A large body of literature in economics analyzes the economy in terms of information or knowledge. In mainstream economics, much ink has been spilled on the implications of relaxing or rejecting the “perfect information” assumption in general equilibrium theory. This has facilitated several important contributions to the literature. For example, transaction cost economics is based on the assumption of actors’ imperfect and asymmetrical knowledge of market prices (e.g., Coase 1937) and the costs arising from contract incompleteness (e.g., Williamson 2010; Klein and Shelanski 1995);[1] endogenous growth theory submits that investments in human capital, innovation, and knowledge are significant drivers or causes of economic growth (Romer 1986; 1987; 1990; Lucas 1988); and evolutionary economics (e.g., Hodgson 2019), explicitly building on Schumpeter (1934; 1947), finds in new technological knowledge a core explanation for industrial development (Nelson and Winter 1974; 1982).

In Austrian economics, knowledge also plays a prominent role and is often referenced as cause or explanation for economic phenomena and processes. For example, F. A. Hayek (e.g., 1937; 1945; 1978) famously explained that the price mechanism has an informational role in aggregating and communicating “very important but unorganized . . . knowledge of the particular circumstances of time and place” (Hayek 1945, 521). Israel Kirzner similarly argues that entrepreneurship is constituted by “alertness” to and thus discovery of existing price discrepancies (Kirzner 1973) that entrepreneurs can exploit—“errors” (Kirzner 1978) in the market that they can correct—thereby bringing about equilibration. Whereas Austrian economists are generally much better than mainstream economists at specifying what they mean by knowledge and its role or function, the concept is still used in several different—and often still too general, vague, and unspecific—ways, with the result that the economic implications lack specificity.

This is problematic, because knowledge can potentially have distinct meanings and different effects, and it can thus generate different understandings of economic processes and predictions. Knowledge may also evolve over time as learning takes place and events uncover or even generate new information about the state of the world. Consequently, for knowledge to be a theoretically useful concept, it needs to be deconstructed to distinguish between specific effects.

In this article, I address and deconstruct the concept of knowledge as it is used within the corpus of Austrian economics. I draw from the works of the Austrian masters, primarily Carl Menger and F. A. Hayek, to clarify the meanings and functions of knowledge in economic theorizing. Specifically, I create a typology of economically relevant knowledge that distinguishes between types of knowledge based on their respective economic uses and implications throughout the production structure.[2] Not only does the typology offer increased specificity that helps clarify and unpack generic references to “knowledge” in Austrian economics—thus shedding new light on prior theorizing and facilitating new theory development—but the deconstruction of knowledge types based on their respective temporal availability in the production process allows for the separation of knowledge from uncertainty for the economic actor. Specifically, by applying the temporal extension of the knowledge typology, it becomes evident that one of the types of knowledge is not (and cannot be) available at the time of action and thus causes uncertainty in the outcome of the action. The theoretical and practical significance of this conceptual temporal separation comes to light in the application of the typology to Austrian theories of the market process. The application clarifies the scope and economic relevance of knowledge problems as opposed to uncertainty, suggests demarcation criteria for economically relevant uncertainty, and raises questions about potential exaggerations of the impact of knowledge problems in Austrian theory.

KNOWLEDGE IN AUSTRIAN ECONOMICS

Knowledge has played an important role in Austrian economics since the publication of Carl Menger’s Grundsätze der Volkswirtschaftslehre. In his initial discussion of what constitutes an economic good, Menger (2007, 52) writes the following:

If a thing is to become a good, or in other words, if it is to acquire goods-character, all four of the following prerequisites must be simultaneously present:

A human need.

Such properties as render the thing capable of being brought into a causal connection with the satisfaction of this need.

Human knowledge of this causal connection.

Command of the thing sufficient to direct it to the satisfaction of the need.

The term “knowledge” only appears once in Menger’s list, but each of the points suggests a need for knowledge of some kind: An actor must recognize—that is, know of—his need before he can act on it and must know about the thing available and its relevant properties, which in turn allows him to form knowledge of the causal connection between the need and the means to satisfy it. Furthermore, he must also know his own ability to use the thing as a means to satisfy that end—what Menger refers to as “command of the thing.” Menger’s respective points suggest that the followings kinds of knowledge are necessary for a thing to be recognized as an economic good: (1) knowledge of the need and the value of satisfying it; (2) knowledge of the thing and its utility; (3) knowledge of how the thing can serve as a means for satisfying the need; and (4) knowledge of the ability to use the thing for the purpose of satisfying the need.

We can immediately identify a difference between these four aspects of knowledge based on what realm they refer to. Points 1 and 4 are knowledge that is specific to the individual and that cannot easily be known by anyone else. The actor’s valuation and assessment of (if not belief in) his ability are both in the subjective realm since they refer to knowledge of one’s self. In contrast, points 2 and 3 relate to the external world, specifically the physical nature of the thing and, therefore, its uses and usefulness. Mises (2003, 185; emphasis in original) corrects Menger by arguing that points 2 and 3 should be combined as “the opinion of the economizing individuals that the thing is capable of satisfying their wants,” which adds a subjective dimension to our understanding of the external world.[3] But whether value is attained from the good ultimately depends on the correctness of this “opinion” and consequently whether it is in line with the facts (and, thus, with knowledge). It is indeed in the intersection of the two realms, where the actor’s subjective valuation and beliefs meet his understanding of the external world, that a thing acquires the character of a good and thus becomes relevant to action, economizing, and economics itself. However, despite indicating that knowledge is important for—if not prerequisite to—action, Menger neither elaborates on nor attempts to explain how actors gain the knowledge they need for economizing actions.

Hayek asks and attempts to answer this question of “how knowledge is acquired and communicated” (Hayek 1948, 33) in “Economics and Knowledge” (1937). Answering this question would allow us to understand what causes change to individuals’ knowledge, which in turn should help us explain how and when their actions become coordinated in the market. Echoing the two types of knowledge implied in Menger—internal and subjective (points 1 and 4) and external and objective (points 2 and 3), respectively—Hayek notes that the core issue in empirical economics is “the relation of the thought of an individual to the outside world, the question to what extent and how his knowledge corresponds to the external facts” (Hayek 1948, 47). Unlike Menger, Hayek is not here interested in the actor’s subjective value or how action is influenced by the physical properties of the external world but in the actor’s understanding of the present economic situation and, especially, how accurate this understanding is—that is, whether it “corresponds to the external facts” (by which Hayek means the present economic circumstances or market data).

In fact, Hayek’s distinction between subjective and objective knowledge lies entirely within the economic sphere. He thus finds that “the really central problem of economics as a social science” is the one of “how the spontaneous interaction of a number of people, each possessing only bits of knowledge, brings about a state of affairs in which prices correspond to costs, etc., and which could be brought about by deliberate direction only by somebody who possessed the combined knowledge of all those individuals” (Hayek 1948, 50–51). With Hayek, therefore, we have taken the step from the individual’s personal recognition of a thing as an economic good—as explained by Menger (2007)—to the economizing interplay of producing actors on the social level (“the economy”). This leveling up creates a knowledge problem due to actors’ different understandings of the specific circumstances they are in. Specifically, the economic problem concerns how the dispersed bits of knowledge—the “external facts”—that actors have attained, or otherwise have access to, can be aggregated so that existing knowledge in toto can rationally direct production in the economy without causing contradictions or inefficiencies.

In “The Use of Knowledge in Society” (1945), Hayek distinguishes between three types of knowledge relevant to economic practice: scientific knowledge, which constitutes theory and “knowledge of general rules” (521); practical or local knowledge, which is the “special knowledge of circumstances of the fleeting moment not known to others” available to the “man on the spot” (522); and tacit knowledge, which is based on intuition and experience and plays a core role in Hayek’s argument against central planning because it, much like the knowledge of how to ride a bicycle, “cannot enter into statistics and therefore cannot be conveyed to any central authority in statistical form” (524). Scientific knowledge, or formal knowledge of the external world, is unproblematic from an economic perspective since it is generally available to (or at least acquirable by) all actors and only indirectly relevant to economic action—that is, it must be applied to be useful and offers no guidance to its proper economic uses (Mises 1935). In contrast, practical and tacit types of knowledge relate to economic practice, which causes the “peculiar character of the problem” of economics.

The issue for Hayek (1945, 519) is that “a rational economic order is determined precisely by the fact that the knowledge of the circumstances of which we must make use never exists in concentrated or integrated form but solely as the dispersed bits of incomplete and frequently contradictory knowledge which all the separate individuals possess.” Hayek (521–22) further notes that “it is with respect to this [knowledge] that practically every individual has some advantage over all others in that he possesses unique information of which beneficial use might be made, but of which use can be made only if the decisions depending on it are left to him or are made with his active cooperation.” Although dispersed practical knowledge is problematic, tacit knowledge cannot at all be communicated or aggregated, which poses an insurmountable problem for central planning. The central plan must consequently be formulated without information about the needs and possibilities of the economy, and production must thus be organized without it, which makes it fundamentally arbitrary if not irrational. It is not, however, merely a matter of access to this existent information but also its timely transfer and availability such that the central planner can address “the economic problem of society [which] is mainly one of rapid adaptation to changes in the particular circumstances of time and place” (524). It is when circumstances change that centrally planned systems really suffer, because not only do they then have incomplete (perhaps severely so) information but they also lack the means to aggregate, access, and act on such information. As a result, the economy’s production structure becomes misaligned with the facts.

In contrast, markets have no central plan but consist of the distributed actions taken by actors using their firsthand knowledge of economic particulars. This solves the problem of “rapid adaptation” to changes since “the ultimate decisions [are] left to the people who are familiar with these [particular] circumstances [of time and place], who know directly of the relevant changes and of the resources immediately available to meet them” (Hayek 1945, 524). Markets are superior to central planning because market-based production does not suffer as much of a knowledge problem—in other words, “fuller use will be made of the existing knowledge” (521). Markets must instead overcome a coordination problem since people acting on local knowledge may push in different directions and their undertakings—their production plans—can require mutually exclusive uses of scarce resources. Thus, actors need access to economically relevant and actionable data beyond what they know about their local circumstances. These data are communicated through the price mechanism:

The whole acts as one market, not because any of its members survey the whole field, but because their limited individual fields of vision sufficiently overlap so that through many intermediaries the relevant information is communicated to all. The mere fact that there is one price for any commodity—or rather that local prices are connected in a manner determined by the cost of transport, etc.—brings about the solution which (it is just conceptually possible) might have been arrived at by one single mind possessing all the information which is in fact dispersed among all the people involved in the process. (526)

Coordination, therefore, is an emergent phenomenon in markets—a bottom-up, unplanned order—based on actors’ local, dispersed knowledge and their economic actions informed by it. These actions in turn generate appropriate responses to changing circumstances that ripple through the economy in the form of price changes. Because production decisions are made locally and take local information into account—changing the structure of supply and demand and therefore prices of both production factors and consumer goods—the market as a whole can adapt to new relevant information without needing specific knowledge of a particular change.

DECONSTRUCTING KNOWLEDGE

Our discussion has shown that knowledge plays a central role in Austrian economic theory but also that the term is used in various ways. This presents to us an opportunity: We can leverage these specific uses of knowledge that refer to its effects and role in the economy to identify general categories of knowledge used by Austrian economists. This, in turn, will allow us to deconstruct the concept to clarify and provide greater nuance to Austrian explanations and economic theory. The purpose here is to shed light not on the nature of knowledge per se—that would be the task of philosophers—but on the economic import already recognized in the literature. We are interested in the uses of the term knowledge in relation to our understanding of economic production.

A Typology of Knowledge in Economics

Menger’s distinction between the objective (i.e., external, physical) and subjective (i.e., value-based, economic) realms is instructive and largely overlaps with Hayek’s own distinction—in particular that between scientific and other types of knowledge. We label this objective category physical-world knowledge since it encompasses objective, measurable facts about the external world amassed through, for example, scientific study or personal experience. It encompasses the economic actor’s grasp of how the physical world works and, therefore, how it can be used or exploited.

There are two aspects of the physical-world category of knowledge. One exists in the form of theories that can be developed through scientific experiments and systematic observations—general knowledge that actors can learn through formal education or independent study. This type of knowledge is typically generated and communicated through academic research and publishing, in textbooks and databases, and as the subject matter of formal education. It consists mainly of developed and corroborated theories, models, and explanations built on or tested against amassed facts about the world. General physical-world knowledge is commonly generated using the scientific method (see, e.g., Popper 2005). Hayek’s scientific knowledge captures this subtype, as does Menger’s knowledge of the thing and its utility (point 2), which consists primarily of the observation of the thing’s objective properties.[4] The other aspect is applied physical-world knowledge, which comprises Menger’s knowledge of how a thing can serve as a means (point 3)—that is, the specific thing’s utility in a particular situation—and the local knowledge of noneconomic circumstances—that is, the physical world that Hayek’s “man on the spot” can acquire and make use of. Whereas general physical-world knowledge establishes truths about the world, applied physical-world knowledge establishes how those truths can be used to create certain outcomes. It adds a practical dimension or know-how that applies and implements general knowledge by making it practicable and actionable in a specific present situation.

To illustrate, scientific knowledge would comprise the general knowledge established by the theories of physics and chemistry, and these can be converted by more specific disciplines, such as architecture and engineering, into applied practices that create things such as buildings and bridges. Applied knowledge builds on and adds a practical dimension—an application—to scientific knowledge. The general theories, along with their more specific elaborations, are instructive but must be applied to be useful and actionable. To simplify the distinction, general physical-world knowledge refers to theories and data explaining how the physical world works—for example, the mechanics of planetary systems and the properties of steel—whereas applied physical-world knowledge involves the practice of making the world useful—the rules, practices, and technologies that add content and specificity to the general theories to make them actionable and useful in the real world.

In contrast to knowledge of the external world, catallactic-world knowledge refers to the economizing uses of factors and goods. Economizing is not about the utility or efficiency of materials, such as the strength of steel or combustibility of gasoline, but the value they can be used to create. Economizing actions are based on choices between alternatives—their trade-offs or opportunity costs—and are fundamentally directed toward attaining the greatest subjective satisfaction possible given the means available. In other words, they are based on, informed by, and ultimately directed toward Menger’s concept of a personal knowledge of a need and the value of satisfying it (point 1). But production and trade in an economy are directed not toward the individual’s own consumption but toward maximizing want satisfactions on a social level—that is, the well-being or standard of living of a population or subset of it—which is the economic problem addressed by Hayek.

Production in a money economy—our primary interest here—is not a self-sufficient action à la Robinson Crusoe prior to the arrival of Friday. It is instead based on the separation of supply and demand in the market per Say’s law (see, e.g., Kates 2003; 2021). The producer engages in the production of goods to satisfy some subset of consumers willing to pay a price in excess of production costs, thereby earning the producer profit. The entrepreneur, as the ultimate decider of what is to be produced, is here a servant of the consumer, whose value attained determines the success or failure of the entrepreneur’s undertaking. Consequently, how resources are allocated and what types of production are undertaken with the limited means available are guided, if not directed, by a conception of the expected market value of the outcome. Naturally, physical-world knowledge plays a part as well, but, economically speaking, productivity is not a measure of how much physical product can be generated from some given quantities of inputs (technological efficiency). Rather, it is about getting as much value as possible from scarce, and therefore costly, means. These distinct issues are related in practice because production is undertaken to facilitate value; however, whereas the physical-world knowledge sets limits to what can be done, the economic dimension—catallactic-world knowledge—decides what should be done and how (Mises 1935). What should be produced is a matter of the imagined value of the goods considered; how goods are produced concerns the selection of the appropriate production structure or technology—that is, the appropriate means of value creation for keeping costs sufficiently low. It is in this latter activity—the how—that actors gain an advantage from Hayek’s tacit economic knowledge of the “particular circumstances of time and place” and where there may be economizing gains for the “man on the spot” with knowledge of effective economic practices. Such “bits of knowledge” become embedded in the production structure as general adjustments arise via the price mechanism in response to locally informed actions, which in turn improves overall economic output.

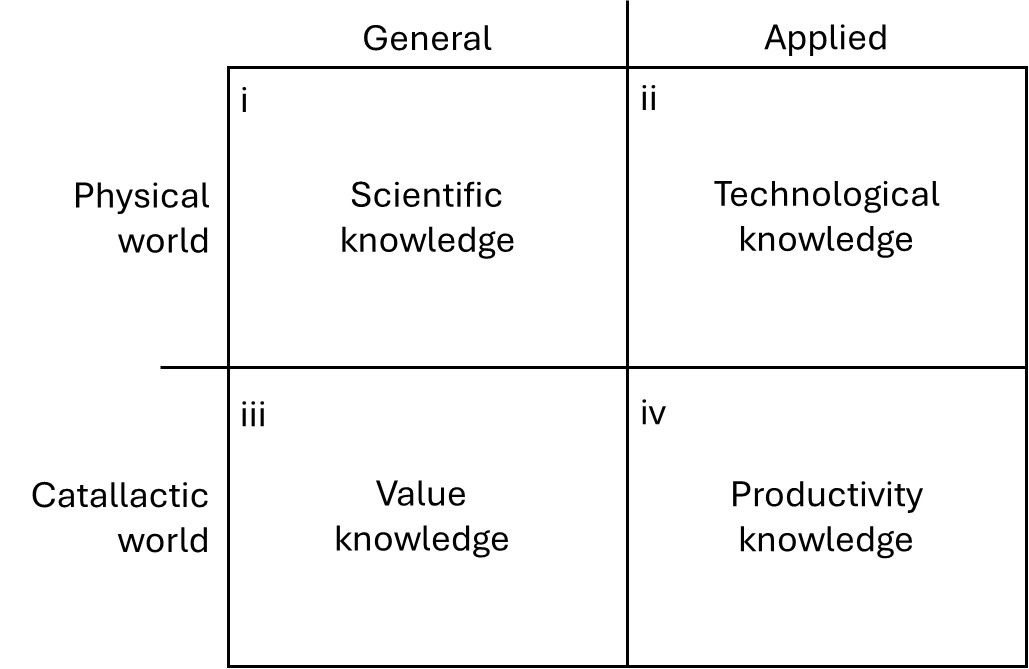

Consequently, we can organize knowledge as within either the physical world or the catallactic world and of either the general or applied kind. Figure 1 captures the differences.

The labels in figure 1 may require further explanation. The “scientific knowledge” of quadrant i is Hayek’s term for general theories of the physical or external world discussed above. It contains general knowledge about how the world works, including worked-out mechanics and explanations of phenomena, typically established through research or scholarship. What we here call “technological knowledge” of quadrant ii includes the general theories of how the world works put into practice toward specific ends such as the construction of buildings, bridges, or consumer products. Physical-world knowledge thus captures both our academic understanding of the world (quadrant i) and the applied practices of this understanding (quadrant ii).

Catallactic-world knowledge specifies types of knowledge relating specifically to economizing production and, therefore, the ranking of alternatives based on value. The value knowledge of quadrant iii refers to the satisfaction of wants for the consumer of a good—the value facilitated—and, in decentralized markets, the monetary market value of some type of production. In terms of market production decisions—and for our present purposes—the “value knowledge” of quadrant iii most importantly refers to the present value of an undertaking’s revenue—that is, its discounted value product (Rothbard 2004, 456–58). The productivity knowledge of quadrant iv, although applied and seemingly materialist, is distinct from the formal knowledge of quadrant i and the practical expertise that applies it in quadrant ii. Rather than the technological effectiveness or efficiency of machines and materials, productivity knowledge refers to the use of fundamentally economic production knowledge, such as the productivity of the division of labor, the use and development of capital goods, the choice of inputs, and production volumes that minimize average cost. It captures effective practices in the economization of scarce means to produce valued output. Productivity knowledge is informed as well as limited by naturalistic knowledge and its application through technology, but it is directed by expectations of value (in outcome and through factor prices).

It should be noted that consumers also rely on forms of knowledge in their decision-making—for understanding both the utility of goods offered for sale and how to satisfy their specific wants. But our interest here is the economic problem of production, which in markets aims to facilitate but is ultimately separate from consumption. This is also where we find the knowledge problem for which central planners have no solution, as addressed by Hayek.

How the Types of Knowledge Interrelate

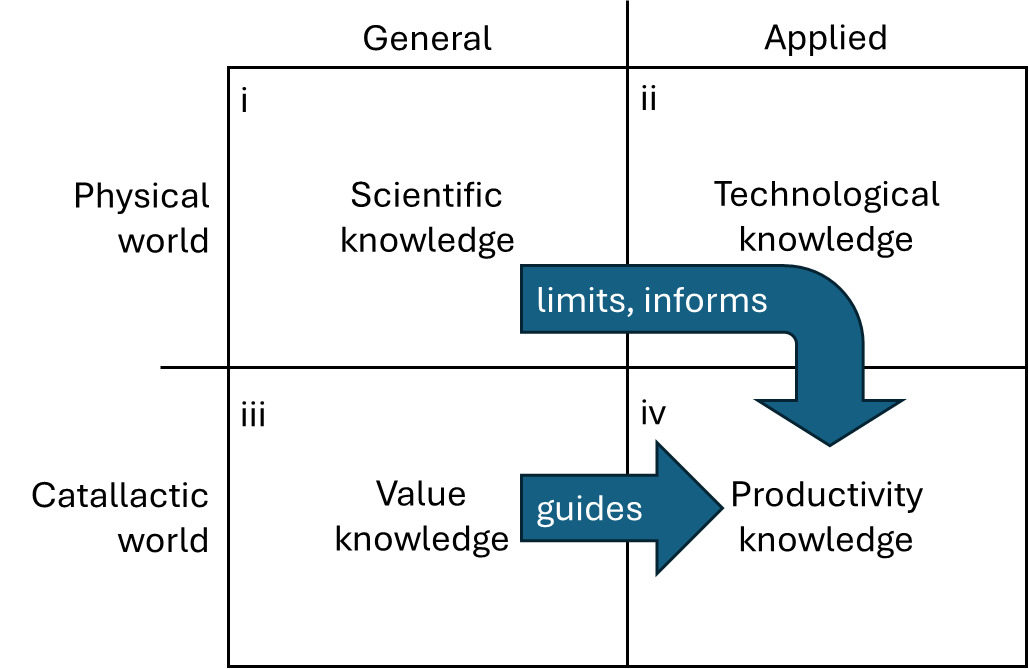

Whereas deconstructing knowledge into four types adds clarity and nuance to the relation between knowledge and economics, the value of this exercise becomes apparent when we elaborate on how the types of knowledge interact and interrelate, which in turn adds depth to economic explanations. We have already established the relationship between general and applied types. The former provides the general rules, if not the framework, for the applications of the latter. In other words, applied knowledge follows from, is informed by, and is more specific than general knowledge. Thus, the technological knowledge in quadrant ii applies, and is in this sense dependent on, the general theories that comprise knowledge in quadrant i. Without scientific knowledge, technological knowledge would be ad hoc, unreliable, and ineffective since it would be limited to personal and shared experiences—and it could easily fall victim to poorly understood practices and even superstitions. For example, the treatment of disease prior to the development of germ theory, immunology, and medicine was a practice based on applied knowledge without a proper foundation in general knowledge. General physical-world knowledge typically provides boundaries for applied knowledge, but the relationship is in effect bidirectional in that unexplained yet effective practices can motivate scientific study. From our perspective of economics, and specifically economic production theory, the primary role of scientific knowledge consists in limiting and informing the development of technological knowledge. This is illustrated in figure 2 as the arrow from quadrant i to quadrant ii.

We find a similar relationship within catallactic-world knowledge, where the value knowledge in quadrant iii directs and serves as a guide for the decisions made with respect to economizing production technologies in quadrant iv. Indeed, decisions to undertake specific kinds of production—whether of a novel and previously untried good or an already developed and traded good—are ultimately based on the value thereof and the calculations of the expected profitability of the enterprise (which, in turn, are based on the market value of the undertaking). For entrepreneurs and managers, value motivates the undertaking of production but is limited by the costs of production.

The relationship between physical-world and catallactic-world knowledge primarily relates to production practice—specifically, to how the theories explaining the physical world and their application in technological knowledge can (and should) be applied in effective production directed by value-based economizing. As already mentioned, physical-world knowledge provides insight into what is possible to produce and how it can be accomplished. It provides knowledge of both the effectiveness and efficiency of certain production choices and technologies, but it lacks entirely the value dimension and thus provides no guidance on how to rank or choose among alternatives. Consequently, the arrow in figure 2 indicating the relationship between general and applied physical-world knowledge is extended down to productivity knowledge. The effect is the same vertically as it is horizontally: Technological knowledge limits and informs productivity knowledge but acts only as input in economizing production decisions. Although informed by physical-world knowledge, productivity knowledge is ultimately guided by the value of the production undertaking and the costs of production.

Figure 2 illustrates the relevance of types of knowledge from the perspective of producing economic goods—that is, it illustrates how each of the types relates to economic action. Going left to right in the figure, the relationship between scientific and technological knowledge captures the distinction between the scientist and the practitioner (researcher, on the one hand, and engineer or builder, on the other), whereas the catallactic world knowledge captures the distinction between value-orientedness and productivity concerns (i.e., production management). Physical-world knowledge provides the setting and determines what is possible within the catallaxy.

THE TEMPORALITY OF KNOWLEDGE

The typology of knowledge and its abstract relationship between general and applied types is straightforward and easy to understand, but there is a major difference between the physical-world and catallactic-world categories that requires elaboration. Indeed, this difference comprises the main economic problem according to Austrian economics, which can only be solved through the process of economic calculation and its generation of real market prices that guide entrepreneurs in their decision-making (Mises 1935; 1951). This problem arises due to the strict temporality of the economy, captured by the specific relationship between value and productivity knowledge. Menger’s definition of an economic good implies the nature of this relationship: The consumer determines a thing’s character as a good based on its ability to satisfy a held (and known) want. Indeed, value, writes Menger (2007, 115), is “the importance that individual goods or quantities of goods attain for us because we are conscious of being dependent on command of them for the satisfaction of our needs.”

This is comparatively unproblematic when a consumer assesses and ranks a good already available for consumption. It is similarly unproblematic when the consumer decides whether and how to produce for his own consumption—for example, in an autistic or Robinson Crusoe economy (see, e.g., Rothbard 2004, chap. 1). In both cases, the person choosing the action and experiencing the value is the same, which means the want is directly known and the subjective value of satisfying it largely knowable. The actor may be wrong about the intensity of the satisfaction he will experience from satisfying the want, how to properly satisfy it, or the good’s ability to provide satisfaction. But these errors may be minimized over time through consumptive learning from experience (Witt 2001; Packard 2022).

The real problem arises in catallactic economies where the producer and consumer are not the same person and supply and demand are separated in accordance with Say’s law. Since value as experienced by the consumer (want satisfaction) is subjective and cannot be known by others, the producer must make decisions about production without knowing the extent to which consumers will value the product. But subjective value determines the consumer’s willingness to pay for the good and therefore also its market price (Bylund 2022; 2025). Thus, at the time of production, the producer cannot establish whether and to what extent the consumer will consider the product to have the character and value of a good, and therefore he cannot establish their willingness to pay for it.[5] In other words, the value knowledge that guides production decisions is unattainable at the time the decision to produce is made. More precisely, the value knowledge does not yet exist, because the value will be determined by the consumer when he has the choice to purchase a good to consume.

Adding temporarily to our typology of knowledge requires that we distinguish between knowledge available or potentially available in the present—when the production decision is made or production is underway—and knowledge that is available only after production has concluded. Knowledge in quadrants i (scientific knowledge), ii (technological knowledge), and iv (productivity knowledge) are all available, albeit imperfectly, in the present and therefore provide the producer with relevant information for production decisions. Value knowledge, however, is neither available nor obtainable at the time the production decision is made or production is underway, but it will be generated when the consumer formulates an expectation of value obtainable from the good (his want satisfaction) and therefore his willingness to pay for it (the market value). Consequently, value knowledge in our typology is nonactionable in specialized production economies, because it is a result of production—that is, it is an outcome of actions taken prior to the knowledge of their value.

This suggests a paradox, because, according to our typology, value knowledge guides economizing production: Production undertakings economize on means based on the value that the means are used to produce. But how can value knowledge guide production that must precede the existence of this type of knowledge (Bylund 2022; 2024; 2025)? Since value knowledge does not exist when production decisions must be made, the consumers’ valuation of production undertakings is unknown, unknowable, and therefore uncertain for the decision-maker. This raises the question, What distinguishes knowledge problems, which involve ignorance or the lack of knowledge, from uncertainty? We will attempt to distinguish these in the next section.

IGNORANCE AND UNCERTAINTY

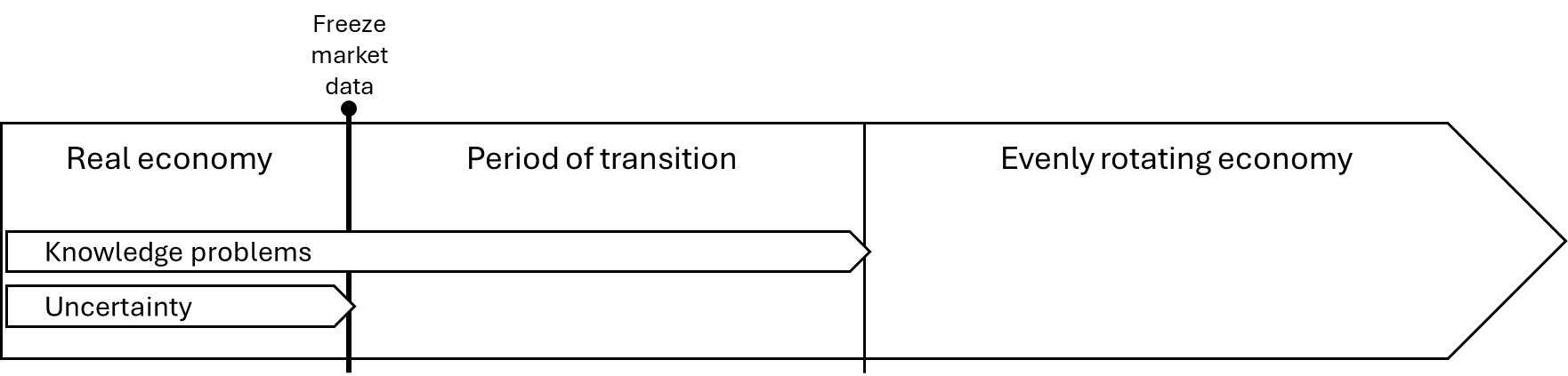

The temporal distinction between existing but not necessarily perfect knowledge, on the one hand, and knowledge that does not yet exist and cannot be generated, on the other, is of great importance in economics and economic practice. Superficially, these may be seen as similar problems or even the same problem—in general terms, consisting of a “lack of knowledge”—but they are, in fact, economically distinct. As illuminated by our typology, the former is best understood as a knowledge problem because it concerns ignorance of some facts about the external world (the imperfect knowledge of quadrants i, ii, and iv). The latter is the problem of uncertainty, which concerns the unknown and unknowable conditions of the future. To distinguish between imperfect knowledge in the present (knowledge problems) and the unavailability of future knowledge (uncertainty), we will make use of Mises’s evenly rotating economy (ERE). In this equilibrium-style model, unexpected changes to market data, which would require “rapid adaptation” for economizing production,[6] are excluded—and therefore so is uncertainty (Mises 1998, 245–51; Rothbard 2004, 320–29). The ERE “is characterized by the elimination of change in the data and of the time element” (Mises 1998, 247) and allows us to answer the question, “What would occur if value scales, technological ideas, and the given resources remained constant?” (Rothbard 2004, 321). In the ERE, actors can make full use of their local and tacit knowledge (Hayek 1945) in pursuit of their own well-being without being burdened by the uncertainty of outcomes and future conditions.[7] The ERE thus allows us to trace the tendency and final state of rest (equilibrium) of the economy.

Given constancy in market data, an economy will first enter a “period of transition” (Rothbard 2004, 321) as actors discover which of their available alternative actions produce the best possible outcome. This will cause “kaleidoscopically changing situations” (Mises 1998, 748), after which the economy will evenly rotate (meaning that the actors will repeat their maximizing actions). In this final stage of the ERE, knowledge ceases to be important (Howden 2009) since every actor has already acquired all relevant knowledge and their maximizing behavior is known.

In other words, the period of transition amounts to a process of discovery in which actors figure out their maximizing options in each situation, a learning process without uncertainty. The maximizing options that are discovered are then perpetually repeated in the ERE since actors realize that any change in their behavior would lead to a known reduction in overall satisfaction. At this point, “the economic problem of society” (Hayek 1945, 524) no longer exists, since actors have nothing more to learn that would be of economic relevance—thus, the market process ceases. Under the assumptions of the ERE, the market process can be understood as a means to deal with and eventually overcome problems that are due to incomplete knowledge—what Kirzner (1973; 1992) refers to as “sheer ignorance.” “Essential to the notion of the market process . . . is the acquisition of market information through the experience of market participation. The systematic pattern of adjustments in market plans which makes up the market process arises . . . from the market participants’ discovery that their anticipations were overly optimistic or unduly pessimistic. It can be shown that our confidence in the market’s ability to learn and to harness the continuous flow of market information to generate the market process depends crucially on our belief in the benign presence of the entrepreneurial element” (Kirzner 1973, 13–14). This “ability to learn and to harness” information relates to knowledge, not uncertainty. They are different causes, as Kirzner (1982, 148) notes: “Whatever the possible reasons for past error, error itself implies merely ignorance, not necessarily uncertainty. To escape ignorance is one thing; to deal with uncertainty is another.” However, the ERE is structured in such a way that it deals with both knowledge and uncertainty. As Howden (2009) correctly notes, knowledge plays no role when the economy “evenly rotates,” because all actors have already discovered their maximizing options in the economy. Any alternative undertakings that are available and relevant have been tried and are known to provide the actor with lower psychic profit. The actor, then, will perpetually repeat the same higher-value option. Even so, undertakings provide actors with value because, as Mises (1998, 287) notes, “in the imaginary construction of an evenly rotating economy there are neither money profits nor money losses. But every individual derives a psychic profit from his actions, or else he would not act at all.” But, in the ERE, there is no real choice for actors: They are already fully aware of the outcomes of each option presented to them and therefore will always “choose” what they know to be of greatest value to them. Options are no longer considered after the ERE reaches the final stage.

But this is not the case during the preceding period of transition, which encompasses all economic choices that take place between the freezing of market data and all actors’ eventual discovery of their own maximizing undertakings. Actors’ undertakings during this period are a trial-and-error process that constitutes learning what specific options, in both production and consumption, are maximizing, since the data do not change—a fact that actors will also learn over time. In other words, during the period of transition, actors are not, according to the ERE’s design, subject to uncertainty, but they still suffer from the knowledge problem of not yet knowing their highest-valued alternative. As the learning process in the period of transition reaches its inescapable conclusion—when actors know their maximizing actions—the economy commences its even rotation and knowledge ceases to be a factor of importance.

We thus have three different situations in the ERE model: the real economy prior to freezing the market data, when actors must deal with both knowledge problems and uncertainty; the period of transition (the intermediate stage), when there are knowledge problems in a world with no uncertainty; and the evenly rotating economy (the final stage), when there are neither knowledge problems nor uncertainty (see figure 3). By contrasting these three stages of the model, we can conceptually distinguish between the economic significance of knowledge (or the lack thereof) and uncertainty. Since only the first of the stages—the real economy—involves bearing uncertainty to earn entrepreneurial profits or suffer losses, we can immediately see that entrepreneurship is, as Kirzner argues, distinct from knowledge problems. Entrepreneurs in the real economy can suffer knowledge problems too, and they typically do, but the praxeological category of entrepreneurship does not (Mises 1998, 286–91; cf. Bylund 2020).[8] Consequently, entrepreneurial profit or loss is also unrelated to the actor’s knowledge or lack thereof. This is well in line with Mises’s theory of entrepreneurship, which “deals with the uncertain conditions of the future. [The entrepreneur’s] success or failure depends on the correctness of his anticipation of uncertain events. If he fails in his understanding of things to come, he is doomed. The only source from which an entrepreneur’s profits stem is his ability to anticipate better than other people the future demand of the consumers” (Mises 1998, 288; emphasis added).

The “future demand of the consumers” is synonymous with their valuation of the goods that are then made available—in other words, the value knowledge that should guide producers’ production undertakings but is unavailable at the time those decisions are (and must be) made. Entrepreneurs, then, earn profits by accurately anticipating consumer value (or, more accurately, the market value that it gives to specific goods)—that is, by successfully bearing the uncertainty of the future value of the production undertakings. The conclusion, as seen in the ERE, is that value is a matter of uncertainty. But it is not a knowledge problem, because the knowledge does not yet exist—it has not yet been created, because consumers have not been exposed to, and therefore have not been able to consider, the good produced. They will do so only when the goods are available and from the perspective of the wants they feel are most urgent to satisfy at that time—that is, are of highest value to them.

The uncertainty of value means economic action is necessarily speculative: There is no firm basis on which decisions can be made about production. The entrepreneur—and the entrepreneurial aspect of every action—can only rely on his understanding of the world: “Everybody uses understanding in dealing with the uncertainty of future events to which he must adjust his own actions . . . action necessarily always aims at future and therefore uncertain conditions and thus is always speculation” (Mises 1998, 58).

But although entrepreneurial profit is a result of bearing uncertainty, this does not mean that there are no returns to knowledge—only that they are separate from the returns to entrepreneurship (namely, profit or loss). These returns are related primarily to what we have labeled technological and productivity knowledge. (Scientific knowledge is also economically important but only when applied—that is, when it informs technological or productivity knowledge.) Mises (1998, 288–89; emphasis added) clarifies:

As far as [the entrepreneur’s] own technological activities contribute to the returns earned and increase his net income, we are confronted with a compensation for work rendered. It is wages paid to the entrepreneur for his labor.

. . . [Losses] due to the technologically inefficient conduct of affairs . . . are to be debited to the entrepreneur’s personal insufficiency, i.e., either to his lack of technological ability or to his lack of the ability to hire adequate helpers. . . .

. . . [Other technological] failures are due to the fact that the present state of technological knowledge prevents us from fully controlling the condition on which success depends. This deficiency may be caused either by incomplete knowledge concerning the conditions of success or by ignorance of methods for controlling fully some of the known conditions.

Because they have incomplete or imperfect knowledge, economic actors will make mistakes and commit errors (Kirzner 1978). As a result, some actors may benefit relative to others because they have greater access to existing information (Hayek 1937; 1945), are more alert to it (Kirzner 1973; 1979), exercise better judgment of the data at hand (Klein and McCaffrey 2022; Foss and Klein 2012), or simply have more luck (Demsetz 1983). Such gains, however, are conceptually distinct from returns to entrepreneurship (Bylund 2025, 16–20).[9]

The technologically more efficient entrepreneur earns higher wage rates or quasi-wage rates than the less efficient in the same way in which the more efficient worker earns more than the less efficient. The more efficient machine and the more fertile soil produce higher physical returns per unit of costs expended; they yield a differential rent when compared with the less efficient machine and the less fertile soil. The higher wage rates and the higher rent are, ceteris paribus, the corollary of higher physical output. But the specific entrepreneurial profits and losses are not produced by the quantity of physical output. They depend on the adjustment of output to the most urgent wants of the consumers. (Mises 1998, 290)

The entrepreneur’s knowledge—whether of the scientific, technological, or productivity type—and the decision to utilize it are a matter of the extent to which he has chosen to acquire it as an investment to increase the productivity of his labor. This is a choice with estimable cost, which does not therefore constitute entrepreneurship (cf. Kirzner 2019). Entrepreneurship is—according to Mises’s definition and the ERE model—about speculating on value, specifically on how it manifests in “the future constellation of demand and supply” (Mises 1998, 291). We must, then, draw a firm line between the returns to bearing uncertainty (entrepreneurial profit or loss) and any advantages of knowledge in production. The former are necessarily unassisted by knowledge of the present state of the world and result from speculation based solely on the entrepreneur’s understanding of what future conditions will hold, whereas the latter primarily raise the productivity of factors and their market prices.

In contrast to Mises, Hayek never developed an explicit theory of entrepreneurship (Bylund 2026) and his analysis of the role of knowledge and market coordination (see, e.g., Hayek 1937; 1945; 1978) leaves little room for bearing uncertainty.[10] His focus is instead on the implications of dispersed productivity knowledge. Physical-world knowledge—scientific and technological—is assumed to be already existent and known, which means it is of no great consequence for market exchange and does not pose an economic problem. The economic problem for Hayek, as we saw above, is the coordination of economic activity—namely, production plans—given that economically relevant knowledge is known by at least some actors but unevenly distributed across the market. Because “practically every individual has some advantage over all others in that he possesses unique information of which beneficial use might be made” (Hayek 1945, 521), their actions for personal gain generate a process of discovery (Hayek 1978) through which knowledge is disseminated. The same mechanism causes “rapid adaptation” as circumstances—that is, facts about the world and actors’ knowledge of them and their economic implications—change.

It is easy to see similarities between Hayek’s conceptualization of the market economy and the period of transition in Mises’s ERE model. Although Hayek certainly does not exclude changes to market data, as the ERE does, his analysis focuses on explaining how the market can overcome the problem of existing knowledge being dispersed. He does not deal with knowledge that does not yet exist, such as value knowledge (quadrant iii). In other words, Hayek does not deal directly or specifically with uncertainty.

CONCLUSIONS

This article created a typology of knowledge. The purpose was to distinguish between different types of knowledge used in Austrian economic theorizing in order to facilitate more nuanced understanding of how knowledge in various forms is relevant to economic production in both theory and practice. Drawing specifically from Menger (2007) and Hayek (1937; 1945), we distinguished between two categories: physical-world knowledge, or knowledge about the external and primarily physical world, and catallactic-world knowledge, which deals with economizing and trade-offs in social settings and, specifically, the economy. These categories were then divided into a general form of knowledge and its specification in an applied or practical form, creating a two-by-two matrix (see figure 1).

The relationship between general and applied types of knowledge provided a basis for elaborating on how the deconstructed types of knowledge relate to each other and to economic understanding. As shown in figure 2, physical-world knowledge both limits and facilitates the use of the objective, external world by determining what economic actors can produce. Thus, both scientific and technological knowledge—the general and applied forms of physical-world knowledge—suggest what is physically possible, which draws a boundary around what goods can be produced. No producer can produce goods that, in themselves or in the production thereof, contradict this knowledge.[11]

However, physical-world knowledge does not provide insight into which goods should be produced or in what way they should be produced. Such questions can only be answered economically and must fundamentally be based on the relative value that these goods can bring. Value knowledge, the general type of economic knowledge, is the market value of a production undertaking based on the satisfaction that a good brings to a consumer; it directs which goods should be produced. Productivity knowledge—the applied type—helps determine how production of goods should be undertaken by providing knowledge about the costs involved.

All four types are relevant and important to economic theory and practice, albeit in different ways. They also have different functions and effects, which means the conception of the market process changes depending on which types are included, excluded, or emphasized. We briefly addressed two of those—the respective market processes of Hayek and Mises.

For Hayek, productivity knowledge is primary, while physical-world knowledge is of secondary importance. The former is acquired locally in the present and is then implemented in economic actions and, as a result, disseminated through the price mechanism, which causes other actors to adjust their production plans. The market as a whole is coordinative and primarily responsive to exogenous changes, as is the case with Kirzner’s (1973; 1978) alert entrepreneur reacting to and profiting from the discovery of prior errors that give rise to price discrepancies. The result is a market in constant flux, seeking, chasing, and closing in on equilibrium. Economizing here takes place primarily within quadrant iv, presumably without guidance from the value knowledge of quadrant iii. The market process solves the knowledge problem by coordinating economic actions that are taken based on incomplete and different knowledge.

This conception of the market process produces an important model for explaining the ongoing adaptations that take place in an economy and adds structured dynamism to the hopelessly static mainstream models, but its explanatory power derives from its simplicity, which is largely attained by abstracting from temporality. The uncertainty of value knowledge at the time of action is either excluded or assumed to be known (Bylund 2024), which in turn shifts focus to market coordination and the informational role of the price system (Hayek 1945). Coordination is an important feature of markets and requires study and elaboration. But to what extent does this model conform to real-world markets? We found significant similarity between this market-process model of coordination and the period of transition in Mises’s ERE. The latter explicitly builds on “the elimination of change in the data and of the time element” (Mises 1998, 247), whereas the former appears to reintroduce change but not the time element.

For Mises, by contrast, the market process is a future-oriented and value-creative process (cf. Bylund 2025) based on and directed explicitly by value knowledge. The main problem here arises from temporality—namely, the fact that the value of production is uncertain and cannot be known until after production has concluded. Thus, bearing uncertainty is key to understanding the market process. The present market data, available in the form of scientific, technological, and productivity knowledge, do not (and cannot) justify new actions: The economic problem is to act in the present to better meet the conditions of the future. Thus, for Mises, what drives the market process—and also causes it to change—is the speculative, future-oriented entrepreneurship of “promoter” entrepreneurs (Bylund 2020), who aim to benefit from better judging and taking advantage of what they imagine will be the future economic state of affairs. The prevailing economic conditions, which we as well as Hayek find in quadrant iv, are data available in the present that were generated by entrepreneurial undertakings in the past. For Mises, the value knowledge of quadrant iii, which is only speculative at the time production is undertaken, is therefore decisive for what actions to take, how to take them, and when to take them. Consequently, value knowledge determines the “direction” for the economy. Specifically, the expected market value of the enterprise (i.e., the appraised revenue) justifies its production costs and how knowledge is used (Bylund 2018; 2024; 2025).

In sum, our typology of knowledge makes clear how and why Hayek’s and Mises’s conceptions of the market process are different (Salerno 1993). Both focus on issues within the economic category of knowledge—the catallactic world—but Mises treats the uncertainty of value as the core problem of an economy and Hayek appears to presume, or even omit, value knowledge in his analysis of the market as a means to coordinate decentralized production despite dispersed knowledge.

The works of Coase and Williamson are often referenced together, but their theories are distinct and rest on assumptions that may be incompatible (Bylund 2021).

The undertaking in this article is thus similar to the typology of money that Ludwig von Mises developed in The Theory of Money and Credit (1953), which facilitated an integration of monetary theory into the larger corpus of Austrian economic theory and led to the development of the Austrian business cycle theory.

Mises’s correction aims to allow for Menger’s category of “imaginary goods,” but Mises (2003, 185) also notes that the dichotomy between real and imaginary goods is “pointless.”

We will here abstract from the complexity noted by Mises (2003, 185) that one’s knowledge of the external world may be not direct but filtered through our senses and thus consist of “opinions.”

This issue is further augmented under roundabout production (Böhm-Bawerk 1959), in which production is undertaken in stages that may be conceptually distant from the final consumption good or consumer (see, e.g., Menger 2007, 58–67). Often, the individual producer at the time production commences may not even know who the consumer of his good will be. However, as Bylund (forthcoming) notes, both theory and history prescribe that the “benefits from the division of labor and comparative advantage [which make] it highly productive . . . also increases the challenge of anticipating wants.”

A change in market data would require rapid adaptation only because the change is unknown and unexpected. If it were known, no adjustment would be needed because actors would have already adjusted their actions to the expected change.

This does not preclude that actors may be subject to class probability (Mises 1998, 107–10) or risk (Knight 1921).

Mises (1998) constructed the ERE to explain the implications of uncertainty, specifically in entrepreneurial profit and loss, which are the economic outcomes of market-based uncertainty-bearing in money terms (Knight 1921; Cantillon 1931; Mises 1998).

Factor prices, which guide entrepreneurial decision-making, already reflect the knowledge problems that burden production, because they are determined through entrepreneurial bidding: “The price of the factors of production takes into account this unsatisfactory state of our knowledge and technological power” (Mises 1998, 289). Interestingly, Mises here notes a fact that, e.g., Coase (1937) failed to recognize when distinguishing between “efficient” resource allocation through market prices and the impact of transaction costs (Demsetz 2011; Bylund 2021).

The same is arguably true for Kirzner’s theory of entrepreneurship (Kirzner 1973; 1979, cf. 1982).

The only conceivable alternative is if the existing “knowledge” is not accurate. A producer could then, by getting closer to the truth, establish production that conflicts with the supposed knowledge. But this only raises questions about whether what is believed to be knowledge is actual knowledge; it does not change the fact that production cannot contradict how the physical-world is known to work.