Fair value measurement is a cornerstone of widely used accounting standards, particularly International Financial Reporting Standards (IFRS) and US Generally Accepted Accounting Principles (US GAAP), but also UK GAAP and Australian GAAP, among others.[1] Previous research has addressed a number of questions related to fair value accounting (FVA). Among them is the fundamental one of whether fair value is a useful and sustainable measurement approach that well serves the purpose of providing decision-useful information to external stakeholders, in particular current and potential investors (Laux and Leuz 2009; Mora et al. 2019; Wallison 2009).

In dealing with fair value measurement, previous work has also touched on the ethics of FVA. The related discussion has mainly been conducted in two ways: First, because fair value measurement often involves discretion, it has been argued that the judgment involved should be ethical (e.g., Cortese-Danile, Mautz, and McCarthy 2010). For example, the reporting entity should not push all of the fair values of its assets to the upper bound of a plausible range, lest it portray itself in a (much) brighter light than it deserves. Second, FVA has been discussed from the perspective of ethics in terms of its ability to provide decision-useful information to external users of financial statements (e.g., Seay and Ford 2010).

However, there is more to understanding the ethics of FVA than these concerns. Rather than merely arguing for or against the ethicality of a particular phenomenon or an isolated action such as determining the fair value of an asset or using it in financial decision-making, Islam and Greenwood (2021, 1) encourage scholars to reconnect “to the social in business ethics.” One path they suggest for reconnecting ethical concerns in business to society at large is to bring “evaluation to prescriptive ethics to orient action.” Such evaluative ethical analysis “promotes systemic understanding by focusing on the realities built through action” (2; emphasis added).

Against this backdrop, this article highlights one implication of FVA for society at large. It does so by examining FVA through the lens of Austrian business cycle theory (Hayek 1932, 1933; Mises 1949, 1953), which reveals that FVA is one of the factors facilitating monetarily induced business cycles, such as the global financial crisis which started to erupt in 2007–8. This finding is problematic from an ethical perspective, as these business cycles are accompanied by specific distributive effects (Hülsmann 2008) and ultimately lead to distributive injustice (Mumtazy and Theophilopoulou 2017), potentially fueling social discord.[2]

This article aims to improve the understanding of the ethics of FVA by adding an additional facet to existing research efforts. We use what Arnold (2016, x–xi) labels “theoretical integration” to “point to limitations of existing research… [on the ethics of fair value],… highlighting the need for cross-disciplinary research, in order to both identify weaknesses in current understanding and constructively develop solutions to the weaknesses identified.” Drawing on Austrian business cycle theory allows us to examine the role of fair value in monetarily induced business cycles. We complement the descriptive analysis of the role of FVA in the boom phases of monetarily induced business cycles with an evaluation of this role from an ethical perspective. The article concludes by arguing that fair value is, in the context of an inflationary monetary system, neither fair nor just in this respect. It is, rather, an ethically questionable practice that facilitates business cycles that ultimately increase inflation-driven economic inequalities by benefiting some—the already wealthy—at the expense of others—the less wealthy—and potentially endangering social cohesion. In contrast, historical cost accounting avoids the objectionable distributive effects of FVA in the boom phase of the business cycle and is, in this regard, an ethically superior alternative for measuring assets in financial accounting.

Literature Review

Critical to the functioning of the market economy (Mises 1949), financial accounting is a multifaceted phenomenon. While it is primarily discussed in terms of its financial and economic facets, it also has an inherent ethical component (Duska, Duska, and Ragatz 2011; Koehn 2005; Melé and Rosanas 2005; Williams 2010). Stewart (1986, 401), citing Burton (1972), concludes that the “major ethical problem of financial reporting is that management, which has the responsibility for preparing financial reports, cannot impartially report on its own achievements.” The ethical facet of financial accounting has become increasingly important, not least since the renaissance[3] and widespread use of fair values in contemporary financial accounting. It is not surprising, therefore, that there has been a significant increase in accounting ethics research in recent decades (Bernardi and Bean 2006; Ferrentino et al. 2016).

Much of that research has embraced an applied ethics perspective. Petersen and Ryberg (n.d.) define applied ethics as “a branch of ethics devoted to the treatment of moral problems, practices, and policies in personal life, professions, technology, and government. In contrast to traditional ethical theory—concerned with purely theoretical problems such as, for example, the development of a general criterion of rightness—applied ethics takes its point of departure in practical normative challenges.” Simply put, applied ethics in (fair value) accounting refers to the appropriateness or “rightness” of the judgments and behaviors of the people involved in disclosing economic events through financial statements.

Sometimes misunderstood as a kind of unambiguous and objective set of numbers (a “true and fair view”) (Bayou, Reinstein, and Williams 2011; Sunder 2010), financial accounting is rather the result of purposeful human design (Duska, Duska, and Ragatz 2011; Espinosa-Pike 1999; Wallison 2009). It involves estimates, such as determining the useful life of depreciable assets, the amount of the allowance for doubtful accounts, or future cash flows, particularly in fair value measurements; and explicit or implicit accounting choices, such as the choice between cost-flow assumptions in inventory measurement. These estimates and choices have potentially far-reaching implications for, among other things, net income.

Thanks to financial accounting’s increased future orientation associated with the shift from historical cost accounting to FVA, Cormier and Magnan (2005) diagnose that “accounting” has meanwhile turned into “forecounting.” Owing to its ambivalent nature, financial accounting is well described as a process of making judgments about how to transform real economic events into accounting figures, in due consideration of the applicable accounting standards. Because of the discretion involved, the reflection of economic events in financial accounting is not a matter of black and white, but one of many shades of gray. It is thus amenable to various types of behavior, both ethical and unethical, of the people involved in making financial accounting decisions (Baiada-Hirèche and Garmilis 2016; Dixon and Frolova 2013; Duska, Duska, and Ragatz 2011; Merchant and Rockness 1994; Stuebs and Thomas 2011).

An important part of financial accounting is the measurement of assets, which, under both US GAAP and IFRS, reflect valuable resources that an entity owns or otherwise controls as a result of a past event and from which it expects to derive future benefits. One approach to measuring such assets is to record them at their fair value as opposed to their (depreciated or amortized and potentially impaired) historical cost (e.g., Biondi 2011). Both US GAAP (FASB ASC 820-10-20) and IFRS (IFRS 13, margin no. 9) define fair value as the “price that would be received to sell an asset . . . in an orderly transaction between market participants at the measurement date.”

Despite its name, however, fair value is often anything but a specific, objective amount (e.g., Sherman and Young 2016); instead, it must be deliberately selected from a range of plausible amounts. In other words, fair value measurement is often a prototypical example of a discretionary choice in financial accounting (Barth and Taylor 2010; Beatty and Weber 2006; Magnan 2009; Marra 2016; Ramanna 2007), and one with potentially far-reaching implications (Bignon, Biondi, and Ragot 2009). Due to its judgment-necessitating nature, fair value has inter alia been discussed from an ethical angle, mainly in two dimensions.

One stream of the literature has focused on the judgment involved in fair value determination and, hence, on the creation part of financial reports (e.g., Hodder and Sheneman 2019; Rentfro and Hooks 2006). In this context, Danile and McCarthy (2007, 47; emphasis added)—concurring with Eugene Flegm, former CFO of General Motors—believe “that the many frauds committed by top management, the largest in history, can be traced not only to the general decline in values in the past 30 years, but also to the steady move to fair value accounting by the FASB.” In addition to increasing the potential for fraud, the discretion in measuring assets at fair value has also increased the potential for earnings manipulation (Cho et al. 2022) or earnings management, which are legitimate, purposeful decisions and subsequent actions designed to alter net income in one way or another (Anderson, Bhattacharjee, and Moreno 2006; Wallison 2009). While lower asset measures generally decrease net income compared to what it otherwise would have been, higher asset measures increase it.[4] Unlike earnings fraud, such earnings management is neither illegal nor necessarily morally questionable in and of itself (Anderson, Bhattacharjee, and Moreno 2006; Yaping 2006; for the opposite position see Gowthorpe and Amat (2005, 63), who assert that “micro-level creative accounting [i.e., earnings management] is informed by an intention to deceive the recipients of financial statements, and can therefore be regarded as morally reprehensible”; and Vladu, Amat, and Cuzdriorean 2017). Yet earnings management is undoubtedly an obstacle to accounting transparency; Duska, Duska, and Ragatz (2011, 143) illustrate this when describing a particular case of earnings management at Enron as a “dubious maneuver.” Wallison (2009, 6) thus categorizes earnings management as “an endemic problem throughout accounting.”

Both prior research (Cortese-Danile, Mautz, and McCarthy 2010; Smieliauskas et al. 2018) and professional bodies (IESBA (International Ethics Standards Board for Accountants) 2018; CA ANZ 2022) have addressed the judgment involved in determining fair value and related earnings management, and have primarily called for such judgment to be ethical. For example, with respect to fair value estimates, the New Zealand Institute of Chartered Accountants Code of Ethics (CA ANZ 2022, 42) requires that reporting entities “shall not exercise . . . discretion with the intention of misleading others or influencing contractual or regulatory outcomes inappropriately.” The International Ethics Standards Board for Accountants (IESBA (International Ethics Standards Board for Accountants) 2018) demands such conduct in almost equal terms. In addition to demanding strong ethics from the accountants involved, research (Amat and Gowthorpe 2004; Smieliauskas et al. 2018) has also discussed the role of accounting regulation in enabling unethical behavior in (fair value) accounting in the first place and suggested adjustments to frameworks to mitigate accountant discretion. Additional research (Liu 2018) has examined how governance mechanisms and internal controls can reduce managers’ discretion in determining fair value and, consequently, the scope for potentially unethical behavior.

A second stream of the literature has examined the users’ end of financial reporting, asking whether or not reported fair values are capable of providing decision-useful information to them, especially to current and potential future investors. In this case, the ethical component relates primarily to whether fair values transparently (and reliably) disclose relevant underlying economic events so as to adequately inform the decision-making of financial statement users.

The literature is far from settled (Magnan 2009). Seay and Ford (2010), among others, argue that FVA is ethical from an applied ethics perspective because it is a transparent messenger of economic reality. Barlev and Haddad (2003) contend that FVA is compatible with transparency and enhances the stewardship function (i.e., it is ethical in terms of providing transparent information, which, the authors argue, mitigates social conflict). Landsman (2007) also considers FVA to be informative for investors, but finds that the extent to which it is so depends on both measurement error and the source of fair value estimates.

On the contrary, King (2008) finds that FVA is likely to be neither relevant nor reliable. Frecka (2008) holds that it can be considered unethical, as it fails to deliver on the proposition to disclose appropriate information transparently. Wallison (2009) expresses fundamental concerns over FVA’s procyclicality, as this potentially (mis)leads investors into overly optimistic (boom phase) or overly pessimistic (bust phase) behavior. When discussing the fall of Enron and its use of specific fair value estimates (namely, level 3[5] fair values), Benston (2006, 483) asserts that “fair-value numbers derived from company created present value models and other necessarily not readily verified estimates provide such people [i.e., those willing to conduct unethical behavior by misusing accounting figures] with additional opportunities to misinform and mislead investors and other users of financial statements.”

Addressing both level 2 and level 3 fair values, Ronen (2008, 186) argues that on level 2 of the hierarchy, “measurement errors and mis-specified models may compromise the precision of the derived estimates. Nonetheless, Level 2 is not as hazardous as Level 3. In the latter, unobservable inputs, subjectively determined by the firm’s management, and subject to random errors and moral hazard, may cause significant distortions both in the balance sheet and in the income statement. Moreover, discounting cash flows to derive a fair value invites deception.”

Dixon and Frolova (2013, 318) contend that the “fair-value reforms to internationally recognized accounting standards have moved accounting from the world of verifiable accounting facts into the world of speculative accounting estimates. . . . The resultant financial statements have become factually opaque, with an illusion of mathematical rigor, and a density of mandatory declarations.”

While previous research has focused on the ethics of both measuring fair value and using it as a means of informing (financial) decision-making, scholars have neglected to examine additional ethical implications of FVA in a broader, more systemic perspective. In particular, there has been a lack of analysis from an ethical perspective of the role of fair value as a facilitating channel for monetarily induced business cycles that are associated with ethically questionable and potentially socially harmful distributive effects.

Fair Value Accounting in Light of Austrian Business Cycle Theory

Austrian Business Cycle Theory

The literature on business cycles is far from uniform. There is no generally accepted theoretical framework for why, when, and how cycles occur. A long-established and prominent theory of the business cycle that has received renewed attention in the context of the financial crisis of 2007–8 is the business cycle theory associated with the 1974 Nobel Memorial Prize laureate in Economic Science, Friedrich August von Hayek (Hayek 1932, 1933) and fellow economists of the Austrian school (Huerta de Soto 2020; Mises 1949, 1953).

Unlike competing theories of the business cycle (Snowdon and Vane 2005), the Austrian theory neither relies merely on an aggregate demand and aggregate supply framework nor focuses mainly on labor allocation over the cycle. Instead, it incorporates the intertemporal capital structure of the economy as the centerpiece of its framework and focuses on the allocation of capital, both funding and goods, in addition to labor over the cycle (Garrison 2001). This arrangement makes the Austrian theory well suited to tracing out the distributive effects on income and wealth that are part and parcel of the business cycle. In particular, the theory demonstrates that the business cycle is generated by the artificial expansion of money and credit engineered by a banking system regulated by a central bank and results in income and wealth moving from the poorer in society to the richer (Huerta de Soto 2020, 397–506). This theory of the business cycle is, therefore, particularly relevant to an ethical analysis and is thus well suited to the purpose of the present article.

According to the Hayek-Mises view, the business cycle is orchestrated by a central bank regulating a banking system for the purpose of generating a controlled amount of monetary inflation and credit expansion (Mises 1949, 1953). Expansionary monetary policy of a central bank initiates an economic boom by giving banks incentive to expand their supply of credit by merely keystroking loan balances to the checking accounts of borrowers. The resulting increased supply of credit suppresses interest rates below the level they would attain if the credit supply of banks were limited to funds acquired by borrowing them from savers. Lower interest rates generally mean higher present values (Bagus 2007; Huerta de Soto 2020; Rapp 2015) and, therefore, higher prices of assets and claims to assets. The prices of assets related to the lines of production of goods being bought with the borrowed money rise to an even greater extent. The higher prices of assets not only increase the equity of entrepreneurs who own and use the assets in production but increase the profitability of the production of the assets themselves. The entrepreneurs producing these assets then expand their production. The higher prices of their output generate more profit and greater equity capital in their operation. With the additional funding, these entrepreneurs can increase their demand for inputs and assets used in their production processes.

In this way, asset price inflation increases the profitability of and equity in lines of production throughout the capital structure of the economy. From the extraction of natural resources, through the production of intermediate capital goods, sequentially to the production of consumer goods, the entire intertemporal structure of production begins to be built up and lengthened out during the boom (Hayek 1932, 1933).

The augmented capital structure of the boom, however, proves to be unsustainable. Any production process in a market economy that fails to satisfy people’s preferences will suffer losses and must be abandoned in favor of production processes that do satisfy people’s preferences. The augmented capital structure of the boom fails to satisfy people’s intertemporal preferences. People only desire to shift a fraction of their incomes to future consumption by saving and investing in the present. Monetary inflation and credit expansion, however, always increase the supply of credit beyond that provided by people’s savings (Rothbard 2000, 3–19; Huerta de Soto 2020, 167–264).

As people reassert their intertemporal preferences, production processes supporting the lengthened production structure no longer earn artificially elevated profits but instead suffer losses. In contrast, normal profits emerge in production processes supporting a shorter capital structure since that is what satisfies people’s intertemporal preferences. In response, entrepreneurs reconfigure a sustainable capital structure. Doing so necessitates selling malinvested assets and misallocated resources out of lines of production suffering losses and into lines of production earning profit. For this process of liquidation and reallocation to occur, prices of assets and resources must fall sufficiently from their artificially elevated heights of the boom to make their reemployment profitable in lines for which they were not initially intended (Rothbard 2000, 11–29; Mises 1949, 564–83).

The central bank’s typical response to the bust is to attempt to arrest the process by reinflating the money stock to relieve the financial stress on the banking system and to prevent price deflation. To the extent that reinflation fuels renewed credit expansion, it will result in a new pattern of boom lines and a new configuration of a lengthened capital structure that corresponds to the new pattern. But just as the original boom was characterized by malinvestment and misallocation, so it will be with the new boom put into motion by reinflation (Rothbard 2000, 19–23; Mises 1949, 547–62).

The recovery phase of the business cycle begins when the liquidation of capital projects and reallocation of resources has resulted in a production structure that once again satisfies people’s preferences, including their intertemporal preferences. With the restoration of normalcy, the volatility of prices and changing dispersion of income and patterns of production are once again influenced by shifting preferences people have for goods and services and the response by entrepreneurs in adapting processes of production to best satisfy preferences as they shift over time. The artificial stimulus to production from the process of monetary inflation and credit expansion has been purged along with the greater volatility of prices and profits the process entails.

Fair Value Accounting in the Boom Phase of the Business Cycle

A number of factors have been blamed for causing or at least exacerbating the 2007–8 financial crisis (e.g., Bresser-Pereira 2010; Brösel, Toll, and Zimmermann 2012; Dowd 2009; Mazumder and Ahmad 2010; Nielsen 2010; Smith 2010). Most certainly the 2007–8 crisis was not monocausal, but it was a prototypical recession preceded by an artificial boom which had been induced by expansionary monetary policy in the early 2000s in response to the bursting of the dot-com bubble (Woods 2009).[6] There has been some discussion in the accounting community about the role that FVA may have played in this business cycle—that is, whether it was an original cause or catalyst of the cycle, or whether it simply acted as a messenger that revealed economic reality but did not contribute to the cycle itself (André et al. 2009; Brösel, Toll, and Zimmermann 2012; Laux and Leuz 2009, 2010; Magnan 2009; Olbrich, Rapp, and Follert 2022).

To assess the role of fair value in the first part of the business cycle (i.e., in monetary policy–induced boom phases), it is necessary to illustrate the impact of expansionary monetary policy on the fair value measurement of assets. Fair value measurements are context dependent and follow a three-level hierarchy in both US GAAP (FASB ASC 820) and IFRS (IFRS 13). Put simply, if the asset to be measured is listed in an active market, its current (unadjusted) market price equals its fair value (level 1). If no current market price is available, other observable inputs, such as prices of similar, comparable assets, serve as the basis for fair value measurement (level 2). If a market price in an active market for the asset to be measured is not available and other observable inputs are not accessible either, fair value is derived from unobservable inputs using widely accepted appraisal techniques, especially discounted cash flow (DCF) methods (level 3).

Whether and how an expansionary monetary policy changes the fair value measurement from what it otherwise would have been depends on the mechanisms by which fair values are determined at each level of the hierarchy. In general, an expansionary monetary policy aims to stimulate the economy (e.g., Herbener 1999), in particular by providing easy access to cheap credit (i.e., at comparatively low interest rates). This typically drives up asset prices (e.g., Bagus 2007, 60–74). In other words, the lower the interest rates and the easier the access to credit, the greater the demand for assets and the higher their prices, especially in the case of stocks and real estate. Consequently, if a given company holds financial investments and reports them at fair value (level 1), the book value of its investments will increase in line with the rising market prices (e.g., Olbrich, Rapp, and Follert 2022).

Level 2 of the fair value hierarchy is not much different. Suppose an entity has financial investments in unquoted stocks and measures the fair value of those stocks using the current market price of comparable stocks that are quoted. Since an expansionary monetary policy tends to raise asset prices generally (though not uniformly), a fair value measurement using a comparable asset detour will also regularly result in inflated fair values on the reporting entity’s balance sheet during periods of monetary expansion.

Although the mechanism for determining level 3 fair values is different from that for determining level 1 and level 2 fair values, the causal effects of expansionary monetary policy will generally also tend to increase level 3 fair values. The primary means of determining fair value at level 3 of the hierarchy are present value–based appraisal techniques, such as DCF methods. DCF methods have two main inputs: the expected future cash flows and the interest rate used to discount them to the present. While there are several potentially counteracting forces at play, the artificial lowering of interest rates by expansionary monetary policy generally tends to lower the discount rates applied (Rapp 2015), which in turn tends to have an increasing impact on present values (Bagus 2007, 60–74; Huerta de Soto 2020, 265–396).[7] Credit expansion triggers a period of general economic optimism (Brown 2017) and even euphoria (Bagus 2007, 62–66), causing sales, revenues, and ultimately (book) profits to reach higher levels than they otherwise would have (Rapp 2015). This makes financial outlooks seem brighter and more sustainable than they are and drives up cash flow projections, which also has an upward effect on present values. In summary, therefore, expansionary monetary policy will tend to increase not only fair values based on observable market prices, but also fair values determined using appraisal techniques.

It should be noted, however, that there are limitations to the use of fair values in different financial reporting environments. It is not the case that either IFRS or US GAAP, for example, require a reporting entity to measure all of its assets at fair value, but rather that they require that a particular portion of its total assets must or can be measured at fair value. In general, financial instruments are the most important application of fair value measurement. IFRS also allows property, plant, and equipment (PPE) to be measured at fair value but limits the use of fair value to such PPE that can be measured reliably (IAS 16), which may be more likely for some of the assets in this class, but less so for others. However, Herrmann, Saudagaran, and Thomas (2006) consider fair value measurement of PPE to be absolutely superior to the cost-based alternative and argue for full adoption of fair value to measure PPE in US GAAP, which, unlike IFRS, requires disclosure of PPE at cost (ASC 360).

In general, of course, the more an entity is subject to fair value measurement of its assets—that is, the more financial assets (and reliably measurable PPE, in the case of an IFRS user) an entity holds, the more asset price inflation will be reflected in the financial statements. However, this effect is not limited to assets explicitly measured at fair value. Asset price inflation is also reflected through an additional channel. Noncurrent assets that are generally measured at historical cost, including intangible assets and investment property carried at cost, are subject to impairment testing (e.g., IAS 36) either annually or upon an indication of impairment. The core of such impairment tests is a comparison between the asset’s carrying amount (book value) and the higher of the asset’s fair value (less costs to sell) and value in use (recoverable amount). If the higher of the latter two is less than the current carrying amount of the asset, an impairment loss is recognized. Because inflationary monetary regimes tend to increase asset prices and thus fair values, the extent to which an impairment loss may be required is reduced relative to what it would otherwise be, or even eliminated, making the financial position of the reporting entity appear brighter than it actually is.

FVA’s Distributive Effects

The reproduction of asset price inflation in corporate balance sheets through fair value asset measurement in the boom phase of the business cycle ultimately leads to higher corporate profits and owner’s equity, and is accompanied by special distributive effects that would not occur otherwise (i.e., in the absence of FVA). We will first recall the mechanisms by which both income and wealth are generally distributed in a market economy, then illustrate how this mechanism is altered by expansionary monetary policy, and finally argue that FVA facilitates an artificial and ethically questionable type of income and wealth distribution and why it does so.

In a market economy, producers earn income and accumulate wealth according to the contribution they make to the satisfaction of the demands for goods and services made by others. For example, workers contribute the productivity of their labor services, and landowners the productivity of the services of their natural resources. By organizing producers within business enterprises, entrepreneurs earn profits by facilitating consumer value experiences at a cost below consumers’ willingness to pay, and those profits are generally justified ethically (N. S. Arnold 1987; Foss 1997; Shapiro 2018).[8] The resulting patterns of income and wealth among persons in a market economy reflect the variation in the productive contributions they make across the market economy’s division of labor. These natural economic inequalities, Simpson (2009, 526) argues, are “both economically and morally desirable.”

In conjunction with a market-driven dispersion of income and wealth among persons according to their productive contributions, there is a market-driven volatility of prices, earnings, and equity in the market economy as people change their demands for goods and services and increase their knowledge about production possibilities. The resulting shifting of patterns of production, resource usage, and capital investment will alter the patterns of income and wealth. These movements, which are referred to as business fluctuations, are part and parcel of the efficiency of the market economy in satisfying people’s preferences for goods and services (Mises 1949, 578–83).

Included among the sources of business fluctuations in market economies are changes in people’s demand for money. If people wish to hold more money as an asset, then its exchange value will rise. If money were produced by private entrepreneurs acting in a competitive market for money, then they would respond to the greater profit by increasing money production (Selgin 2008). As with business fluctuations from changing demands for other goods, changing demand for money sets in motion an adjustment process in the market economy to rearrange resource use to better satisfy people’s preferences. Increased demand for money will raise money’s exchange value and therefore the profitability of its production. In response, entrepreneurs will earn profit by producing more money. These entrepreneurs will be the first users of the newly produced money. To increase production, however, they must use the additional money they are producing to increase their demands for inputs. The resulting increase in wages and other input prices will redistribute income to workers and input suppliers who are producing money. They, in turn, will increase their demand for consumer goods, which will raise the incomes of producers in those markets. Those who receive the new money more remotely from its initial source and later in the process will have their real incomes diminished as prices of the goods they are buying have been bid up by the increased demands of producers who received the new money earlier in the process. These distribution effects of money production were first analyzed by Richard Cantillon (2001, 51–91) in 1755 in his posthumously published work.[9] When such Cantillon effects are endogenous to the market economy, like all other distribution effects from changing demands, they are part and parcel of the efficiency in satisfying people’s preferences.

In contrast, the process of monetary inflation and credit expansion in the present monetary system is an alien element imposed on the market economy by state intervention into money and banking. Because the prices of financial and business assets and the income earned from holding these assets increase disproportionately during the boom, central bank–generated monetary inflation and credit inflation aggravate income and wealth inequality in society.[10] The inflation-driven increase in economic inequality occurs neither suddenly nor randomly. It requires specific channels through which the income and wealth effects of monetary and asset price inflation can gradually unfold over time. One such channel is the use of fair values to measure assets on corporate balance sheets. As shown in the previous section, expansionary monetary policy tends to increase the book value of assets when measured at their fair value. Increased asset book values—relative to what they would have been without the effects of expansionary monetary policy—ultimately cause both corporate profits and equity to increase. Owners of the reporting company’s stock benefit from this in two ways: First, higher profits generally lead to higher dividend payouts.[11] Second, higher profits, dividends, and equity generally attract additional investor demand for the company’s stock, ultimately driving up the stock price and allowing current investors to profit by selling their shares before the boom ultimately turns into a bust.

The fact that some members of society—especially those who own large amounts of financial assets, such as corporate stock—benefit, in terms of both income and wealth, from monetary inflation, its price effects, and fair value asset measurement is not the only distributive effect of expansionary monetary policy. Monetary inflation through credit expansion also generates its own redistribution process across lines of production and across time. While Cantillon effects can be augmented by astute investors who anticipate the lines of asset price inflation and buy into such lines with their existing money balances,[12] those who receive the new money first, or at least in the early stages, generally benefit the most, simply because the price increases that are the ultimate result of monetary inflation have not yet materialized in the early stages (Sieroń 2019a, 2019b). In other words, the first user advantage is to be able to use the new money at a relatively high purchasing power (i.e., before the price level rises).[13] Among those who gain early access to the newly created financial means are corporate shareholders. A decline in the market interest rate induced by an expansionary monetary policy allows companies to borrow at lower interest rates (i.e., to reduce their borrowing costs). Beyond the increase in (book) profits resulting from the fair value measurement of assets, having to pay less for debt financing, ceteris paribus, also increases the company’s net income, which tends to leave more room for dividend distributions to shareholders.

Those members of society who get access to the no-longer-so-new money only later—for example, in the form of salaries—are already confronted with the problem of rising prices or, in other words, falling purchasing power. They can only afford to buy less for the money they received due to “bad timing.” What this pattern ultimately means, then, is that an elite section of society, usually those who have already accumulated excessive wealth, are enriched relative to and at the expense of society at large by being able to get a “bigger bang for their buck.” In other words, a small minority of wealthy members of society benefits from having a disproportionate amount of wealth which they can invest in financial markets, and those benefits are magnified by the use of fair values to measure assets on corporate balance sheets. The facilitation by FVA of the process of relative enrichment of the already wealthy raises the question of FVA’s ethicality. The rest of society pays the price, through the ever-decreasing purchasing power of their financial means, of the private benefit to a few, who are not desperately in need. Writes Hülsmann (2008, 48; emphasis original): “Money production . . . redistributes real income from later to earlier owners of the new money.”

Moreover, monetary inflation and credit expansion can increase the size of financial markets relative to production in the economy, resulting in even greater income disparity. The financial expansion of the boom that stimulated production would reverse along with the liquidation of malinvestments in the bust except for the attempts by the central bank to reinflate money and credit. Reinflation directed to bail out banks can prevent further declines in the money stock. Arresting the fall in the money stock, in turn, can prevent further deflationary forces on overall prices, including asset prices. Reinflation can even ignite a new round of asset price inflation, although not a revival of the lines and locations of those of the previous boom. To the extent that reinflation puts in motion a new boom, that new boom will suffer the same fate as the previous boom: turning into a bust. While the long-term trend of production growth will slow as a result, financial markets and financial institutions supported by monetary inflation and credit expansion can continue to expand apace over time (Grant 2008).

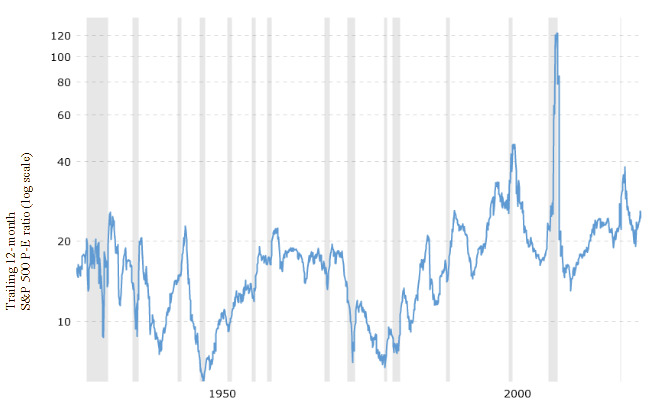

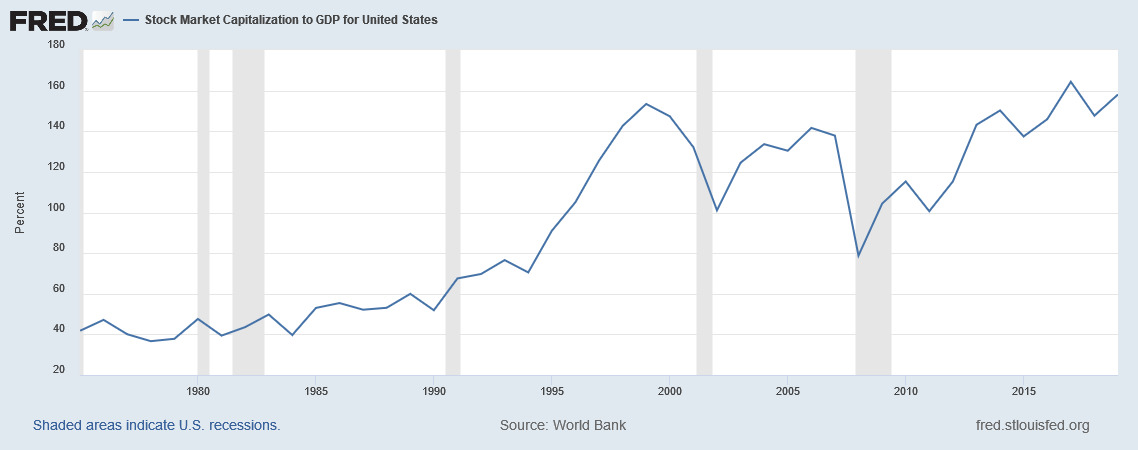

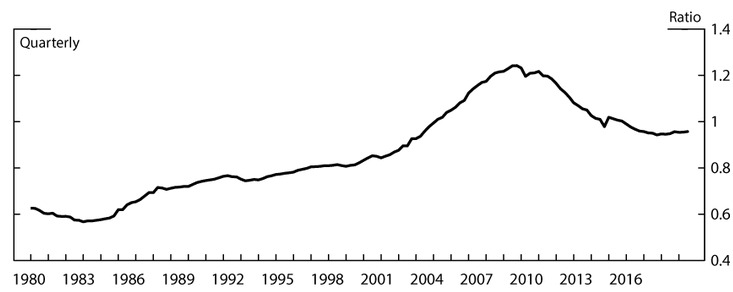

Since the early 1980s, the Federal Reserve, for instance, has aggressively reinflated at every economic downturn. The result has been a sizable increase in the ratio of financial market claims to real production. For example, price-to-earnings (PE) ratios of companies on the S&P 500 rose from 6.85 in October 1979 to 46.50 in December 2001. From August 1953 to May 1974, the PE ratios moved in a range of about 10 to 20, but from February 1992 to February 2023, the range was 20–40 (figure 1).[14] Stock market capitalization as a percentage of gross domestic product (GDP) rose from 39.68 in 1984 to 153.44 in 1999 (figure 2). Household debt-to-income ratio rose from 0.57 in 1982 Q3 to 1.24 in 2007 Q4 (figure 3).[15] Federal government debt as a percentage of GDP rose from 30.6 in Q3 1981 to 133.0 in Q2 2020 (figure 4).

The growth of financial markets, facilitated by the self-reinforcing effects of FVA, has augmented the wealth and income of the haves, who hold a disproportionate and growing share of financial claims. For example, the share of the stock market capitalization held by the top 1 percent of wealth holders in the United States rose from 36 percent to 52 percent in the largest five-year stock boom in US history, 1924–29; from 1978 to 2011, the share of capitalization held by the top 1 percent rose from 24 percent to 42 percent (figure 5). In 1989, the share of household wealth held by the bottom 50 percent of households was 4 percent, the next 40 percent held 34 percent, the next 9 percent held 36 percent, and the top 1 percent held 26 percent; by 2019, the shares were 2 percent, 27 percent, 38 percent, and 33 percent respectively (Bricker et al. 2020, fig. B).

Not only are the haves commanding a larger share of household wealth over time, but the composition of their wealth holdings is skewed toward financial assets and business assets. In 2019, 74 percent of mean household wealth for the bottom 50 percent of households was held as “other” and housing, while only 10 percent was held as financial assets and business assets. For the next 40 percent of households, 69 percent of mean household wealth was held as defined-benefit pensions, housing, and other, while only 16 percent were financial and business assets. For the next 9 percent of households, 35 percent of mean household wealth was held as financial and business assets. For the top 1 percent of households, 74 percent of mean household wealth was held as financial and business assets. Moreover, of the total mean household wealth held as financial assets and business assets, the top 1 percent held 91 percent and 95 percent, respectively (Bricker et al. 2020, fig. A).

Discussion

Fair Value Accounting, Distributive Injustice, and Impediment of Social Peace

To recapitulate, the distribution of income and wealth in a market economy follows a particular pattern: in general, market participants earn income and accumulate wealth according to their contribution to satisfying the wants of others. While this pattern is often criticized and labeled unethical because of its natural tendency to produce inequality of outcomes, the mechanism is not random or unfair—it rewards the degree to which a person contributes to the well-being of others, regardless of the cause of that contribution. In this sense, wealth creation distinguishes ethical from unethical pursuit of profit (Young 2022). If one generally serves oneself by serving others first, the income earned and wealth accumulated from that service is ethically justified (N. S. Arnold 1987; Foss 1997; Shapiro 2018; Simpson 2009). In turn, interfering with this pattern by creating artificial deviations from it is ethically problematic. External intervention jeopardizes the relationship between contributions to the satisfaction of others’ wants and the rewards for those contributions. A prototypical example of such intervention is the creation of an artificial economic boom through monetary inflation and credit expansion and its exacerbation through fair value asset measurement, as discussed in this article. As early as 1920, Keynes (1920, 235–36) noted:

By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some. The sight of this arbitrary rearrangement of riches strikes not only at security, but at confidence in the equity of the existing distribution of wealth. Those to whom the system brings windfalls, beyond their deserts and even beyond their expectations or desires, become “profiteers,” who are the object of the hatred of the bourgeoisie, whom the inflationism has impoverished, not less than of the proletariat. As the inflation proceeds and the real value of the currency fluctuates wildly from month to month, all permanent relations between debtors and creditors, which form the ultimate foundation of capitalism, become so utterly disordered as to be almost meaningless; and the process of wealth-getting degenerates into a gamble and a lottery.

Anything that contributes to the artificial inflationary boom, including fair value asset measurement, disrupts the contribution-reward mechanism and its ethical basis. In a discussion of the foregoing remark by Keynes, DeLong (2022, 425) observes: “But woven through this passage is another effect of inflation: one can usually pretend that there is a logic to the distribution of wealth—that behind a person’s prosperity lies some rational basis, whether it is that person’s hard work, skill, and farsightedness, or some ancestor’s. Inflation—even moderate inflation—strips the mask. There is no rational basis.”

FVA is one factor that facilitates the business cycle by introducing asset price inflation into corporate balance sheets, thereby manipulating the contribution-reward pattern and causing distributive injustice. We consider this arbitrary alteration of the distribution of wealth and income to the privileged group of wealthy persons at the expense of others to be unethical. Relatedly, Simpson (2009, 537) concludes that “government policies that seek to redistribute income should be opposed for economic and ethical reasons.” Convincing arguments in favor of arbitrarily benefiting some at the expense of others by measuring assets at fair value seem implausible. Interpersonal utility comparisons are impossible (Robbins 1938; Rothbard 1956), and so it is impossible to determine whether the benefit to some outweighs the loss to others. But even if interpersonal utility comparisons were possible, and FVA would produce greater benefits for some than detriments for others, there is no obvious reason why the contribution-reward pattern should be artificially and arbitrarily altered. How could it be justified ethically that an already privileged group benefits at the expense of others through FVA’s tendency to exacerbate artificial booms? Relatedly, Endörfer and Larue (2022, 22; emphasis added) urge “market participants to engage in mutually beneficial transactions while respecting two moral side constraints, [one of which is] the requirement not to exploit . . . market failures that foreseeably generate significant morally relevant harm.” Business cycles, exacerbated by FVA, are often (mis)portrayed as market failures (when they are in fact the result of regulatory interventions and their failures), and thus fit well with the call for avoidance made by Endörfer and Larue (2022).

In the above quote, Keynes (1920, 235–36) emphasizes that those who benefit from the inflationary boom, the “‘profiteers,’ . . . are the object of the hatred of the bourgeoisie, whom the inflationism has impoverished, not less than of the proletariat.” Facilitators of the inflationary boom, including FVA, cause inflation-driven economic inequality between social groups, which can aggravate social discord. Fehr (2018, 123) writes that “a major concern is that too much inequality may trigger social unrest and conflicts between social classes.” This is because “high economic inequality . . . undermines the social fabric of society and engenders anomie” (Jetten, Mols, and Selvanathan 2020, 3). In fact, economists have long known that interventionist policies and their effects can, among other things, cause social unrest (Mises 1998). Inflationary monetary policy and the expansion of credit, exacerbated by FVA, are prototypical examples of such policies. It is not surprising, then, that there has been a growing trend of social unrest in Western countries following the massive monetary inflation unleashed both by the US Federal Reserve’s and the European Central Bank’s responses to the financial, sovereign debt, currency, and health crises of the past decade and a half and by the shift to FVA spurred by the large-scale adoption of IFRS accounting in the EU in 2005.[16]

Policies leading to social discord that result in the destruction or even the attenuation of the social order are unethical on that ground as well. In its economic aspect, society is the cooperation of persons within a division of labor. By taking advantage of people’s differing efficiencies, specialization in the use of resources increases productivity beyond self-sufficient production. Only within a market economy, however, can the potential of the greater productivity of the division of labor be realized (Mises 1949). The freedom that persons have within the market gives them scope to discover and implement new technology in production and to extend the division of labor into new fields. Persons can, thereby, pursue their interests and develop their personal potential as participants in the social order. Mises (1949, 164) wrote:

Seen from the point of view of the individual, society is the great means for the attainment of all his ends. The preservation of society is an essential condition of any plans an individual may want to realize by any action whatever. Even the refractory delinquent who fails to adjust his conduct to the requirements of life within the societal system of cooperation does not want to miss any of the advantages derived from the division of labor. He does not consciously aim at the destruction of society. He wants to lay his hands on a greater portion of the jointly produced wealth than the social order assigns to him. He would feel miserable if antisocial behavior were to become universal and its inevitable outcome, the return to primitive indigence, resulted.

Since the late eighteenth century, free market economies and the development of production fostered within them have produced unprecedented levels of growth and standards of living (Maddison 2001; Rand 1966). Not only has the market economy raised the average standard of living to heights unimaginable to people living in 1800, but the greater productivity developed since then has allowed an explosion in population. Not surprisingly, the Index of Economic Freedom (Heritage Foundation 2024) lists the wealthiest and most developed countries as the most free. However, the existence of (mostly) free markets in certain countries is not a random phenomenon; their existence and persistence depends heavily on their widespread public acceptance. Patterns that interfere with the market process, thereby interfering with its desirable contribution-reward mechanism and instead creating inflation-driven economic inequality, are likely to eventually cause societal discomfort. It seems a plausible conjecture that people, by and large, will resent harmful interference with a system they generally consider desirable. Such resentment may eventually lead to social discord that disrupts a system—the free market—that almost guarantees economic prosperity and is on the whole ethically preferable to coercive alternatives. For example, when parts of the workforce walk out to strike and demonstrate against growing economic inequality, goods and services that could have been provided are not provided, and thus society as a whole is worse off than it otherwise would have been. The sophisticated division of labor in today’s market economies is undermined by persistent social unrest and, as a result, is unable to realize its full potential. This is reflected not least in the study by Hadzi-Vaskov, Pienknagura, and Ricci (2021), which empirically observes the negative macroeconomic impact of social unrest.[17]

As has been argued throughout this article, FVA is a facilitator of monetarily induced business cycles and thus contributes to unethical distributions of income and wealth that artificially increase economic inequality in society. Because an artificial, unjustified increase in economic inequality can create social discomfort, FVA may also subtly contribute to rising social tensions and the tendency to express discomfort through social unrest. Since such tendencies often prove to be detrimental overall, any artificial stimulus to social discord should be removed. For this reason and in this respect, the widespread use of FVA should be reconsidered.

Is Historical Cost Accounting a More Ethical Alternative?

While certainly not the only contributor, FVA is one contributor to business cycles induced by expansionary monetary policy and thus produces ethically questionable distributions of income and wealth. It does this by reproducing the artificial rise in asset prices caused by monetary inflation and credit expansion on corporate balance sheets, making these companies appear more economically viable than they may actually be. Ultimately, the artificially created boom increases dividend payouts and stock prices relative to what they otherwise would have been, thereby undeservedly enriching those already wealthy elites who own large holdings in corporations.

The primary alternative to FVA for measuring assets on the balance sheet is to record them at their (depreciated or amortized and potentially impaired) historical cost. The use of historical cost as a measure of assets has been rejected by many in both academia and practice because, it is argued, it does not provide information that is both timely and useful for decision-making (e.g., Laux and Leuz 2010).[18] Whether the critics of historical cost are right or wrong, there is more to the evaluation of alternative asset measures than timeliness and decision-usefulness; ethical considerations should also be taken into account.

As argued throughout this article, in inflationary monetary systems FVA has ethically inappropriate features. Historical cost accounting, on the other hand, is ethically acceptable when fair value is not. Historical cost, once actually incurred by the reporting company, acts as a ceiling on increases in book value.[19] In other words, even if the market price of a particular asset, such as a particular stock, rises above its historical cost, the book value of that stock may never exceed its original cost. Therefore, asset price inflation is not reflected in historical cost balance sheets as it is in balance sheets based on FVA. The use of historical cost serves as a barrier against an unearned distribution of income and wealth, and reduces the magnitude of artificially created booms. It does not tend to further benefit a wealthy minority at the expense of society as a whole. In the context of inflationary monetary systems, historical cost takes precedence over fair value in the measurement of assets in this respect.

Does Its Procyclical Nature Make Fair Value Accounting Absolutely Unethical?

Focusing on inflationary monetary environments, we have characterized FVA as unethical because it facilitates and reinforces the occurrence of monetarily induced business cycles accompanied by arbitrary and inequitable distributions of income and wealth that benefit the wealthy at the expense of society as a whole. But does this make FVA absolutely unethical? In other words, is FVA’s contribution to distributive injustice and impediments to social peace sufficient reason to reject it entirely on ethical grounds, or is there more to a holistic assessment of its ethicality?

FVA is a multifaceted and complex phenomenon, as is its ethical dimension. The contribution of FVA to the development of business cycles and their potentially far-reaching devastating effects seems to be sufficient reason to disqualify FVA as unethical—in this particular respect. But there are certainly other aspects that are relevant when discussing the ethics of FVA from a systemic, societal perspective. Examples that come to mind are the intended goal of fair value to provide information that facilitates the efficient allocation of resources, and instances of contracting that involve the use of fair value in one way or another, such as compensation contracting (Henderson 2022). In both of these cases, the use of fair value may be considered to be efficiency enhancing and, as such, ethically superior to its cost-based alternative. At least there is some literature that suggests that this is so (Barlev and Haddad 2003; Seay and Ford 2010; Shivakumar 2013). However, the use of fair value may also be ethically questionable in these respects. For example, Shalev, Zhang, and Zhang (2013) find that the fair value dependence of CEO pay may incentivize the misuse of earnings management for the private benefit of the CEO, which is potentially unethical, not least from a societal perspective. Dechow, Myers, and Shakespeare (2010) argue that fair value discretion can be (mis)used to overstate current gains from asset securitizations, making (potentially socially) costly future impairments more likely.

Assessing the ethics of fair value holistically is a very challenging, if not impossible, endeavor. There are several potentially opposing forces at play. Some facets of FVA appear unethical, while others may appear ethical. At present, only the ethicality of specific facets of FVA can be assessed. But as more and more of these individual pieces of the puzzle are explored, a more complete picture of the ethics of FVA may emerge.

Our primary goal here is not to stigmatize the use of FVA in inflationary monetary contexts as absolutely unethical and despicable. Rather, we seek to encourage scholars not to limit their consideration of the ethics of FVA to its determination or use in financial decision-making, but rather to broaden the field of academic inquiry into the ethics of FVA and to consider it from a more systemic and societal point of view. We believe that by linking the ethics of FVA to the Austrian theory of the business cycle, we have contributed a first step in this endeavor, and we hope to have stimulated many more steps to come. The ethical dimension of FVA is important at the societal level; it does not only concern individual accountants and users of financial statements. Therefore, we would like to encourage the academic community to study the ethics of fair value from a systemic, societal perspective. We believe this is a viable avenue for future research to improve our understanding of the various ethical implications of FVA for society as a whole. Ultimately, we may arrive at a much more comprehensive, perhaps even more or less definitive, understanding of the ethics of FVA. Such an understanding may be informed not least by analyses that go beyond the boundary conditions set in this article.

An obvious question to ask in this context is whether the assessment made in this article still holds or whether it needs to be modified when analyzing the ethics of FVA in a natural monetary order characterized by mild price deflation (i.e., outside the setting of this article). While a detailed analysis is beyond the scope of this article, the general thrust is clear: if asset prices in general tend to fall slightly over time rather than being boosted by inflationary interventionism, then neither fair value nor historical cost accounting will artificially inflate asset book values and, in turn, maintain the illusion of a better financial condition of the reporting company than is actually justified by economic fundamentals. While it would still be debatable whether increasing asset book values above their historical cost is a reasonable approach to asset measurement and financial accounting in general, increases in asset prices, such as those of stocks, would not result from artificial booms, making the reflection of such increases through FVA at least much less problematic from an ethical perspective.

Conclusion

FVA is an issue of ethical concern. Previous research has examined the ethical component of FVA in terms of the judgment involved in its measurement and the ability of fair value to provide decision-useful information to users of financial statements. This article advances the understanding of the ethics of FVA by adding a new dimension to the debate and examining it from a systemic, societal perspective. Drawing on Austrian business cycle theory, it argues that FVA is a channel through which business cycles induced by expansionary monetary policy unfold and cause inequitable income and wealth distribution effects in inflationary monetary contexts. In other words, FVA helps generate unearned private profits for a powerful elite at the expense of society as a whole.

Dacin et al. (2022, 872; emphasis added) offer a fundamental concern when they suggest that “perhaps our system of financial accounting . . . is no longer appropriate to this . . . era. Perhaps it even serves to occlude the means by which an elite can generate private profits without producing any goods.” In light of the argument presented in this article, this concern seems more than justified. While FVA may have ethical features, and may be ethically preferable to historical cost accounting in some ways yet to be discovered, it is unethical in the sense that it allows private gains for some at the expense of society by reinforcing business cycles induced by expansionary monetary policies. Roberts and Mahoney (2004, 399) thus rightly “demonstrate the need for accounting researchers to become more focused on ethical considerations in the design of . . . financial reporting models.” Accounting scholars should focus much more attention on further examining the ethics of fair value, especially from a systemic and societal perspective. Both accounting research and accounting practice, especially standard setters, should take into account the emerging evidence on the systemic ethics of fair value and, where appropriate, reconsider their preference for FVA over historical cost accounting if the potentially socially devastating consequences of FVA outweigh its benefits and need to be mitigated.

In the remainder of this article, there are a few references to specific accounting standards, such as IFRS 13 and FASB ASC 820. Each reference is to the current version of those standards as of the date of this article, which is spring 2024, as issued by the International Accounting Standards Board (IASB) for IAS/IFRS or the Financial Accounting Standards Board (FASB) for US GAAP.

In analyzing FVA with a different focus (namely, the agricultural sector), Elad (2007, 773; emphasis added) underscores the role of fair value in social conflict when he concludes that “far from enhancing accountability to stakeholders or resolving agency problems in the agricultural sector, FVA has actually played a major ideological role in sustaining social conflict.”

While the impression is sometimes given that FVA is a twentieth-century invention (e.g., Barlev and Haddad 2003), Richard (2005) discusses the concept of fair value, which dates back at least to 1673, in early French and German accounting regulations.

Not all changes in fair value affect the reporting entity’s net income. Depending on the specific case, changes in fair value may be reported as part of “other comprehensive income” (OCI). While OCI is separate from the income statement and therefore does not change net income, a positive OCI will increase owners’ equity and thus contribute to an improved picture of the company’s financial position. However, while certain fair value changes will be recognized only in OCI, IFRS 9, Financial Instruments includes a fair value option for certain cases of accounting for debt instruments, which results in fair value changes being recognized in the income statement, and requires most fair value changes of equity instruments to be recognized in the income statement.

Both US GAAP (ASC 820) and IFRS (IFRS 13) contain a context-dependent hierarchy for fair value determination spanning from level 1 to level 3 inputs. The lower the level (the higher the level number), the higher the degree of inputs necessitating judgment and, consequently, the greater the space for discretion, earnings management, and ethically questionable behavior (Danile and McCarthy 2007). Unsurprisingly, trust in fair values was observed to decrease along the hierarchy levels, with the lowest degree of trust on level 3 (Tang et al. 2016).

It is therefore no mystery that proponents of the business cycle theory of the Austrian school were among the few to call the crisis ahead of time. See, for example, Thornton (2004) or Peter Schiff’s crisis predictions shared on various occasions on US television in 2006 (e.g., Folkenflik 2008).

It is important to note, however, that there are exceptions to this tendency. Whether or not a decrease in discount rates leads to higher present values ultimately depends on the structure of the projected cash flows (Hering, Olbrich, and Rapp 2021). Negative estimated cash flows will actually increase present values when discount rates decrease. Therefore, it is inaccurate to maintain a general claim that lower discount rates lead to higher present values, as recently done by Kruk (2020), for example.

This view has certainly been challenged. For example, Allinson (2004, 18) argues that the “profit system, defined as a win-loss system, is inherently unethical. By definition, one man’s profit is another man’s loss. In order to profit, therefore, one must cause loss in another. The very making of profit is inherently unethical.” However, this assessment mistakenly buys into the zero-sum view of exchange. For a profit to be made, both parties must believe that they are better off as a result of the exchange. One man’s gain is another man’s gain, not his loss (Mises 1949). Relatedly, Maitland (1997, 17; emphasis added) argues that “the market . . . strengthens its own foundations and reproduces a moral culture that is functional to its own needs,” and Cohen and Peterson (2019) argue that market mechanisms are ethical because they best help satisfy consumer preferences.

For a general appreciation of Richard Cantillon, see Rothbard (1995, 343–62).

Research indicating the uneven income and wealth effects of inflationary monetary policy includes, among others, Adam and Tzamourani (2016), Colciago, Samarina, and de Haan (2019), De Luigi et al. (2023), Erosa and Ventura (2002), Hülsmann (2014), and Israel (2017).

It could be argued that in many environments, such as the EU, IFRS-based financial statements and the profits they calculate are not, in a strictly legal sense, the ones that determine dividend payouts. However, corporate practice has shown that the profits calculated in IFRS-based financial statements are indeed relevant to dividend policy.

We are grateful to an anonymous referee for this point.

For an example of empirical work on Cantillon effects, see Thornton (2018).

Except for three outliers: 2006, when the PE ratio was 17; 2009, when it was 120; and 2011, when it was 13. The main point is that PE ratios had roughly doubled in the later period compared to the earlier period.

These precise numbers can be accessed by consulting the source for figure 3.

A prototypical example of this social unrest is the “rise of the Yellow Vest movement as a collective response to perceptions of growing levels of economic inequality in France whereby collective action is triggered by the perceived illegitimacy of the growing gap between the ‘haves’ and ‘have-nots’” (Jetten, Mols, and Selvanathan 2020, 1).

Social unrest that leads to reforms favorable to the market society can be ethically justified—for example, the well-known social unrest in the late German Democratic Republic. Such unrest was an expression of people’s rejection of oppression, an overarching state, and restrictions on personal freedom—an expression that a majority of people would regard as positive.

Others, however, have convincingly argued that historical cost is, in fact, the superior approach to measuring assets, including for satisfying the demand of investors for decision-useful information (e.g., Braun 2014; Hering, Olbrich, and Rollberg 2010; Schmalenbach 1959).

It should be noted that historical cost accounting also includes fair values. The main difference is that in the historical cost regime, fair values are used only if they are less than the historical cost carrying amount of an asset, which oftentimes triggers impairment of the asset. However, for the purposes of this discussion, the most important difference between FVA and historical cost accounting is that historical cost accounting prevents the artificial inflation of asset measures on the balance sheet.