of real GDP growth was marginally lower; indeed, financial markets have been more volatile since 1971 (Hogan 2021).

Although the Federal Reserve did make some progress in subduing price inflation after the Great Inflation of the 1970s and early 1980s (Domitrovic 2012), the longer-run record of the fiat regime and central banking does not even remotely compare to the economic record under the gold standard. In fact, between 1969 and 2024, the average yearly inflation rate was about 4 percent (US Bureau of Labor Statistics 1635–2026), compared to the near-zero average of the classical gold standard period (1879–1914) before the interventions of the Federal Reserve (US Bureau of Labor Statistics 1635–2026; Dorn 2020).[24] The nation’s fiscal path also took on an unsustainable trajectory once gold’s constraints on spending were lifted (US Government Accountability Office, n.d.).

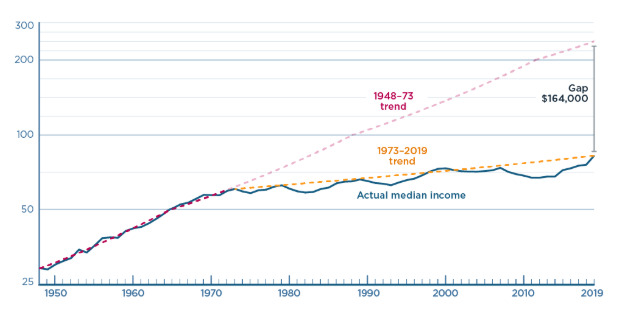

The reason for these outcomes lies in the inherent flaws of centralized monetary planning: As Joseph Salerno (1983, 243) argues, “Any scheme for politicizing and centralizing the decisions regarding the supply of the social medium of exchange is in fact merely a special application of the general case for the centralized planning of any sector of the economy and shares the widely-recognized defect of this case: The inability to contrive a serviceable replacement for the price system to rapidly and efficiently communicate massive amounts of widely scattered information to the planners.” Under the Federal Reserve’s discretionary direction, the US has moved progressively away from a market-based, commodity-backed currency with market-enforced reserve requirements and spending limits toward a fully fiat-money regime featuring fractional reserve banking and effectively no reserve requirements or fiscal restraints. As a consequence, it has experienced lower real incomes (see figure 5), excessive government debt and budget deficits, speculative booms and busts, rapid money supply growth accompanied by persistent price inflation, and widening wealth disparities (Askari and Krichene 2016, 30–31). Thus, the fiat system has arguably introduced significantly greater risks of prolonged instability than the self-correcting mechanisms of historical commodity standards (Kydland and Wynne 2002; Hogan 2021), even in their previously discussed imperfect applications.

.png)

Toward Sound Monetary Reform

After more than five decades of fiat money, the question naturally arises: How could the United States return to a sound monetary system? Previous analysis, including that of Lawrence White (2023; 2013) and Salerno (2010; 1983) have rebutted many of the common objections to a sound monetary standard, such as a supposedly insufficient amount of gold to operate a modern gold standard; the fear that such a standard would lead to secular deflation; and concerns that hard money would too rigidly tie the government’s hands and amplify business cycles. Building on this article’s historical survey and on prior scholarship, we next examine some practical considerations of such a reinstatement, drawing on historical criteria for successful sound-money standards that emerge from American monetary experience—from colonial fiat inflations to the classical gold standard era and beyond.

Criteria for Successful, Sound Monetary Systems

The most consistent characteristics of the monetary history surveyed above are that the US government has frequently resorted to inflationary policies, often to finance war or achieve other political goals (episodes 1–5); that this fiscal profligacy has invariably led to economic dislocations and crises; and that the pre–Bretton Woods periods (especially the third and fourth reinstatements) provided insulation from political control that was superior to the monetary eras that have followed, as well as better outcomes in terms of monetary and fiscal stability.

In addition, the record shows that periods during which the nation followed a rules-based commodity standard, especially the gold standards of the nineteenth and early twentieth centuries, have consistently yielded stronger growth, lower price inflation, and lower debt levels than those in which governments circumvented those hard-money constraints through inflationary finance and suspension of convertibility. Thus, market-disciplined commodity standards appear to constitute the strongest historically tested defense against inflation and government profligacy precisely because they are the only regimes that have substantially separated money creation from state power and discretion.[25] The first criterion (A) for a successful, sound monetary system is therefore a separation of money creation and management from state power.

A second, corollary criterion (B) is that the composition, quantity, and value of money must be determined exclusively by market forces. The most successful US monetary episodes (e.g., episodes 2 and 3) demonstrate that alignment of statutory ratios with prevailing market conditions promoted smooth adoption and operation of hard money. Free coinage and monetary freedom further reinforced success, as seen in the Coinage Acts of 1792 (15:1) and 1834 (about 16:1) (episodes 2 and 3), the Jacksonian reforms (episode 3) that legalized foreign coins, and the gradual 1875–79 deflation and resumption (episode 4). Indeed, while sound money does not necessarily require a silver- or gold-based monetary system, gold nevertheless “represents the money that emerged in the past from a natural selection process of the free market that spanned centuries” (Salerno 1983, 250).

A third important criterion (C) is that sustainable monetary regimes enforce and maintain fiscal discipline. Unlike fiat and gold-exchange systems, genuine metallic standards constrain excessive spending and deficit monetization naturally through market mechanisms (episodes 1–4), while political interventions associated with the other systems invariably fuel malinvestment and inflation-driven cycles (episodes 1–5). The market-determined interest rates of genuine gold or metallic standards likewise reflect genuine time preferences, discouraging overborrowing and aligning investment with savings (Mises [1949] 1998, 547–63).

Additional features that marked successful monetary periods or transitions include criterion D, the gradual implementation of sound-money policy after a prolonged abandonment of hard money (as in the 1875 Specie Resumption Act); criterion E, the nonexistence or end of central banking, as occurred during the Jacksonian era (see Rothbard’s 2002, 72–104, analysis); and criterion F, the return of the internationally effective, self-enforcing price-specie-flow mechanism of the nineteenth and early twentieth centuries, which automatically adjusted balance-of-payments disequilibria without discretionary intervention. In regard to this last criterion, adherence to gold also signaled fiscal and monetary rectitude, lowering sovereign borrowing costs and attracting capital inflows at reduced risk premiums (Bordo and Rockoff 1996).

Analysis of Monetary Proposals

Clearly, given the economic dislocation that has occurred during this latest episode of fiat currency (thirty years longer than the Civil War greenback experiment), we should expect the transition to any new monetary system to have its difficulties. To avoid those challenges, and in particular the supposed resource costs of implementing a new gold standard, Friedman (1960) supported a strict money supply rule that would mimic the automatically adjusting nature of a gold standard but would entail much lower costs. Unfortunately, despite theoretical appeal, such rules lack binding enforcement against political pressures, failing what is clearly the most important requirement of sound money, criterion A. Indeed, Friedman (1986, 642) later acknowledged that, while the costs of producing dollar bills are unquestionably low, his proposal’s real costs to society could be significantly higher “as a result of the decline in long-term price predictability”; in other words, as a result of the probable welfare costs of price inflation under a central bank.[26]

As Richard Timberlake (2014) later pointed out, the implementation of monetary rules such as the Friedman rule or the Taylor rule are subject to public-choice considerations: policymakers do not dispassionately pursue sound economic policy but instead are, like everyone else, motivated by their own self-interest. Salerno (2010, 334) explains that Friedman ignored the root cause of inflation: that the government has a monopoly on the money supply process. Instead of challenging the monopoly control of money, Friedman simply wanted the political authorities to be more restrained, a request which Salerno describes as “incredibly naive in the light of theory and history.” In stark contrast to that monopoly’s history, of course, banknotes and deposits under a gold standard would increase only as new gold flowed into the banks.

Given the lack of traction and impotence of monetary rules, then, what about a return to an actual gold standard based upon the historical success and experience of that system, both here and abroad? Several recent researchers have examined the feasibility of establishing a new gold standard,[27] one of them noting that “if a fiat dollar crisis is already happening, a return to gold may actually reestablish economic stability” (Skousen 2010, xxvi). A good example of a monetary crisis leading to a successful transition occurred in Ecuador during the 1990s. As inflation increased rapidly, the private sector began informally adopting the dollar, creating a parallel dollar-based economy between 1998 and 2000. In 2000, the government finally abandoned the Ecuadorian sucre and replaced it with the dollar, stabilizing the country’s monetary and banking systems. This transition reflected a Mengerian process, where decentralized market behavior and consumer choice effectively guided monetary reform (White 2012). Such a transition aligns well with private initiative and market rates (criterion B) and may lead to gradual reform (criterion D), but it initially lacks the remaining criteria.

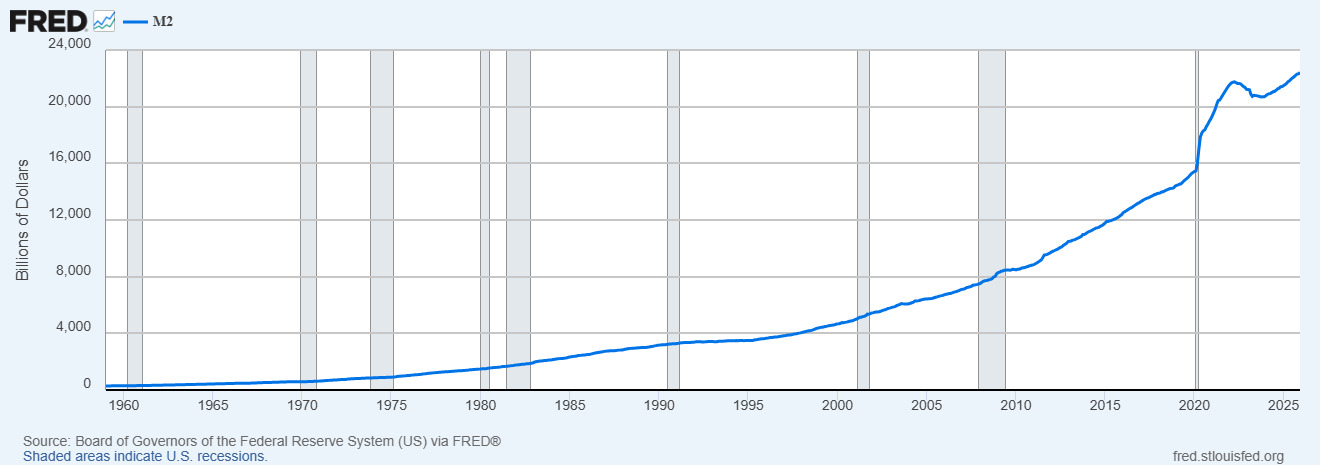

Another model for monetary transition involves setting a future date on which the conversion will occur. In 2001, for example, El Salvador shifted from a dollar-pegged exchange rate to the full adoption of the US dollar. At the time, inflation was low, and the local currency remained in widespread use, so the move was proactive instead of reactive. The data suggest that the transition resulted in lower inflation and interest rates, contributing to greater macroeconomic stability (Moran 2016, 20–21). The transition in the United States between 1875 and 1879 (episode 4) was similar, leading to the classical gold standard era. As previously discussed, a deliberate contraction of the money supply was undertaken at that time to restore gold convertibility at the pre–Civil War price. Though some have proposed revisiting this deflationary approach, it is not politically practical, as Rothbard ([1963] 2024) has argued.[28] The problem is that attempting to reestablish gold parity at outdated levels, especially at its statutory 1973 value of $42.2222 per ounce, at which it is still held in the nation’s vaults, would trigger severe deflation—likely much worse than what occurred when Britain went back to the gold standard in 1925 at the pre–World War I parity, causing painful deflation and severe adjustment problems in British labor markets (Morrison 2009). On the other hand, setting a new parity too high (to fully back the current money supply with existing reserves) could result in significant inflation. Indeed, accomplishing full gold backing today would not be feasible in light of the current M2 money supply of approximately $22.3 trillion (as of October 2025, the latest available monthly figure) (Board of Governors of the Federal Reserve System 1959–2025) and the nation’s roughly 8,133 metric tons of gold reserves (equivalent to about 261.5 million fine troy ounces) (US Department of the Treasury 2012–2026; World Gold Council 2025). Doing so would require a dramatic increase in the official price of gold—to roughly $85,000–$90,000 per ounce (depending on exact M2 and gold reserve figures used)—and would therefore lead to severe hyperinflation if implemented abruptly.[29] Using just the monetary base (about $5.3 trillion; Board of Governors of the Federal Reserve System 1925–2025b)—the sum of currency in circulation plus bank reserves held at the central bank—would still risk hyperinflation, requiring a gold price of about $20,500 (as compared to the current price of around $5,000).

Conversely, Friedrich Hayek ([1976] 1990) and White (2012), among others, have called for reform that begins with establishing freedom in monetary matters. Long before the advent of bitcoin, whose market dominance since 2009 emphatically demonstrates public demand for an alternative money, Hayek proposed the denationalization of money, a system in which private institutions would issue competing currencies (today, they might be cryptocurrencies), with any residual government money facing market competition. Market forces would determine the winners based on their stability in value. “Should the US inflation rate return to double digits, consumers would find it very helpful to have an alternative currency network available,” notes Lawrence White (2012, 420), drawing on the research of Gabriele Camera et al. (2004) highlighting the benefits of monetary denationalization and competition. White would like to see legal and regulatory changes that would grant citizens better and untaxed access to gold-, silver- or bitcoin-denominated banking services.

Some of the important, initial steps that could be taken in this direction include (1) ensuring the enforceability of contracts denominated in gold and other units besides fiat dollars by removing exclusive legal tender status from Federal Reserve notes and Treasury coins (a status which they did not have until 1933); (2) removing taxes on gold and silver coins, which the IRS currently classifies as “collectibles,” meaning that taxes on them can be higher than those on long-term capital gains; (3) removing sections of the US Code which have criminalized private minting of metal intended to circulate as money; and (4) allowing banks or other companies to issue gold-redeemable paper currency notes and token coins (White 2012). The case for a level playing field between the fiat dollar and other monetary standards rests on the simple proposition that the well-being of consumers is better served by market forces than by monopoly. In addition, the emergence of monetary competition would incentivize the Fed to maintain a less inflationary monetary policy. These steps thus represent a clear advance toward monetary freedom via a market-determined, gradual implementation (meeting criteria B and D), although they don’t immediately reestablish a historically chosen commodity money.[30] Indeed, while such parallel-money proposals end a significant amount of the government’s monetary intervention (criterion A) and offer a path to market-enforced monetary and fiscal discipline (criterion C), they don’t necessarily offer the disciplinary benefits of commodity anchoring and therefore do not provide the automatic specie-flow mechanism of historical gold standards (criterion F), although it should be noted that Hayek expected commodity-backed currencies to win in the marketplace. Finally, while Hayek and White offer critiques of fractional reserves under monopoly money (criterion E), they would allow them competitively under their plans, believing that fractional reserves might potentially curb excesses via market discipline.

In short, while the denationalization framework may yield a bitcoin or bitcoin-like standard with anti-inflationary and disciplinary advantages similar to those of historical commodity standards (and firm independence from state abuse), the end result could lack metallic money’s nonmonetary demand anchor, natural supply elasticity (via mining), and proven long-term stability. These plans also overlook the great advantage fiat dollars currently have in competition with alternative potential moneys and do not consider the broader political and institutional changes required for a durable sound-money regime. As a result, they imply a passive stance[31]—waiting for the eventual breakdown of the current system without a clear strategy for shaping the subsequent monetary framework, as Kristoffer Hansen (2020) and Jörg Guido Hülsmann (2008, 241) have argued.[32]

Alternatively, Judy Shelton (2024) proposes an intermediate gradual conversion to gold through the issuance of Treasury zero-coupon securities. Dubbed Treasury Trust Bonds, the securities would offer lower interest rates than conventional Treasuries (thus reducing current deficits) and be redeemable either at their face value in dollars or at a prespecified equivalent in gold at the buyer’s discretion. In other words, should monetary policy continue on its current path and the dollar’s purchasing power decline significantly, this could result in a significant loss of US government gold. But if the United States straightens out its finances, most of the bonds would likely be redeemed in dollars. Shelton argues that this “trust-but-verify,” mechanism would create a foundation for sound money, potentially spurring broader reform, perhaps even resulting in a new, gold-based international monetary system. This proposal creatively incentivizes fiscal discipline and gradualism (criteria C and D), but it initially lacks the remaining qualities (i.e., criteria A, B, E, F) of successful monetary periods.

A transitional plan less reliant on hope and much more comprehensive, however, was designed by Mises ([1912] 1953, 435–52) and has been further elaborated by Hansen (2020). This plan stands out for two reasons: Rather than taking on the difficult task of figuring out the correct legal par between dollars and gold, the proposal leaves it to the marketplace to determine the correct gold price. And rather than backing the entire money supply with gold all at once, it promotes a free and sound monetary marketplace by focusing on halting all further inflation—whether created by the government or by the banks—immediately.[33] As a result of this phased implementation, the plan would be much less likely to cause economic dislocations than the types of plans requiring more abrupt conversions.

The moment this new policy was enacted, any new issue of currency would be backed 100 percent by gold held by the government. While the total quantity of money in the economy would not be backed 100 percent by gold reserves immediately (which would be very difficult to achieve, for the reasons outlined above), savers would know that from the date of the reform all additions of currency would be fully backed. As Mises explained ([1912] 1953, 448),

The first step must be a radical and unconditional abandonment of any further inflation. The total amount of dollar bills . . . must not be increased by further issuance. No bank must be permitted to expand the total amount of its deposits subject to check or the balance of such deposits . . . otherwise than by receiving cash deposits in legal-tender bank notes. . . . This means a rigid 100 percent reserve for all future deposits; that is, all deposits not already in existence on the first day of the reform.

Once the market price of gold had stabilized, that price would be decreed the new legal parity for the dollar, and additional currency would then become convertible at this parity.[34] The Treasury Department, not the Federal Reserve, would accomplish this reform with the goals of stabilizing the value of the dollar and facilitating the circulation of the new notes and coins. Indeed, the government would initially make no effort to bulk up on its gold holdings; rather, it would passively accept gold deposits from those who wished to obtain newly issued dollars in exchange for gold at the official peg.

Thus, all inflationary activity would be halted immediately, as would boom-bust business cycles, and the system would promote sound money going forward. Like Hansen, Robert Murphy (2011) sees Mises’s scheme as a “nonarbitrary and sensible approach, yielding two desirable outcomes: First, the government would not need to absorb a large fraction of the stock of gold from the private sector early on. Second, as the quantity of domestic currency expanded over time, a larger and larger fraction of the currency would be backed by gold.” Notwithstanding the immediate use of modern technology that would facilitate buying, saving, and spending gold digitally, a central goal would be to allow physical metals to circulate as money again, thus connecting money back to its commodity origins while making Americans better aware of the benefits of “hard” money and the perils of monetary inflation.[35] Additional elements of the plan have been elucidated or modified for the modern economy by Hansen (2020), including the eventual elimination of all unbacked Federal Reserve notes by allowing the marketplace to establish a slight premium for gold over paper dollars.

In summary, Mises’s reform plan excels in multiple areas, conforming with the historical criteria for successful monetary regimes: It provides insulation against further monetary interference and inflation (criterion A); reinstates the marketplace’s historically chosen money and allows the marketplace to set the price of gold (B); and sets the monetary system on a path toward market-enforced monetary and fiscal discipline (C). It also entails a gradual implementation, thus allowing for a smoother transition (D); and ends the inflationary powers of the Federal Reserve (E).[36] Furthermore, its adoption by the United States, which remains the dominant monetary power in the world, would likely lead to its gradual international adoption and an accompanying, self-enforcing monetary discipline (F), particularly given that other nations’ central banks already appear to be preparing for this possible outcome.[37]

Although there are certainly many details to be worked out, the point of delineating some of the key features of this plan and others is to demonstrate that there are viable paths forward to the reinstatement of a gold or sound monetary standard—even if they require further study and do not represent immediate, perfect, or painless solutions. Indeed, although its end goal is the reestablishment of a free-market monetary system in the United States and abroad, the Mises plan, as elaborated by Hansen (2020), does not immediately sever the link between the government and money or end the problems associated with fractional reserve banking or fiscal profligacy.[38] Nevertheless, it represents an economically feasible and substantial step toward an orderly withdrawal of paper money and the reintroduction of gold into the US monetary system, not to mention an enormous positive change in the direction of market money and sound economics—the reason that many economists in the Austrian tradition have regarded the reestablishment of a gold standard as a prudent and constructive institutional reform (Murphy 2011).

Moreover, it is encouraging to note, as the historical review above has demonstrated, that the nation’s history is replete with successful reimplementations of sound money. Indeed, American history yields no reason to believe that a genuine reinstatement of sound money would not work in the present era as well. Rather, among US monetary regimes, commodity or “hard-money” standards are the only ones that have consistently delivered long-term stability and prosperity (Lewis 2017, 246).

Conclusion

The recent surge in gold’s dollar price signals eroding trust in the world’s reserve currency, with gold clearly reclaiming its historical role as a monetary asset (CBS News 2025). As Carl Menger ([1892] 2009, 51), who underscored money’s market-driven essence, explained, this dynamic emerges organically from individuals selecting the most marketable medium of exchange, not from government decree. “Man himself is the beginning and the end of every economy,” wrote Menger (8). Yet US history reveals how government interventions in the money supply—favoring political agendas over monetary stability—have eroded the national well-being. According to Hayek ([1977] 2019), “To put [the monopoly privilege of issuing money] into the hands of an institution which is protected against competition, which can force us to accept the money, which is subject to incessant political pressure, such an authority will not ever again give us good money.”

Is a return to commodity money or a gold standard—long considered by a wide swath of economists to be the most effective means of making the “determination of the monetary unit’s purchasing power independent of the ambitions and activities of dictators, political parties and pressure groups” (Salerno 1983, 50)—feasible after five decades of fiat dominance and record debt and deficits? Skeptics cite technical and political barriers, but US monetary history demonstrates repeated success in restoring gold- and silver-based standards after prolonged fiat failures. These monetary episodes reveal a pattern: Fiat regimes tend to fuel inflation, balloon debt, weaken currencies, and breed instability, culminating in recessions. By contrast, reinstatements of sound money, paired with restrained intervention, have reliably restored stability and spurred recovery. Under the pre-Fed classical gold standard, stable prices and exchange rates fostered innovation, wealth creation, and free trade (Rockoff 1990; Dorn 2020); inflation’s maladies “persist under fiat regimes, but not under the classical gold standard, where private banks’ promises to convert paper money into fixed quantities of gold were strictly enforced” (Selgin 1999, 23).

Certainly, the lesson from the American experience is that any durable new monetary order will require the reinstatement of market discipline, not discretionary central control. Building on history’s insights and criteria, and with gold’s recent ascent suggesting a growing Mengerian shift toward sound money, US policymakers ought to consider practical strategies—such as Mises’s elegant gradualist framework—that can reimplement a sound monetary regime to safeguard the nation’s economic stability. Returning to such a system may be more feasible than most monetary economists, government officials, and the public realize.

Tables

The data in tables 1 and 2 illustrate the correlation between the reintroduction of a gold standard and marked gains in output, productivity, and real wages, coinciding with declining or stable prices.

As the tables indicate, the most pronounced and sustained periods of real economic growth and rising wages occurred during intervals of price stability and metallic restraint. Periods of heavy monetary expansion, by contrast, consistently coincided with inflationary booms followed by contraction and real-income losses. These patterns are consistent with the view that monetary stability fosters stronger long-term real economic performance than managed inflation.

Global central banks shifted from net sellers of gold in the late twentieth century to net buyers beginning about 2010. In 2018, the volume of purchases marked the highest level since the end of the gold standard era, with over 650 metric tons purchased; and it reached a record amount of more than 1,000 metric tons annually between 2022 and 2024 (World Gold Council 2025). The share of gold in central bank reserve allocation increased by 50 percent between 2019 and 2024, from an already material 10 percent of reserves to nearly 15 percent. By mid-2025, gold represented about a quarter of international central bank reserves, up from below 10 percent in 2015 (see Bertaut et al. 2025, fig. 3).

As of August 2025, twelve US states have recognized gold and silver as legal tender, reflecting rising interest in alternatives to the dollar and concerns about inflation or federal monetary policy (LegalClarity 2025).

Virginia followed in the late 1750s to help finance the French and Indian War.

These were mostly silver dollar coins originating in the Spanish Empire (Babones 2017).

Unfortunately, the workings of Gresham’s law meant that as each metal’s respective price changed in the marketplace, the undervalued coin would be driven out of local circulation and increasingly saved for uses in which the exchange laws did not apply (i.e., in foreign trade). So as silver production increased in subsequent years, gold coins became increasingly rare by 1820 (Rothbard 2002, 67–68).

Rothbard (2002, 70) notes that the First Bank and its monetary expansion fueled the creation of eighteen new commercial banks in five years, aggravating the paper money expansion.

The Second Bank of the United States (1816–36) followed the expiration of the First Bank (1791–1811). Under the Second Bank, crude open market operations were initiated whereby the bank bought or sold state banknotes to loosen or tighten credit conditions (Rothbard 2002, 68–69; Todd 2012, 4).

This action remained in effect through 1857, when Congress overturned it and ended the legality of the original Colonial-Era coin, the aforementioned Spanish silver “dollar” (Rothbard 2002, 49).

Free coinage (under which individuals could bring gold or silver bullion to the US Mint and have it coined into legal tender money, typically for only a small fee to cover minting costs, continued uninterrupted during the Jacksonian period. Legal tender was extended to foreign coins, but not to private coinage. In addition, banks of the era were continually allowed to suspend specie payments during financial crises, a longstanding problem leading to lower reserve ratios. The prohibition on interstate branch banking was also maintained (Hummel 1978, 153, 155, 160–61).

Paul Auerbach and Michael Haupert (2002, 65) figure that the monetary base, or high-powered money (currency held by the public as well as reserves held by banks), increased by 144 percent between 1858 and 1865, from $3.7 billion to over $9 billion.

For the moment, Grant transformed his party into the party of sound money and fiscal restraint (Waugh, n.d.).

From the beginning of 1875 until specie payments were resumed on January 1, 1879, the money stock contracted by about 8.6 percent and prices fell by almost 4 percent, even as GDP averaged an outstanding 5.2 percent growth rate. These facts bring into question the conventionally held connection between falling prices and real output, but they also suggest that fiscal deflation actually contributed to the sharp growth rate. “Real resources that had been absorbed in wasteful uses by government or in propping up business malinvestments precipitated by previous bank credit expansion were now released . . . to be more efficiently allocated by entrepreneurs responding to the anticipated demands of fellow producers in the social division of labor” (Salerno 2003, 96).

Long-run GDP series compiled under the Maddison Project suggest that by the early 1880s, the United States overtook the UK in GDP per capita, achieving a lasting lead by around 1900 (Bolt and van Zanden 2020).

Today, government spending equals about 40 percent of GDP in the United States, and that figure is typically lower than that in other advanced economies (Trading Economics, n.d.).

Milton Friedman (1961, 78) wrote that a pseudo–gold standard of this type “violates fundamental liberal principles in two respects: First, it involves price-fixing by government. . . . Second, and no less important, it involves granting discretionary authority . . . to the central bankers or Treasury officials who must manage the pseudo-gold standard. This means the rule of men instead of law.”

Rothbard (2002, 153–55) explains that the financial panics of 1873, 1884, 1893, and 1907 were in large part caused by the National Banking System’s reserve pyramiding, leading to excessive note and deposit creation.

Congress had passed the Sherman Silver Purchase Act (1890), requiring the Treasury to buy large amounts of silver and issue Treasury notes redeemable in either silver or gold. This effectively expanded the money supply by monetizing silver (a nongold medium) at a time when many creditors and investors preferred strict adherence to the gold standard. The worry was that silver’s market value was falling relative to gold’s, so monetizing silver risked driving gold out of circulation (the dynamic of Gresham’s law). By 1893, these tensions helped trigger a financial panic and a deep depression, as Thomas Klitgaard and James Narron (2016) explain.

The British gold-exchange standard ended with a worldwide banking crash and the general shift toward fiat paper money that began in the early 1930s (Rothbard 2002, 232).

Most mainstream economists also blame Fed policy for causing and/or deepening and prolonging the economic downturn following the late 1920s, albeit for wholly different reasons. According to Milton Friedman and Anna Schwartz (1963, chap. 7), the Great Depression was caused by the Federal Reserve’s failure, through overly restrictive monetary policy, to prevent a collapse in the banking system and money supply.

This is not to imply that this price stability was constant throughout the entire period, as the monetary survey above should make clear. For example, performing this same calculation from 1780 to 1928 (which was the last year of the inflationary period preceding the Great Depression), yields an annual inflation rate of 0.15 percent per year—or a cumulative price increase of nearly 25 percent. Many of the resulting malinvestments had clearly been corrected by 1935. Of course, even the 25 percent figure pales in comparison with the 708 percent cumulative increase in prices that occurred between 1970 and 2024 (US Bureau of Labor Statistics 1635–2026).

The Bretton Woods Conference also created two new international institutions—the International Monetary Fund (IMF) and the World Bank—intended to promote economic stability and finance postwar reconstruction.

While gold ownership was technically illegal for US citizens between 1933 and 1974, individuals still found ways to buy and hold gold as an inflation hedge. This was primarily done through international gold markets and alternative investment vehicles that indirectly involved gold. The rapid price increase debunked the notion that gold’s official demonetization would lead to less demand, lower prices, and lower economic resource costs. On the contrary, demand exploded and the price of gold had reached as high as $850 by January of 1980 (Macrotrends 1915–2025).

Official acknowledgement that the dollar was no longer based on gold did not come until October 1976.

Arthur Rolnick and Warren Weber (1997) found, more generally, that countries experienced lower inflation rates and less money growth while on a gold standard than under a fiat-money system.

As Carmen Reinhart and Kenneth Rogoff (2009) have demonstrated, this inflationary impulse is a recurring pattern across eight centuries of governance. States have repeatedly engaged in excessive borrowing, leading to debt crises, defaults, or inflationary episodes, and often using high inflation (or historical currency debasement) as a covert form of default on their obligations.

Also see Roger Garrison ([1985] 1992), White (2019), and Bryan Cutsinger (2020), who argue that the resource costs of today’s fiat system may be higher than they would be on a gold standard.

Several recent analyses examine aspects of how a gold standard could be effected or would perform in a modern monetary framework. These include Skousen (2010); Askari and Krichene (2016); Cutsinger (2020); Hansen (2020); Fernández-Villaverde and Sanches (2022; 2024); White (2023); Shelton (2024); and Ammous (2025).

Rothbard ([1963] 2024, 110) rejected deflationist policy as a means of deflating a nation’s currency back to a previous par value against gold, as Britain did after World War I much less successfully (National Archives (UK), n.d.): “The sensible thing to do would have been to recognize the facts of reality . . . and to return to the gold standard at a redefined rate: a rate that would recognize the existing supply of money and price levels.”

While this is a problematic ratio for a monetary conversion, it nevertheless does not imply an insufficient stock of gold (or silver) for a reinstatement. As many have pointed out, once the market selects a commodity as money, its existing stock is always sufficient for money’s functions. Like other goods in a free market, money’s price (exchange value) adjusts via supply and demand: scarcity raises the price of money, and abundance lowers it. Thus, there can be neither “too little” nor “too much” money—as long as markets clear freely, no shortages or surpluses arise (Salerno 1983).

Mises ([1912] 1953) set forth the regression theorem, which explains that the value of money can be traced back (or “regressed”) to its use-value as a commodity, pointing back to gold (or, more broadly, precious metals) as the marketplace’s chosen money.

Robert Greenfield and Leland Yeager (1983) have advocated a less passive approach, requiring major institutional change, whereby the government would be prescribed a single monetary role: defining a stable unit of account based on a comprehensive commodity bundle so as to maintain a near-steady general price level; private institutions would handle the supply of media of exchange. This separates creation and supply of money from the state and aims to satisfy criteria A and C, but if the government retains any involvement in its management (e.g., via bundle selection), fiscal discipline would be undermined (and the plan would fail criterion B). It does not meet criteria D, E, or F.

Dollars would fulfill “the primary purpose of money better than the alternatives. Since prices are expressed in dollars, it is much easier to continue to use the incumbent money rather than speculate on some other commodity that might in time become widely used as a medium of exchange” (Hansen 2020, 339).

Banks’ adherence to this framework would depend upon regulatory enforcement. Robert Murphy (2025), skeptical that the government would effectively regulate banks for the purpose of ending fractional reserve banking, advocates backing only the monetary base (i.e., government-created money) with gold—rather than the broader M1 or M2 aggregates (which include bank-created deposits)—since ideally the Fed, its lender-of-last-resort function, and FDIC insurance would all be abolished in concert with this plan, thus allowing private competition to discipline the banks.

The reason the plan is likely to work is that there is no reason to think that the whole dollar stock would be presented for redemption at once: Rather, “the dollar will . . . improve considerably in quality once all inflation stops and redemption in gold is resumed.” Thus, “an orderly withdrawal of paper money and its substitution with gold will be possible, and the Treasury will be able to gradually buy up gold in the market as necessary to redeem all dollars as they are presented” (Hansen 2020, 349).

A disappearance of coins from circulation would then alert citizens to the reimposition of monetary inflation. Today’s price of gold would make small gold coinage almost impossible, but silver and copper (without a fixed exchange rate) could possibly circulate as money as well in Hansen’s (2020) plan.

Murphy (2025) has conjectured about how the closure of the Federal Reserve Bank could be effected; see note 34.

Today, central banks’ growing preference for gold reserves—$4.5 trillion in gold versus $3.5 trillion in US Treasuries as of September 2025 (McGeever 2025)—signals market convergence toward gold amid inflation and geopolitical risks.

Toward this end, a balanced budget amendment reinforced by additional fiscal constraints would bolster Mises’s reinstatement plan by imposing firm limits on government spending and deficits—particularly during the shift to full gold convertibility. Rothbard ([1979] 2011) argued that such an amendment could curb deficits and inflation only if paired with deeper measures, including major federal income tax cuts, abolition of the Federal Reserve’s inflationary powers, and further rules or amendments to block evasion through tax increases or “emergency” exceptions. A Swiss-style debt brake (see Macovei 2024) would similarly bind future policymakers and support sound-money objectives, as Brancu and Brancu (2025) contend in their analysis of Japan’s debt crisis.